Lender and Distressed Debt Investment Panel: State of the Market - PowerPoint PPT Presentation

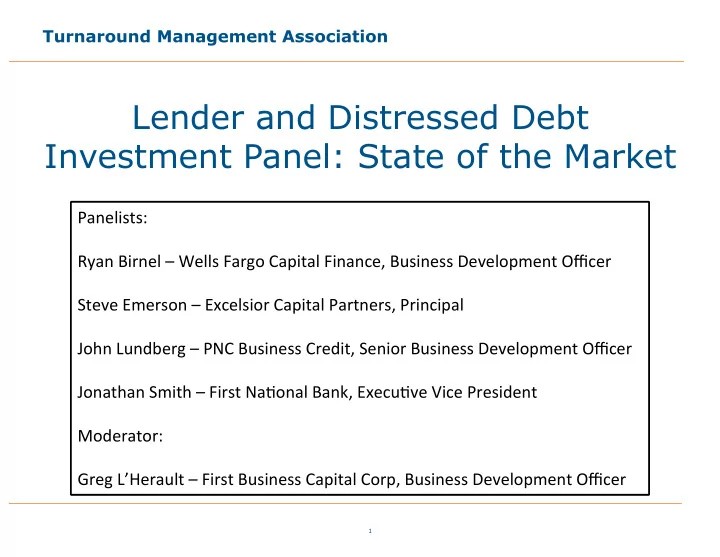

Turnaround Management Association Lender and Distressed Debt Investment Panel: State of the Market Panelists: Ryan Birnel Wells Fargo Capital Finance, Business Development Officer Steve Emerson Excelsior Capital Partners, Principal

Turnaround Management Association Lender and Distressed Debt Investment Panel: State of the Market Panelists: Ryan Birnel – Wells Fargo Capital Finance, Business Development Officer Steve Emerson – Excelsior Capital Partners, Principal John Lundberg – PNC Business Credit, Senior Business Development Officer Jonathan Smith – First NaGonal Bank, ExecuGve Vice President Moderator: Greg L’Herault – First Business Capital Corp, Business Development Officer 1

Turnaround Management Association Lender and Distressed Debt Investment Panel: State of the Market Audience Participation: Have you seen a bank make a puzzling decision recently? Here’s your chance to get a banker’s perspective! Other interesting topics we didn’t cover? Please ask questions throughout F IRST N ATIONAL 2

Turnaround Management Association Lender and Distressed Debt Investment Panel: State of the Market Agenda § Introductions § Panel Presentations: § PNC § Wells Fargo § First National Denver § Moderated Discussion § Audience Participation and Questions F IRST N ATIONAL 3

Credit Outlook The U.S. speculative default rate was 2.76% in October 2015; Moody’s default rate forecast predicts the default rate will rise § modestly to 3.77% in the U.S. by end of October 2016 – inching back to the historic average. Distressed ratios have ticked up in 2015. § − Worsening metrics are being impacted by certain industries such as metals and energy. Moody’s downgrade / upgrade ratio has been a leading indicator for the speculative grade default rate in recent history. § Default Rate Remains Below Average Distressed Ratios Downgrade / Upgrade 18% 6x 14% 35% Actual Difference 16% U.S. Speculative Grade Default Rate S&P Distress Ratio 12% 30% 5x Baseline Forecast MLHY Distress Ratio 14% 10% 25% Average 4x 12% 8% 20% 3x 10% 6% 15% 8% 2x 4% 6% 10% 1x 2% 4% 5% 0x 0% 2% 1998 2000 2002 2004 2006 2008 2010 2012 2014 0% Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15 0% Moody's Downgrade/Upgrade Ratio 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 U.S. Speculative Grade Default Rate Source: Moody’s, Federal Reserve Board, Bureau of Economic Analysis 4

Solid M&A Offset by Lack of Refinancings Refinancing Activity: Following a significant increase in refinancing activity in 2Q15, refinancing volume declined to $13.8 § billion in 3Q15, down 75.6% from 2Q15 volume of $56.5 billion. − The decline in refinancing was a result of deteriorating technical conditions in the institutional market (lack of CLO issuance and retail outflows), paired with the fact that most high-quality borrowers have already tapped the market for a refinance. Mergers & Acquisitions: Non-LBO M&A activity increased to $62.1 billion in 3Q15, up approximately 62.5% from 2Q15, § mostly as a result of increased activity in the pro rata market. − Non-LBO M&A activity in the pro rata market increased from $12.3 billion in 2Q15 to $34.8 billion in 3Q15. − While LBO issuance increased slightly from the second quarter, YTD issuance is down 14.6%. Private equity firms continue to be squeezed between high purchase price multiples and regulatory pressures to keep leverage ratios inside predetermined thresholds, lowering the population of leveraged debt LBO transactions that translate to attractive IRRs. Leveraged Loan Volume By Purpose Quarterly M&A Leveraged Loan Volume YTD YTD ∆ from 2014 3Q15 2Q15 ∆ from $90 ($ in billions) 2015 LBO Strategic (PE) Strategic (corp) 2014 2Q15 $80 Volume ($ in billions) $70 LBO $60.3 $70.6 -14.6% $20.5 $18.7 9.5% M&A (non-LBO) 142.1 144.1 -1.4% 62.1 38.2 62.5% $60 Total M&A 202.3 214.7 -5.8% 82.6 56.9 45.1% $50 Refinancing 95.6 151.7 -37.0% 13.8 56.5 -75.6% $40 Dividend 35.9 48.7 -26.4% 14.3 13.7 4.4% $30 Other 12.6 46.3 -72.9% 1.7 8.0 -79.3% $20 Total $346.4 $461.4 -24.9% $112.3 $135.1 -16.9% $10 $0 3Q09 1Q10 3Q10 1Q11 3Q11 1Q12 3Q12 1Q13 3Q13 1Q14 3Q14 1Q15 3Q15 Source: S&P Capital IQ (LCD) 5

Leveraged Lending Update The increase in leveraged debt issuance to record highs across the loan and bond asset classes in 2013 has caused § regulators to issue stringent guidelines regarding this development. Goal is to stem the potential for broad systemic risk and protect the soundness of banks. – Guidelines have resulted in increased tracking and reporting required by banks for leveraged credits. – These recent guidelines have caused certain highly leveraged deals to be constrained as banks more closely evaluate the § necessary yields that will be required to lend to these credits. Leveraged Lending Tests Senior Leverage ≤ 3.00x Non-Leveraged Lending > 3.00x Leveraged Lending Total Leverage ≤ 4.00x Non-Leveraged Lending > 4.00x Leveraged Lending 6

Regulatory Guidance Curbs Leveraged Lending Regulators finalized Leveraged Lending Guidance (“LLG”) in 2013, causing many banks to evaluate and often reduce their risk § tolerance levels. Many lenders are more reluctant to invest in transactions considered to be Highly Leveraged Transactions (“HLTs”), which § appears to have correlated to a lower trend in average leverage levels. – The rules around leveraged lending guidance continue to make the structuring of sponsored financings more difficult for arrangers and private equity firms. At $221.9 billion, 1-3Q15 sponsored loan volume was down 31% compared to the same time last year. – Although average equity contributions among sponsors have remained stable at about 39%, the distribution of equity contributions did become more weighted to buckets of 40-50+%, which represented a combined 48% of total equity weightings for 2015 sponsored deals so far this year. Although lenders still face uncertainty with regards to LLG, market respondents have begun to express a significant impact on § lender behavior compared to previous years; in 2015 no respondents indicated the LLG regulations would have zero impact on lending decisions. The elevated level of diligence and economics required for banks to support HLTs has contributed to the emergence of non- § regulated entities competing in the leveraged market. Sponsored Loan Volume at 3-year LBO Equity Contributions Rise Increased Lender Impact from LLG Low Significant Impact Modest Impact No Impact Non-LBO LBO $450 50.0% 90% $400 45.0% 80% Sponsored Issuance ($ in Billions) $350 40.0% 70% Equity Contribution (%) $300 35.0% 60% % of Respondents $250 30.0% 50% 25.0% $200 40% 20.0% $150 30% 15.0% $100 20% 10.0% $50 10% 5.0% $- 1Q-3Q97 1Q-3Q98 1Q-3Q99 1Q-3Q00 1Q-3Q01 1Q-3Q02 1Q-3Q03 1Q-3Q04 1Q-3Q05 1Q-3Q06 1Q-3Q07 1Q-3Q08 1Q-3Q09 1Q-3Q10 1Q-3Q11 1Q-3Q12 1Q-3Q13 1Q-3Q14 1Q-3Q15 0% 0.0% 2013 2014 2015 2H04 2Q05 4Q05 2Q06 4Q06 2Q07 4Q07 2009 3Q10 1Q11 3Q11 1Q12 3Q12 1Q13 3Q13 1Q14 3Q14 1Q15 3Q15 Source: Loan Pricing Corporation 7

Non-Sponsored Middle Market Loan Volume Non-sponsored Middle Market (“MM”) loan issuance year-to-date through 3Q15 was the lowest since 2010, reaching only $66.4 § billion — a 31% decline from the same period in 2014. – New money and refinancing's declined significantly in 3Q15, driving overall MM loan volume to a five-year quarterly low. – Stabilization in pricing, coupled with the recent extension of a large number of deals, has provided little incentive for borrowers to refinance, while record purchase price multiples have deterred significant M&A volume in the MM. Non-sponsored MM M&A loan volume was relatively quiet in 3Q15 at only $1.3 billion, a 67% decline year-over-year, despite the § Large Corporate market benefiting from a surge in M&A activity. – An LPC survey of lenders showed that lenders expect M&A activity will drive the bulk of loan volume in 4Q15; however, expectations for the amount of new money issuance have tempered since late 2014 given MM borrowers’ hesitation to pursue M&A transactions in the current market environment. Non-Sponsored MM Loan Volume New Money & Refinancing Volume Non-Sponsored M&A Loan Volume $5.0 M&A M&A% of Non-Sponsored 14.0% $40.0 $40.0 Traditional Large Refinancings New Money $4.5 $35.0 $35.0 12.0% $4.0 M&A Volume ($ in billions) M&A (% of Non-Sponsored) $30.0 Issuance ($ in billions) $30.0 10.0% $3.5 Issuance ($ in billions) $25.0 $25.0 $3.0 8.0% $2.5 $20.0 $20.0 6.0% $2.0 $15.0 $15.0 $1.5 4.0% $10.0 $10.0 $1.0 2.0% $5.0 $5.0 $0.5 $0.0 0.0% $0.0 $0.0 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 * Traditional Middle Market: Deal size ≤ $100.0 million * Large Middle Market: Deal size $100.0 million to $500.0 million Source: Loan Pricing Corporation 8

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.