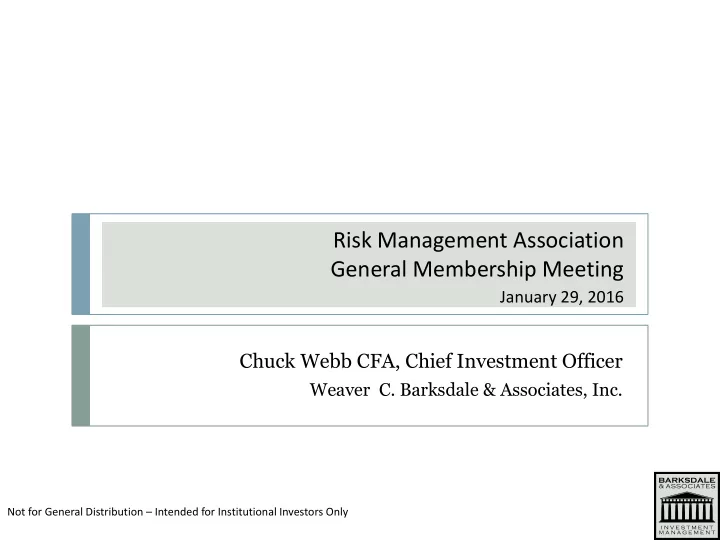

Risk Management Association General Membership Meeting January 29, 2016 Chuck Webb CFA, Chief Investment Officer Weaver C. Barksdale & Associates, Inc. Not for General Distribution – Intended for Institutional Investors Only

WCB 2015 Returns by Asset Class Percent 10 9.00 5 0.55 0.48 0.05 0 -2.41 -5 -5.30 -10 -15 -14.80 -20 -25 -24.66 Non - U.S. Non - U.S. Emerging U.S. Dollar U.S. Fixed U.S. Equity Cash Commodities Dev. Equity Fixed Mkts Equity 2015 Return 9.00 0.55 0.48 0.05 -2.41 -5.30 -14.80 -24.66 Source: Barclays, Bloomberg, SunGard 2

Source: Pensions & Investments 1/11/16 3

Equity Market

S&P 500 Price Performance WCB 2400 2200 October 07 Peak to 2000 March 09 Trough: -56.8% 1800 1600 1400 3/09 Low to Now: +183% 1200 1000 800 600 07 08 09 10 11 12 13 14 15 16 5

Chinese Yuan vs U.S. Dollar WCB 6.00 6.00 6.20 6.20 6.40 6.40 China Devalues Yuan 6.60 6.60 6.80 6.80 11 12 13 14 15 16 Source: Bloomberg, 6

S&P 500 Total Return WCB Since Stock Market Bottom March 2009 Value of $100 Invested 3-31-09 thru 1-27-16 China Devalues Yuan 360 320 340 300 320 280 300 260 280 240 260 220 240 220 200 200 180 180 160 160 140 140 120 120 100 100 10 11 12 13 14 15 16 Source: Bloomberg, 7

U.S. and Global Economic Growth WCB 1995 - 2015 OECD industrial Production Index 110 105 100 95 90 85 80 75 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 Source: Bloomberg 8

Developed Economies (OECD) GDP Estimate WCB 2.5 2.5 2.5 2.5 2.4 2.4 2.4 2.4 2.3 2.3 2.3 2.3 2.2 2.2 2.2 2.2 2.1 2.1 2.1 2.1 2.0 2.0 June 30 2016 9

10

Source: IBD 1-6-16

WCB U.S. Dollar Brent Crude Oil Futures Price Oil / bbl 140 140 130 130 120 120 110 110 100 100 90 90 80 80 70 70 60 60 50 50 40 40 30 30 20 20 10 10 05 06 07 08 09 10 11 12 13 14 15 16 Source: Yardini Research, JP Morgan, Bloomberg 12

WCB U.S. Dollar vs Crude Oil Price U.S. Dollar Oil / bbl 75 140 130 JP Morgan Tradeable Brent Crude Oil <---- Currency Index Futures Price ---> 120 80 110 100 85 90 80 90 70 60 95 50 40 100 30 20 105 10 05 07 09 11 13 15 Source: Yardini Research, JP Morgan, Bloomberg 13

U.S Dollar Index WCB U.S. Dollar Index 105 105 100 100 95 95 90 90 85 85 80 80 75 75 70 70 05 06 07 08 09 10 11 12 13 14 15 16 Source: Bloomberg 14

Total U.S. Exports WCB 3 Month Average (000) 150 Recession Recession 125 100 75 50 99 01 03 05 07 09 11 13 15 Source: Bloomberg, Bureau of Labor Statistics, 15

Corporate Earnings vs Manufacturing WCB y/y % Change S&P 500 Earnings Estimate ISM Manufacturing Indices 50 70 12 Mo S&P Earnings Est. (L) ISM (R) 40 30 60 20 10 50 0 -10 40 -20 -30 -40 30 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 Source: Bloomberg 16

S&P 500 Earnings vs Stocks WCB THE STOCK MARKET IS BEING DRIVEN BY EARNINGS S&P 500 S&P 500 As Reported Earnings 2,400 40 Estimated EPS 9-30-15 35 2,100 S&P 500 30 1,800 25 Estimated 1,500 EPS 20 1,200 15 900 10 600 5 10 11 12 13 14 15 16 Source: Gerring Wealth Management, Standard and Poors 17

S&P 500 Earnings vs Price WCB S&P 500 Earnings S&P 500 Stock Price 200 S&P 500 Earnings S&P 500 2400 40 8 120 2 Both have grown at an annualized 6.3% rate over the past 50 years 0 6 68 71 74 77 80 83 86 89 92 95 98 01 04 07 10 13 16 Source: Bloomberg, WCB Computations 18

S&P 500 WCB Monthly Close 2200 2100 2000 Recession Recession 1900 1800 1700 1600 1500 1400 1300 1200 1100 1000 900 800 700 600 99 01 03 05 07 09 11 13 15 Source: Bloomberg, Bureau of Labor Statistics, 19

IBD 9-4-15 20

U.S. Real GDP Growth WCB Annual Rate of Change y/y Fed Tightening Range GDP y/y change U.S. GDP GROWTH 8 8 7 7 6 6 5 5 4 4 3 3 2 2 1 1 0 0 -1 -1 -2 -2 -3 -3 -4 -4 -5 -5 -6 -6 -7 -7 -8 -8 -9 -9 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 Source: Bloomberg 21

GDP Predictor WCB * Housing Starts, Yield Curve, ISM Mfg, Sales Expectations, Real M2, LEI, Philly Fed Business Outlook COMBINED GDP MODEL* y/y% GDP 8 10 Model ( L ) Y/Y GDP ( R ) 8 6 6 4 4 2 2 0 0 -2 -2 -4 -4 -6 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 Source: Bloomberg, WCB Computations 22

S&P 500 Earnings Peak WCB % Above Prior Post WWII Non-Disinflation Cycle Peak Percent Above Prior Peak Earnings 120 111.6 100 EPS Peaks 68% above the prior EPS Cycle Peak implies $154 80 Currently at $125 67.8 67.6 60.6 60 36.3 40 30.4 20 - 06/49- 10/74- 12/87- 10/02- Average of 03/09- 08/56 11/80- 03/00- 10/07- Prior Bulls Current- Source: Fundstrat Global Advisors per Bloomberg, Factset 23

Total U.S. Employees WCB Nonfarm Payrolls (000) 145 Recession Recession 140 135 130 125 99 01 03 05 07 09 11 13 15 Source: Bloomberg, Bureau of Labor Statistics, 24

Fed’s Balance Sheet is Bloated by Crisis -Fighting Federal Reserve Total Assets ($Tn) 9/12 Fed Announces QE3 11/10 Fed Announces QE2 12/08 Fed Announces QE1 9/08 Lehman Bankruptcy Financial Crisis Ensues 25

Fed Balance Sheet Assets vs Stocks WCB THE STOCK MARKET IS BEING DRIVEN BY THE FED BALANCE SHEET EXPANSION S&P 500 Fed Balance Sheet, Trillion $ 2,400 5.0 4.5 2,100 4.0 1,800 Estimated Balance Sheet 3.5 1,500 3.0 S&P 500 1,200 2.5 The $2.5 trillion increase in the Fed’s 900 balance sheet since Quantitative easing 2.0 began has largely found it’s way into stocks. 600 1.5 09 10 11 12 13 14 15 16 Source: Gerring Wealth Management, Federal Reserve Bank of Cleveland 09/2014 26

Treasury Yield Curves WCB Treasury Yield Curves - At Various Year Ends and Current 6 6 % YTM 2006 5 5 4 4 3 3 2008 Current 2 2 2012 1 1 0 0 -1 -1 3 mo 6 mo 1yr 2 yr 3 yr 5 yr 10 yr 30 yr 7 year Change 0.26 0.24 0.12 0.06 0.1 -0.03 -0.1 0.17 12/31/2012 0.04 0.11 0.14 0.25 0.35 0.72 1.76 2.95 12/31/2006 5.04 5.06 4.93 4.79 4.71 4.68 4.68 4.79 12/31/2008 0.06 0.18 0.32 0.77 0.95 1.45 2.1 2.63 Current 0.32 0.42 0.44 0.83 1.05 1.42 2 2.8 Source: Bloomberg 27

WCB Historical Fed Monetary Policy 6 6 Fed Funds Less Inflation Real Fed Funds Rate 5 5 4 4 Inflation Measure = Average of : Trailing 12 Mo CPI ex Energy Trailing 12 Mo Median CPI 3 3 2 2 1 1 0 0 -1 -1 Prolonged negative interest rates encouraged excessive risk taking, unwise -2 -2 bank lending, and commodity inflation. Solution ? -3 -3 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 Ironically, now the Fed is encouraging risk taking and inflation through repressing interest rates. Source: Salomon Smith Barney, Bloomberg, Federal Reserve, Institute for Supply Management, Bureau of Labor Statistics, WCB computations 28

A History of Home Values WCB CASE SHILLER HOME PRICE INDEX, ADJUSTED FOR INFLATION 225 225 July 2006 200 200 175 70’s 80’s 175 Great WW 1 WW 2 Depression Boom Boom 150 150 125 125 100 100 75 75 50 50 Source: 2006 Irrational Exuberance by Robert Shiller, multpl.com/sitemap; in October 2015 dollars 29

Housing Starts WCB New Privately Owned Starts Units / Persons 2400 2200 Recession Recession 2000 1800 1600 1400 1200 1000 800 600 400 99 01 03 05 07 09 11 13 15 Source: Bloomberg, Bureau of Labor Statistics, 30

Bank Lending by Type WCB Year over Year Jan 2008 to Dec 2015 08 10 12 14 16 Total Bank Lending Commercial Real Estate Residential Real Estate Loans Source: Federal Reserve, SISR, 31

Leading Economic Indicators vs GDP WCB y/y % Leading Economic Indicators y/y% GDP (mo) 10 7 8 Stock Market Peak 10/07 6 5 4 2 3 0 -2 1 -4 -6 -1 -8 -10 -3 -12 -14 -5 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 Source: Bloomberg, WCB Computations 32

X = Current Core Inflation of 2.1% and S&P P/E Ratio of 16.8 X 33

Equity Market Valuation WCB Based on Manufacturing Data 70 60 (L) ISM Avg. (R) y/y% S&P 500 65 40 60 20 55 0 50 -20 45 ISM Avg Historical y/y% S&P 500 >60 22.0% 55-60 13.0 -40 50-55 now 53.5 5.3 40 45-50 -14.6 40-45 -33.9 <40 -40.8 35 -60 00 05 10 15 Source: ISM, Bloomberg, WCB Computations 34

35

Poop Initiated ? 36

Annual GDP Forecasts by FOMC WCB In December of the Prior Year Actual 4Q-to- 4Q GDP percent growth vs Fed’s central tendency forecast at the start of each year Actual Lower Band Upper Band 4 3 2 Dec 2014: Dec 2015: Projection Projection for 2015: for 2015: 1 2.6% - 3.0% 2.3% - 2.5% 0 -1 -2 -3 2009 2010 2011 2012 2013 2014 2015 2016 Final GDP within Fed’s Bands from previous December projection Source: Federal Reserve, Commerce Department 37

38

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries