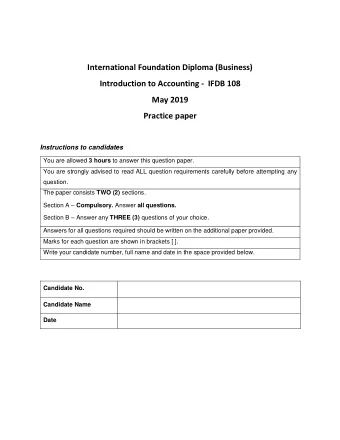

International Foundation Diploma (Business) Introduction to Accounting - IFDB 108 May 2019 Mock Paper Instructions to candidates; You are allowed 3 hours to answer this question paper. You are strongly advised to read ALL question requirements carefully before attempting any question. The paper consists TWO (2) sections. Section A – Compulsory . Answer all questions. Section B – Answer any THREE (3) questions of your choice. Answers for all questions required should be written on the additional paper provided. Marks for each question are shown in brackets [ ]. Write your candidate number, full name and date in the space provided below. Candidate No. Candidate Name Date Page 1 of 11

SECTION A – 40 MARKS Answer ALL questions Question 1 1. ‘ Income recognised against the cost incurred to generate that income .’ Which accounting principle is this describing? A business entity B matching C prudence D going concern 2. Which one of the following is recorded in sales journal? A Credit sales of goods and non-current assets B Cash sales of goods C Credit and cash sales of goods D Credit sales of goods 3. Dishonored cheques are adjusted in the ledger through; A Sales journal B General journal C Cash book D Return inwards journal 4. Jayson started graphite mine in year 2015 and he waits till it stops operations of the mine to prepare financial statements. Which accounting concept is breached through this practice? A Accounting period B matching C realisation D accruals 5. When a company accounts for accrued interest of the bank loan; A equity decreases, assets increase B equity increases, assets increase C equity decreases, liabilities increase D equity increases, liabilities increase 6. What is the correct statement? A Production cost does not include overhead costs. B All the variable manufacturing costs are direct costs. C All the direct costs are not variable costs. D Indirect labour is a part of production cost all the time. Page 2 of 11

7. Companies keep a provision for doubtful debts in accordance with; A historical cost concept. B materiality concept C prudence concept D business entity concept 8. Which of the following statement/ statements is/are correct? I. Money measurement concept explains that financial statements are valued at initial costs. II. Disclosure of accounting policies and their changes in financial statements would lead to improve the comparability. III. The legal condition of transactions should be shown in financial statements all the time. A I only B II only C I and III only D I, II and III all 9. Which is a mandatory requirement to be classified as an asset? A Existence of limited life time B Tangibility C Occurrence due to a future transaction and incident D Possibility of future economic benefits inflow 10. Which of the following is the incorrect statement on double entries? A It provides foundation for accounting equation. B The fundamental rule is to have a debit entry and identical credit entry. C It helps in identifying arithmetic errors in recording transactions. D It ensures accuracy of all the transactions entered. Page 3 of 11

Question 2 (a) AW PLC ‘s trial balance at 31 December 2018 is shown below: AW PLC Trial balance as at 31 December 2018 Description Dr ($) Cr ($) Stated Capital as at 1 January 2018 99,554 Bank Balance 1,208 Retained Earnings as at 1 January 2018 102,000 Cash in hand 8554 Trade Receivables 14,320 Trade Payables 7,311 Inventories as at 1 January 2018 10,985 Sales 190,800 Purchases 108,350 Building 190,000 Motor vehicle 158,000 Office equipment 45,000 Accumulated depreciation as at 1 January 2018 Building 32,000 Motor vehicle 41,500 Office equipment 14,000 10% Bank loan (Payable in 3 years) 75,000 Provision for doubtful debt 25 Rent 8,412 Salaries and wages 24,850 Bad debts 820 Insurance paid 1,200 Advertising cost 1,330 Electricity bill payment 3,250 Telephone bill payment 1,850 Sales commission paid 885 Additional information: 1. Inventories as at 31 December 2018 are valued at $11,302. 2. Rent of $8,000 is paid for the period of four months ending 31 March 2019. 3. Depreciation for the year ended 31 December 2018 is to be provided as follows: Page 4 of 11

Buildings – 5% per annum using the reducing balance method Motor Vehicle- 15% per annum using the reducing balance method Office equipment – 10% per annum using the straight line basis 4. Trade receivables include a debt of $900, which is to be written off as bad debt expenses at 31 December 2018. Provision for doubtful debt should be 5% on trade receivables. 5. Unpaid insurance and electricity bills for the month of December 2018 are $400 and $250 respectively. 6. Bank loan interest is not yet accounted. 7. Tax rate is 10% Required: I. Prepare the Property, plant and equipment note. (4 marks) II. Prepare the income statement for the year ended 31 December 2019. (9 marks) III. Prepare the statement of financial position as at 30 December 2018. (10 marks) (b) Karthik (Pvt) Ltd. produces and sells branded pair of shoe ‘ Ustyles ’ . The following balances were extracted from their books of accounts on 30 September 2018. $ Opening stock: Raw materials at cost 20,000 Work in progress 5,000 Carriage inwards 2,600 Returns outwards 3,500 Utilities 35,000 Factory supervisors’ salaries 90,000 Direct labour cost 160,000 Factory fixed overhead expenses 78,000 Purchase of raw material 420,000 Additional information: Raw Material closing stock is valued at cost: $15,000 and closing work in progress is valued at $6,200. 70% of utilities are spent on factory premises. Page 5 of 11

Required: I. Prepare the Manufacturing Account for the year ended 30 September 2018. (6 marks) II. Calculate the cost of a pair of Ustyles shoe , if the company manufactured 25,000 pairs during the year. (You have to show all the workings clearly) (1 mark) Page 6 of 11

SECTION B – 60 MARKS Answer any THREE (3) questions of your choice. Question 3 Telco LTD , a printing press, commenced business during May 2018. The following information relates to Telco LTD ’s first month of operations. 2018 May 1 Started business with $5,800 cash May 3 Deposited $1,900 of the cash into a bank account May 3 Bought goods for cash $260 May 4 Bought goods on credit from: Nova LTD $480; Penguin PLC $270 May 5 Bought machinery on credit from RICHARD PLC $860 May 6 Sold goods on credit to: IBM $85; Shopmore LTD $180; NLB LTD $210 May 11 Paid salaries in cash $350 May 14 Returned goods to: Penguin PLC $50 May 18 Goods returned to Telco LTD by IBM $30 May 21 Cash sales $120 May 26 Paid creditors by cheque: Penguin PLC $80 May 31 Received $110 cash from NLB LTD Required: (a) Prepare all the relevant prime entry books (journals). (5 marks) (b) Prepare all the ledger accounts. (9 marks) (c) Prepare the trial balance of Telco LTD as at 31 May 2018. (6 marks) Page 7 of 11

Question 4 (a) The following information relates to Catalyst Ltd , a single owner bakery. On 31 March 2018, the bank column of Catalyst Ltd’s cash book showed a debit balance of $2,585. On reviewing the cash book with the bank statement, it was discovered that the following transactions had not been entered in the cash book: 1. Interest payment of $240 had been charged from the bank account. 2. Cheque book charges $150. 3. Bank charges $85. 4. Rent income of $1,050 is directly deposited to the bank account. 5. A standing order of $850 for Catalyst Ltd loan repayment had been paid by the bank. 6. A debtor has directly deposited the due amount of $125 to Catalyst Ltd ’ s account. A further check revealed the following items: Cheques amounting to $960 and $640 had been collected by the bank on 31 March 2018, but, were not credited by the bank until 5 April 2018. Two cheques drawn in favour of Ideal PLC $480 and Mega PLC $840 had been entered in the cash book but had not been presented for payment. Required: I. Prepare bank account with adjustments as at 31 March 2018. (6 marks) II. Prepare the bank reconciliation statement for the month of March 2018. (4 marks) (b) Mary and Ann are in a partnership to run a business with the name MaryAnn Enterprises . They produce and sell a specific model of motorcycles for ladies. The current year 2017 has been a successful year for MaryAnn Enterprises . They run the business in a shop rented at a fixed sum of $100,000 per annum. Other fixed costs for the year amounts to $300,000. Variables costs mainly for materials and wages amount to $800 per unit and $500 per unit respectively. MaryAnn Enterprises earns a profit of $300 per unit when the production and sales are 2,000 units. Page 8 of 11

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries