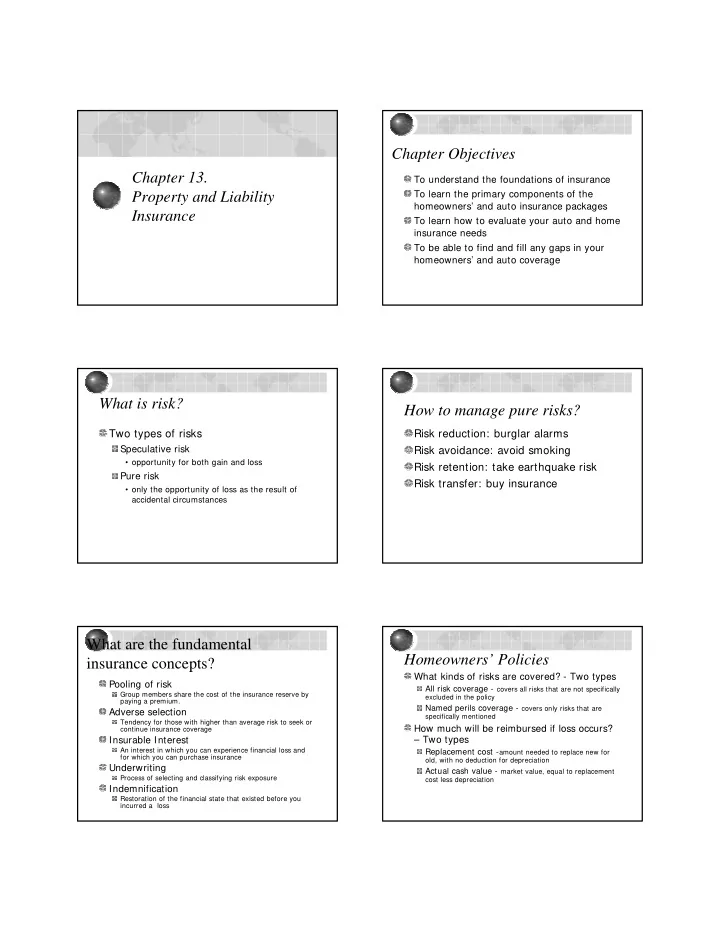

Chapter Objectives Chapter 13. To understand the foundations of insurance Property and Liability To learn the primary components of the homeowners’ and auto insurance packages Insurance To learn how to evaluate your auto and home insurance needs To be able to find and fill any gaps in your homeowners’ and auto coverage What is risk? How to manage pure risks? Two types of risks Risk reduction: burglar alarms Speculative risk Risk avoidance: avoid smoking • opportunity for both gain and loss Risk retention: take earthquake risk Pure risk Risk transfer: buy insurance • only the opportunity of loss as the result of accidental circumstances What are the fundamental Homeowners’ Policies insurance concepts? What kinds of risks are covered? - Two types Pooling of risk All risk coverage - covers all risks that are not specifically Group members share the cost of the insurance reserve by excluded in the policy paying a premium. Named perils coverage - covers only risks that are Adverse selection specifically mentioned Tendency for those with higher than average risk to seek or How much will be reimbursed if loss occurs? continue insurance coverage Insurable Interest – Two types An interest in which you can experience financial loss and Replacement cost - amount needed to replace new for for which you can purchase insurance old, with no deduction for depreciation Underwriting Actual cash value - market value, equal to replacement Process of selecting and classifying risk exposure cost less depreciation Indemnification Restoration of the financial state that existed before you incurred a loss

What are the different types of What are the major policy clauses? coverage? Replacement Cost Provision If you insure less than 80% of the total value of your house, then the reimbursement amount is reduced. Property Coverage Inflation Guard Endorsement loss of dwelling unit and personal Increases face amount of dwelling protection to reflect rising market prices belongings, such as fire damage Deductible Clause Limits payments to damages that exceed a given dollar loss Liability Coverage Mortgage Clause protection from the financial harm your Insurance payments for structural damage are made to the mortgage holder negligence causes others, such as Other Insurance and Apportionment Clause somebody falling and getting injured while Prevents insured from collecting more than 100% of the loss Subrogation Clause walking on your slippery driveway Places your right to sue for recovery after the insurer’s What are the details of property Here is an example of property coverage coverage? for a $100,000 face amount Coverage A Dwelling Protection Coverage B Appurtenant Structures Dwelling $100,000 Appurtenant structure (10%) $10,000 such as a storage shed Unscheduled property Coverage C Contents - Unscheduled On premises (50%) $50,000 Off premises (5%) $5,000 Personal Property Additional living expenses (20%) $20,000 Coverage D Loss of Use such as hotel ---------------------------------------------------------------------------- Total coverage $185,000 expenses when the house is being repaired What are the details of liability What are usually excluded from coverage? property loss coverage? Coverage E - Personal Liability articles in a floater up to limits, provides protection against legally animals, birds, or fish obligated expenses for bodily injury and property motorized land vehicles damage -$300,000 minimum coverage is recommended aircraft and parts Coverage F - Medical Payments Coverage property of roomers, boarders and tenants small amount of medical coverage to insure prompt property of apartment rented to others attention to bodily injury of others - Most policies business records and equipment limit this to $500-$1000 per person credit cards and fund transfer cards

How to deal with risks excluded from a standard policy? - What are excluded from the liability Specialized Insurance coverage? Endorsement - an amendment, extending or Slander and libel changing the underlying insurance coverage Business related liabilities Examples: replacement cost coverage endorsement on personal property, inflation guard endorsement, small Automobile related liabilities business pursuit endorsement Floater - contains scheduled property; property described in terms of type, quality, and value Examples: wedding ring, a valuable collection Umbrella Policy - extends limits on an underlying homeowners’ policy and a family auto policy Flood Insurance - federally guaranteed insurance How to select homeowners’ insurance? sold through private insurance companies. Step 1 - Determine needed amount and coverage Price set by the government 80% of market value is common If you home is in a Special Flood Hazard Area, your mortgage lender will require flood insurance Step 2 - Determine the type of needed insurance Visit http://www.fema.gov/nfip/answe2d.shtm for more Step 3 – Shop around: talk to a insurance broker or several information insurers and compare prices, get information Earthquake Insurance - high premium and high the web: visit INSWEB and Yahoo deductible. But you need to have it if you live in an Step 4 - Check out the insurance company earthquake hazard area. Step 5 - After purchase, annually review your insurance Visit http://quake.wr.usgs.gov/prepare/factsheets/RiskMaps/ needs to check earthquake risk in your area Visit the California Earthquake Authority to look up rates http://www.earthquakeauthority.com/rates/rates.html# top For some comparison information on Homeowner’s insurance in Utah, check out http://www.insurance.state.ut.us/AutoHOcomp.htm How to make sure you can collect on a Checklist for College Students loss? � Are you covered under your parents Document your property before the loss homeowners’ policy? Notify the relevant authorities and � Do you have adequate overall contact the insurer immediately after protection? the loss � Have you taken a personal inventory? Evaluate your loss before you accept a � Do you exceed the limits on specific settlement offer classes of property?

What are the major types of coverage? Automobile insurance – who needs it? If you drive a car, you need it. Part A - Liability What’s Utah’s mandated minimum liability? most important component 25/50/15 Part B - Medical Payments Meaning: payments to insure prompt treatment of injuries of • First number: bodily injury liability maximum for one the car person injured in an accident is $25,000. • Second number: bodily injury liability maximum for all Part C - Uninsured Motorists injuries in one accident is $50,000. needed coverage that also covers underinsured • Third number: property damage liability maximum for one accident is $15,000. motorists For other states, go to Part D - Damage to Your Auto http://moneycentral.msn.com/content/Insura the need for collision is determined by the value of nce/Insureyourcar/P35266.asp the car What is no-fault insurance? – Utah How is the cost of auto insurance is a no-fault state determined? Allows you to recover from your own insurer, The Rate Base regardless of who is at fault determined by your personal Verbal threshold characteristics, your driving record, your may sue for reimbursement if injury satisfies car make and model, and where you live definition High risk drivers may have to purchase Monetary threshold expensive insurance in the shared may sue for medical expenses that exceed stated amount (assigned risk) market Personal Injury Protection (PIP) mandatory requirement in no-fault states Can you reduced your premium? -Typical reasons for insurance What’s the discounts average annual Away at school Multipolicy driver cost of car household Carpool driver Nonsmoking driver insurance Good driving record Retired driver in your Good student record Mature driver state?

Chapter Objectives Chapter 14 To describe the separate components of basic health care coverage Health and Disability To discuss the need for major medical insurance Insurance To list the important providers and insurers of health care To compare and evaluate health care insurance plans To list sources of disability income To estimate your disability insurance needs What are the different types of What is basic health care coverage? health care insurance coverage? Hospital Insurance Room & board and other medical expenses while Basic Health Care Coverage in the hospital Major Medical Coverage Surgical insurance Long-Term Care Coverage Covers fees for operating surgeon and anesthesiologist Dental Insurance Physician’s expense insurance Specific Disease and Accident Insurance Payments for general nonsurgical care at the office or hospital An example of major medical coverage What is major medical coverage? Example Cost Basic payment Overage Provides protection after limits on basic Hospital bill $ 5,200.00 $ 3,000.00 $2,200 health care coverage have been Office visits 840.00 - 840.00 exceeded Surgical services 2,400.00 1,900.00 500.00 Prescription drugs 760.00 - 760.00 Typical co-insurance clause Total $ 9,200.00 $ 4,900.00 $ 4,300.00 insurer pays 80% of covered expenses Minus deductible (100.00) $ 4,200.00 dollar limit on out-of-pocket expenses 20% $ 840.00 In this case, you pay $850 out of pocket

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries