ENGIE Energía Perú Corporate Presentation September 2017 (based on 2017 H1 financial figures)

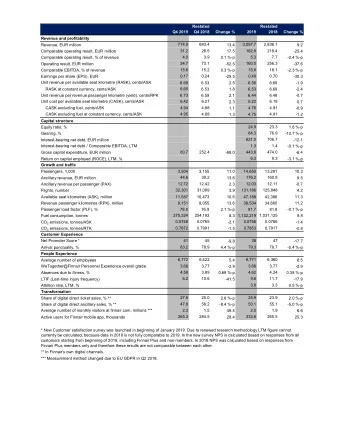

2017 H1 – EEP HIGHLIGHTS � During 2017 H1, EEP was the first private player of the sector accounting for 21% of the total capacity and 15% of the total energy generation of the system � Intipampa solar project at 73%. Expected to enter into commercial operation in early 2018 � New 15 year PPA with Marcobre @ 84MW to supply electricity demand of Mina Justa mining project subject to final NTP � In June 2017, EEP successfully issued ~ 101 MUSD of local corporate bonds in two tranches ( 25MUSD @ 7y & 76MUSD @ 10y ). Bonds were issued in local currency and backed by a cross currency interest rate swap, resulting in a final cost of debt in dollars of 3.15% and 3.55%, respectively � 2017 H1 EBITDA reached 213.7MUSD while Net Result totalized 109.9MUSD , growing 17% and 7% respectively compared to H1 2016. The increase was mainly explained by an extraordinary income from Las Bambas penalty and the start of Nodo Energetico project; which was partially offset by the end of Southern Peru Copper Corporation (SPCC) PPA � The 20-year PPA with Southern Peru Copper Corporation (SPCC) ended in April 2017 . As a result, 111.5MW from old units were disconnected from the grid as they will be no longer required. Units disconnection will not have an impact on commercial margin � Las Bambas confirmed their intention to terminate its PPA at the end of August 2017. A termination penalty of 28 MUSD due in July 2

2017 H1 - INDUSTRY HIGHLIGHTS No significant changes in market context � As of June 2017, annual energy generation (SEIN) grew 4.8% compared to similar period in 2016 � Installed capacity totalized 12,120MW . Among projects entering into operation: + Additional OCGT (+50MW): Malacas TG6 + Mini hydro projects (+40MW): Marañon & Potrero (RER auction 2011) � The country was under emergency due to heavy rains and land slides. Fortunately, EEP operations were not affected and all our generation plants were operating normally � After cancelation of the Gas to South pipe contract, Government expects to tender the project again in Q1 2018 � Natural Gas Price declaration norm was modified to allow two declarations periods (dry & rainy seasons) instead of a single annual period � Transmission line 500kv “Mantaro – Montalvo” (ISA), which increases the transmission capacity connecting the center and south of the country, is expected by Q4 2017 � Consumer access to spot market (“mercado de corto plazo”) expected to be ready in Q4 2017 3

MAIN FINANCIAL RESULTS H1 2017 EBITDA Net Result Debt Total Net Result (MUSD) Net Debt / EBITDA (12m) Total EBITDA (MUSD) EBITDA MUSD +18% -7% +7% 214 110 182 102 2.8 2.6 2016 H1 2017 H1 2016 H1 2017 H1 2016 H1 2017 H1 Total Debt (MUSD) Recurrent EBITDA* (MUSD) Net Recurrent Result* (MUSD) +2% -5% -12% 186 182 1004 951 102 90 2016 H1 2017 H1 2016 H1 2017 H1 2016 H1 2017 H1 * Does not include penalty fee and its effect on the deferred tax 4

2017 H1 SNAPSHOT Operations • Higher generation of Yuncan & Quitaracsa hydro-plants due to longer rainy season and higher generation of Ilo 21 due to transmission congestion in the south of the country • Successful operation of new projects: Chilca2 & Nodo Energetico Commercial • New 15 year PPA with Marcobre (84MW) to supply energy demand of Mina Justa • In addition to Marcobre, new contracts with Volcan (85MW) & Gloria Groups (60MW) will replace Las Bambas contract Finance • Successful 100MUSD bond issuance in local capital market: 25MUSD @ 7 years and 75MUSD @ 10 years, at final rates in USD of 3.15% and 3.55%, respectively • Reduction of average cost of debt and increase of average duration Sustainability • Training programs improved the technical and commercial capabilities of 900 entrepreneurs and small businesses • Earth Hour show in Lima (La hora del planeta”), proving clean energy through solar panels •Battery collection campaign with students from Huachon and Paucartambo communities 5

AGENDA 1 Peruvian Electricity Market 2 Company Overview 3 2016 Financial Results 4 Capital Structure 6

PERUVIAN ELECTRICITY MARKET Market Clients Generation Market share 21% 31% 44% 13% 46% Installed capacity 54% 54% 12,120 MW 18% 17% 3% +16.% y/y Hydro ENGIE Government Non Conventional Renewables Enel Generación IC Power Natural Gas Regulated Clients Free Clients Others Coal & diesel Peak demand • Main regulated clients are 6,596 MW • Natural Gas generation is • Market share as of June in Enel Distribución and Luz concentrated in Chilca terms of energy generation +5.7% del Sur (Distribution district (60km from Lima) (12m) companies in Lima) y/y • Diesel plants dispatch in • Others include: Fenix • Main free clients are case of emergency and Power, Duke, Statkraft, Mining and industrial transmission congestion Termochilca, among Annual energy companies others Generation • Clients with a consumption 49,217 GWh above 0.2MW are able to contract directly with generation companies +4.8% (free clients) y/y Information as of June 2017 7

SUPPLY & DEMAND � System is based mainly on hydro and natural gas from Camisea Field � 2 seasons: wet (from November to April) and dry (from May to October) � Electricity demand increased on average 7% annually between 2005 and 2016 (YTD) and is expected to have an average annual growth of 5-6% between 2017 and 2022; Balance Supply - Demand - Wet Season Balance Supply - Demand - Dry Season MW Reserve Reserve MW 14,000 100% 14,000 100% 12,000 12,000 80% 80% 10,000 10,000 60% 60% 8,000 8,000 6,000 6,000 40% 40% 4,000 4,000 20% 20% 2,000 2,000 - 0% - 0% 2017 2018 2019 2020 2021 2022 2017 2018 2019 2020 2021 2022 Hydro Renewable Hydro Dry Season Renewable Natural Gas (CC) Natural Gas (OC) Natural Gas (CC) Natural Gas (OC) Coal Oil and Fuel Oil Coal Oil and Fuel Oil Max Demand Reserve Wet Season (%) Max Demand Reserve Dry Season (%) Source: COES 8

MARGINAL COST RESULTING FROM SETTING UP DISPATCH ORDER 9

AGENDA 1 Peruvian Electricity Market 2 Company Overview 3 2016 Financial Results 4 Capital Structure 10

ENGIE ENERGIA PERU OVERVIEW Largest private electricity generation company in Peru 2,562 MW of installed capacity & ~8,000 GWh of annual generation Diversified & decentralized portfolio of generation sources Others, 15.0 20 years operating in the country & listed since 2005 Profuturo , 5.0 Integra, Shareholders 6.8 519 employees % ENGIE, Prima, 61.8 11.4 Solid clients Strong financials to support ambitions, AAA local rating Sponsored by a global leader 11

SPONSORED BY A GLOBAL ACTOR 12

LEADING THE ENERGY REVOLUTION THROUGH 3 PILLARS Environmental Energy efficiency awareness ENERGY REVOLUTION & Customer MEGA TRENDS Centricity New Digitalization technologies 3 pillars 13

WITH A CLEAR TRANSFORMATION PLAN 2018 14

OUR ROLE IN THE ENERGY TRANSITION � Focus on low CO2 � Reduce exposure to commodity prices � Optimum contracting level � Balanced portfolio between Regulated Clients (Distribution Companies) and Free Clients � Power Purchase Agreements under “pass-through” scheme � Minimize non-manageable risks � Balanced portfolio of assets under development � Develop solutions for clients � Geographic diversification and proximity to our clients � Customer focus: partnering with our clients to � Non conventional renewable pipeline help them finding efficiency gains � Continue with hydro mapping and studies � Value added proposals � Studies for natural gas options � Integral solutions � “one shop” approach � M&A opportunities � Leverage from worldwide experience to � Focus on improving operational efficiency elaborate tailor made solutions of existing assets 15

SUPPORTED BY A STRONG PORTFOLIO OF ASSETS Quitaracsa Hydro Yuncan 112MW Hydro #1 136MW Largest private electricity company Natural Diesel, Coal, Gas, 963, 106, 135, 38% 4% 5% 2,562MW Dual fuel, Chilca 1110, 43% Complex Hydro, 248, Natural Gas 10% 963MW Low Co2 generation base Intipampa Diversified & decentralized asset base across 4 regions Solar 40MW [under construction] Ilo Complex • Nodo – 610 MW – Dual Fuel 220 km of transmission lines + 1 substation • Ilo 31 (Cold Reserve) 500 MW - Dual Fuel • Ilo 21 – 135MW - Coal • Ilo 1 – 106 MW - Diesel 16

PROVEN TRACK RECORD IN DRIVING ORGANIC GROWTH 2,572 MW Investments for 1.6 BnUSD in 2010 - 2018 Nodo Ilo & Chilca Dos +723MW Intipampa Upsides +40MW AVERAGE More than 3x capacity in 10 years [under construction] GROWTH 18% Quitaracsa +112MW Ilo 31 +500MW Hydro Natural Gas Chilca 1 +854MW Dual Fuel 374 Solar MW Yuncan +134MW 2004 2007 2010 2013 2016 … Total Capacity MW 374 676 1,064 1,820 2,673 EBITDA MUSD 80 84 163 270 330 Market Cap MUSD - 645 1,600 2,005 1,611 17

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries