Determining oil price drivers with Dynamic Model Averaging Krzysztof Drachal Faculty of Economic Sciences, University of Warsaw Research funded by the Polish National Science Centre grant under the contract number DEC-2015/19/N/HS4/00205. K. Drachal (WNE UW) Determining oil price drivers . . . 1 / 15

Potential spot oil price determinants supply and demand forces stock markets global economic activity exchange rates interest rate(s) speculative pressures (. . . ) A lot of, moreover, the impact can be time-varying K. Drachal (WNE UW) Determining oil price drivers . . . 2 / 15

Sketch of a model What people sometimes do? OLS: y t = x t θ + ǫ t ⇓ TVP-OLS: y t = x t θ t + ǫ t or Consider all possible OLS models which can be constructed out of m independent variables, i.e., 2 m OLS models, and select some subset of models from them (or even take all of them!). t θ k + ǫ k OLS: y t = x k t ⇓ TVP-OLS: y t = x k t θ k t + ǫ k t Final forecast is produced as some weighted average. K. Drachal (WNE UW) Determining oil price drivers . . . 3 / 15

Formal model: Dynamic Model Averaging (DMA) Raftery, A.E., Karny, M., Ettler, P., (2010). Online prediction under model uncertainty via dynamic model averaging: Application to a cold rolling mill. Technometrics 52, 52–66. Let there be m independent variables. Then, K = 2 m different regression models can be constructed. The state space model is given by y t = x k t θ k t + ǫ k (1) , t θ k t = θ k t − 1 + δ k (2) . t k = { 1 , . . . , K } θ k t are parameters. ǫ k t ∼ N(0,V k t ) and δ k ∼ N(0,W k t ). Initially, values of V k 0 and W k 0 have to be set. Further, V k t is estimated by a recursive method of moments estimator, and W k t by the Kalman filter updating. During this, a forgetting factor λ ∈ (0 , 1] has to be set. K. Drachal (WNE UW) Determining oil price drivers . . . 4 / 15

Weights: π t | t − 1 , k and π t | t , k Initialize the process with π 0 | 0 , k := 1 K , i.e., all models are initially equally ”good” (non-informative prior). Then, ( π t − 1 | t − 1 , k ) α + c π t | t − 1 , k = , (3) i =1 ( π t − 1 | t − 1 , i ) α + c � K π t | t − 1 , k f k ( y t | y 0 , y 1 , . . . , y t − 1 ) π t | t , k = . (4) � K i =1 π t | t − 1 , i f i ( y t | y 0 , y 1 , . . . , y t − 1 ) α ∈ (0 , 1] is a fixed forgetting factor. f k ( y t | y 0 , y 1 , . . . , y t − 1 ) is the predictive density of the k -th model at y t given the data from the previous periods. π t | t , k are called posteriori inclusion probabilities . A small constant is specified, c := K · 10 − 3 , in order to avoid reducing the probabilities to 0 due to numerical approximations. K. Drachal (WNE UW) Determining oil price drivers . . . 5 / 15

DMA DMA forecast K π t | t − 1 , k · ˆ � y k y t = ˆ , (5) t k =1 where ˆ y k t is the forecast produced by the k -th model. Notice that weights π t | t − 1 , k are continuously updated, basing on the models’ performances. Economic part: For every t sum up π t | t − 1 , k for models containing a given independent variable. Time-paths of these (summed as above) weights can be used to describe the importance of a given variables as a driver. K. Drachal (WNE UW) Determining oil price drivers . . . 6 / 15

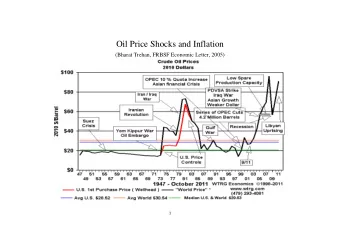

Spot oil price: Data WTI – WTI spot price in USD per barrel MSCI – MSCI World Index EM – EM (Emerging Markets) MSCI Index TB3MS – U.S. 3-month treasury bill secondary market rate in % CSP – Crude steel production in thousand tonnes TWEXM – Trade weighted U.S. dollar index (Mar, 1973 = 100) PROD – U.S. product supplied for crude oil and petroleum products in thousands of barrels CONS – Total consumption of petroleum products in OECD in quad BTU IMP – Average U.S. imports of crude oil in thousands of barrels per day INV – U.S. total stocks of crude oil and petroleum products in thousands of barrels VXO – Implied volatility of S&P 100 Monthly data beginning on Jan, 1990 and ending on Dec, 2016. Log-differences, except TB3MS and VXO (i.e., rates) which were taken in ordinary differences. Also, data were normalized (i.e., rescaled to fit between 0 and 1, which is desirable from computational point of view). K. Drachal (WNE UW) Determining oil price drivers . . . 7 / 15

Results Mean Squared Error λ \ α 1 0.99 0.95 0.90 1 0.0148 0.0147 0.0154 0.0163 0.99 0.0146 0.0146 0.0152 0.0161 0.95 0.0144 0.0143 0.0149 0.0159 0.90 0.0143 0.0142 0.0147 0.0157 naive MSE = 0.0198 TVP OLS = 0.0155 Also, Mean Absolute Error preferres DMA. Also, DMA according to minimization of MSE and MAE is preferred over Dynamic Model Selection. (In Dynamic Model Selection the final forecast is produced not as a weighted average, but comes from the model which has the highest weight in a given period.) K. Drachal (WNE UW) Determining oil price drivers . . . 8 / 15

Economic interpretation (outcomes from all 16 models) developed stock markets emerging stock markets K. Drachal (WNE UW) Determining oil price drivers . . . 9 / 15

Economic interpretation (outcomes from all 16 models) global economic activity interest rates K. Drachal (WNE UW) Determining oil price drivers . . . 10 / 15

Economic interpretation (outcomes from all 16 models) supply forces demand forces K. Drachal (WNE UW) Determining oil price drivers . . . 11 / 15

Economic interpretation (outcomes from all 16 models) exchange rates speculative pressures K. Drachal (WNE UW) Determining oil price drivers . . . 12 / 15

Economic interpretation (outcomes from all 16 models) demand forces market stress K. Drachal (WNE UW) Determining oil price drivers . . . 13 / 15

Software https://CRAN.R-project.org/package=fDMA K. Drachal (WNE UW) Determining oil price drivers . . . 14 / 15

Thank you for your attention! K. Drachal (WNE UW) Determining oil price drivers . . . 15 / 15

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries