Introduction Dividend policy is not a numbercrunching topic Javier - PDF document

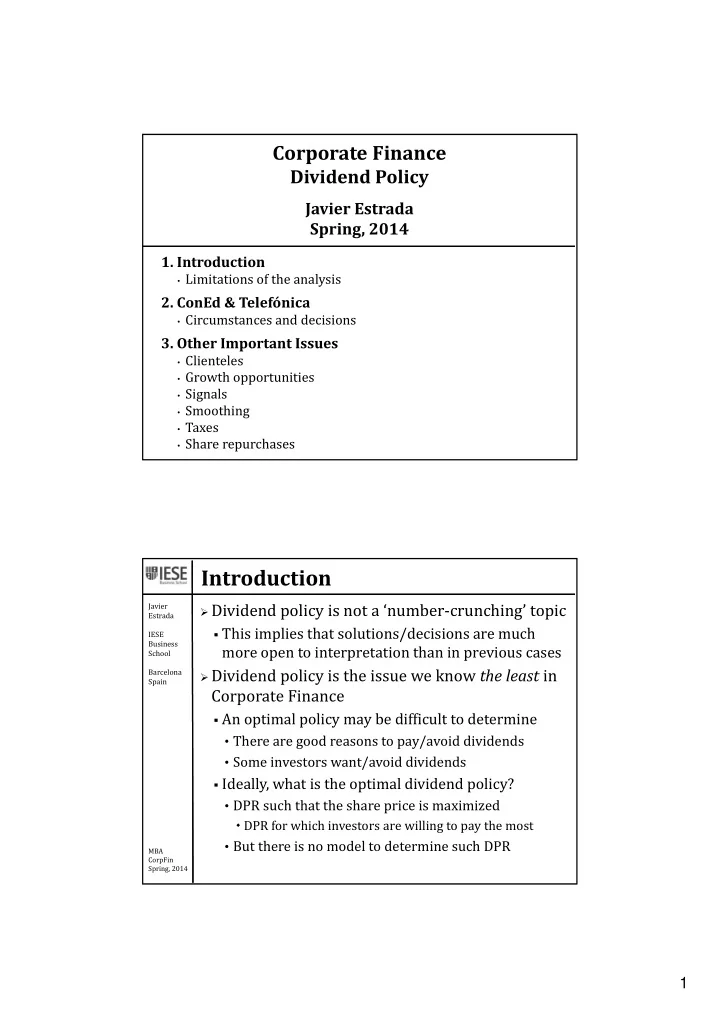

Corporate Finance Dividend Policy Javier Estrada Spring, 2014 1. Introduction Limitations of the analysis 2. ConEd & Telefnica Circumstances and decisions 3. Other Important Issues Clienteles Growth opportunities Signals

Corporate Finance Dividend Policy Javier Estrada Spring, 2014 1. Introduction • Limitations of the analysis 2. ConEd & Telefónica • Circumstances and decisions 3. Other Important Issues • Clienteles • Growth opportunities • Signals • Smoothing • Taxes • Share repurchases Introduction Dividend policy is not a ‘number‐crunching’ topic Javier Estrada This implies that solutions/decisions are much IESE Business more open to interpretation than in previous cases School Dividend policy is the issue we know the least in Barcelona Spain Corporate Finance An optimal policy may be difficult to determine • There are good reasons to pay/avoid dividends • Some investors want/avoid dividends Ideally, what is the optimal dividend policy? • DPR such that the share price is maximized DPR for which investors are willing to pay the most • But there is no model to determine such DPR MBA CorpFin Spring, 2014 1

Introduction What we do know Javier Estrada Basic trade‐off IESE Business • Reinvesting v . Paying out School Empirical regularities Barcelona Spain • Dividend smoothing • Relationship between dividend yield and income Relevant variables to consider • Environment (Macro/Industry/Company) • Clienteles (What do shareholders want/expect?) • Growth opportunities (The critical trade‐off) • Signals (The implicit message conveyed) • Dividend history (Smoothing) • Taxes MBA CorpFin Spring, 2014 Other Relevant Issues Clienteles Javier Estrada Companies can use their dividend policy to … IESE Business • please their clientele School Barcelona • target a clientele (Telefónica) Spain Critical (cash) trade‐off Reinvesting (and growing) Paying out Go MBA CorpFin Spring, 2014 2

Other Relevant Issues Signals Javier Estrada What information does management convey with IESE Business its dividend policy? School • ConEd Barcelona Spain The company is in deep trouble (The stock price tanked) • Telefónica The company has great growth opportunities (The stock price soared) • More generally Go MBA CorpFin Spring, 2014 Other Relevant Issues Smoothing Javier Estrada Dividends are sticky (less volatile than earnings) IESE Go Business Model (Lintner) School • DPS t = α ⋅ (TDPR)(EPS t ) + (1– α ) ⋅ DPS t ‐ 1 Barcelona Spain TDPR: Target dividend payout ratio α: Adjustment rate • Note that … if α=0 ⇒ DPS t = DPS t‐1 (Dividends are constant) if α=1 ⇒ DPS t = (TDPR)(EPS t‐1 ) (Dividends are just as volatile as EPS) • Empirically, Lintner found TDPR = 50% and α=0.3 DPS t = (0.15) ⋅ EPS t + (0.7) ⋅ DPS t MBA Hence smoothing is substantial CorpFin Spring, 2014 3

Other Relevant Issues Taxes Javier Estrada Dividends are usually taxed at the personal tax rate IESE Business • For wealthy individuals the personal tax rate typically School is much higher than the capital gains tax rate Barcelona Go Spain Dividends versus share repurchases As discussed, dividends tend to be smoothed Buybacks are far more volatile/unpredictable Go MBA CorpFin Spring, 2014 Appendix Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 4

Critical Trade ‐ Off Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Critical Trade ‐ Off Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Back 5

Signals Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Signals Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 6

Signals Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Signals Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 7

Signals Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Signals Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 8

Signals Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Back Smoothing Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Back 9

Taxes Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Taxes Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 10

Taxes Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Back Share Repurchases Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 11

Share Repurchases Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Share Repurchases Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 12

Share Repurchases Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Back 13

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.