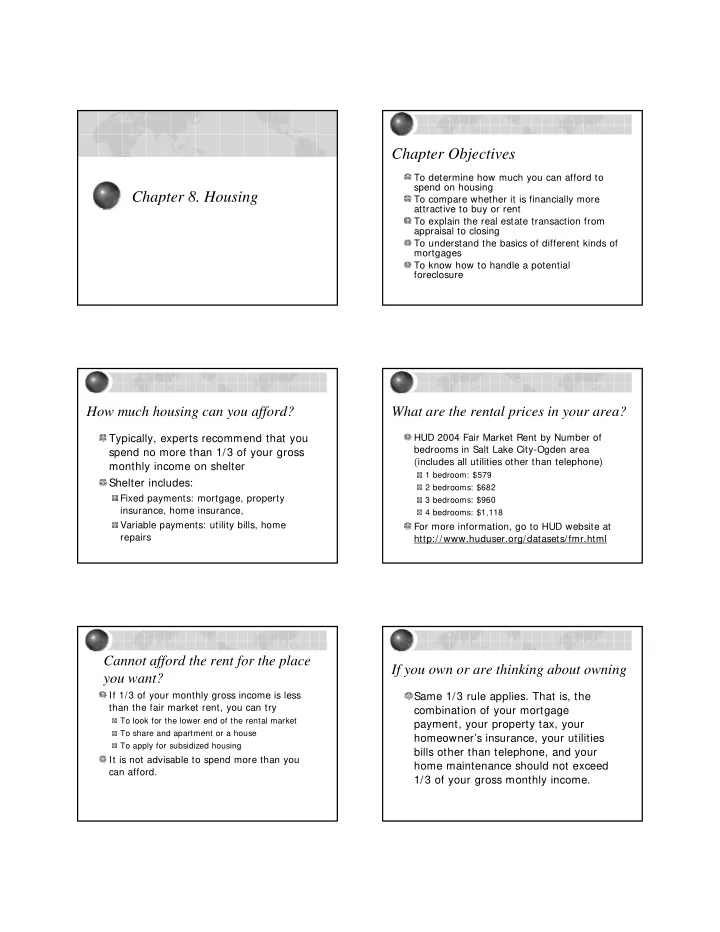

Chapter Objectives To determine how much you can afford to spend on housing Chapter 8. Housing To compare whether it is financially more attractive to buy or rent To explain the real estate transaction from appraisal to closing To understand the basics of different kinds of mortgages To know how to handle a potential foreclosure How much housing can you afford? What are the rental prices in your area? Typically, experts recommend that you HUD 2004 Fair Market Rent by Number of bedrooms in Salt Lake City-Ogden area spend no more than 1/3 of your gross (includes all utilities other than telephone) monthly income on shelter 1 bedroom: $579 Shelter includes: 2 bedrooms: $682 Fixed payments: mortgage, property 3 bedrooms: $960 insurance, home insurance, 4 bedrooms: $1,118 Variable payments: utility bills, home For more information, go to HUD website at repairs http://www.huduser.org/datasets/fmr.html Cannot afford the rent for the place If you own or are thinking about owning you want? If 1/3 of your monthly gross income is less Same 1/3 rule applies. That is, the than the fair market rent, you can try combination of your mortgage To look for the lower end of the rental market payment, your property tax, your To share and apartment or a house homeowner’s insurance, your utilities To apply for subsidized housing bills other than telephone, and your It is not advisable to spend more than you home maintenance should not exceed can afford. 1/3 of your gross monthly income.

So how expensive of a house can How much down payment should you you afford? save? The answer will depend on several It usually a good idea to put 20% of the things: house price as your down payment. That The down payment you have saved way, you don’t have to pay private mortgage • You can afford more if you have a large down insurance, which can be expensive. payment These days, you can buy a house with very The mortgage interest rate little down payment. However, you need to • You can afford more if mortgage interest rates are low be sure you can afford your monthly payment How much other debts you owe (including private mortgage insurance) and other housing related expenses. • You can afford more if you have little other debts. How high are the mortgage interest Mortgage interest rate also vary depending rates? on your credit history, the kind of loan you take, and the amount you borrow. Rates vary a lot over time. For more information, visit the Monthly Effective Interest Rate on Fixed-Rate Interest Rate Survey by the Federal Housing Mortgage 1985-2004 Finance Board at Effective rate (%) http://www.fhfb.gov/MIRS/mirs.htm 15.00 10.00 For up-to-date rate information, see 5.00 bankrate.com at 0.00 http://www.bankrate.com/brm/rate/mt 5 7 9 1 3 5 7 9 1 3 8 8 8 9 9 9 9 9 0 0 9 9 9 9 9 9 9 9 0 0 g_home.asp 1 1 1 1 1 1 1 1 2 2 Year How expensive of a house can you How does debt affect me ? - The debt afford to buy? repayment test Debt Repayment Test Housing Expense Test 7. Debt repayment-to-income ratio 36% 1. Annual gross income $75,600.00 8. Allowable debt payment $2,268 2. Monthly gross income $6,300 9. Monthly installment debt and alimony $474 Housing Expense Test 10. Total nonmortgage expense and installment $814 3. Housing expense-to-income ratio 28% debt repayment 4. Allowable housing expenditure $1,764 5. Estimated nonmortgage housing payment 340 11. Affordable monthly mortgage payment $1,454 6. Affordable monthly mortgage payment under housing $1,424 under debt repayment test expense test

How much housing can $242,585 So what’s the bottom line? buy? Your Affordable Home Purchase Depending on the location 12. Affordable monthly mortgage $1,424 Median sale price of existing single family (lesser of Line 11 or Line 6) houses in 1 st quarter 2005 ** Contract rate on home mortgage 8.00% Salt Lake City – Ogden: $158,000 ** Duration of loan (months) 360.00 San Francisco Bay area: $641,700 13. Monthly payment per $1,000 mortgage $7.34 South Bend/Mishawaka, IN: $93,600 14. Your affordable mortgage $194,068 For more information, visit the website for 15. Fractional amount borrowed 0.80 16. Your affordable home purchase $242,585 National Association of Realtors at Required Down Payment $48,517 http://www.realtor.org/Research.nsf/file s/REL05Q1T.pdf/$FILE/REL05Q1T.pdf How affordable are houses in general? What is Housing Affordability Index An index of 100 means a family earning median Typically, places that have higher housing income can qualify for a conventional loan on an prices also tend to have higher wage rates. existing median-priced home. So prices alone don’t tell the whole story. The larger the number, the more affordable houses are relative to median income in the U.S. Over time, household income also increase. For the second quarter of 2005, the housing So if income keeps up with housing price affordability index in the U.S. was 117.1. increase, then houses are not less affordable. Meaning: If a family earns about 85.4% (100/117.1) of median income in the U.S., then this family can qualify for a The Housing Affordability Index takes these conventional loan to buy an existing median-priced home. factors into consideration. For more information about Housing Affordability Index, go to The larger the index, the more affordable houses http://www.realtor.org/Research.nsf/files/REL0506A.pdf/$FI are. LE/REL0506A.pdf Buying Vs. Renting Tax advantages for home purchase Pluses Pluses Appreciation Mobility Itemized property tax deduction Tax Advantage Low Maintenance Itemized mortgage interest deduction Privacy Low Risk Negatives Tax exempt capital gain Negatives Immobility You can typically exclude from taxable income up Landlord restrictions to $250,000 ($500,000 if married) of the capital Sales Commissions No equity buildup gain on the sale of your home Maintenance No tax advantage To get the full exclusion you must have owned the Financial Risk home for the last two years, and used it as your main home for two recent year

The process of buying Buying vs. Renting Comparison Bottom Line The Real Estate Agent Buying is better Finding the house you want and can afford The longer the holding period The Purchase Contract The lower the mortgage interest rate The Home Inspection The higher your marginal income tax rate The Title Search The lower the local property tax rate The Mortgage Decision The more financial risk tolerant you are The Closing The opposite is true for renting Finding the house you want and can The agent afford Seller’s agent: represent seller The realtor will show you houses listed for sale on Multiple Listing Services (MLS) that fit Buyer’s agent: represent buyer your criteria In Utah, a seller’s agent can also You can also access MLS at represent buyers in a limited capacity. http://www.utahrealestate.com/ Issue of commission: typically, seller Read Newspaper ads for “for sale by owners”. pays commission, unless otherwise There are several for-sale-by-owner websites. specified. Go to open houses Elements of the Purchase Contract The Home Inspection A sample purchase contract Purchase price and earnest money Freddie Mac: Title http://www.freddiemac.com/sell/consumerkit/english Mortgage clause Interviewing the owners and/or occupants Pests Conducting the consumer home inspection Home inspection The final analysis Lead-based paint hazards in housing built before 1978 The American Association of Home Other environmental concerns Inspectors (ASHI): Home warranty Sharing of expenses http://www.ashi.com Settlement agent/Escrow agent Settlement costs

Title Search – done by title Home Warranties insurance company An examination of the public records in order to New home: builder’s warranty determine who may have enforceable claims Resale: home buyer’s warranty on the property Deed a written document transferring title Marketable title title free of claims by other parties Title insurance protects the insured against defective title Types of Mortgages Getting a Mortgage Mortgage brokers Government programs Fixed Rate Mortgages Federal Housing Administration (FHA) interest rate and monthly payment remain constant over the life of the loan • protects the lender against loss on the mortgage • Minimum 5% down payment Adjustable Rate Mortgages • maximum limits on the loan at interest rate is periodically adjusted over the term http://www.huduser.org/datasets/il.html of the loan Veterans Administration (VA) the monthly payment may change over the term • loan guarantees by the Veterans Administration of the loan, or the term of the loan may change • borrowers may have a debt repayment to income ratio of The initial rate (called teaser rate) is low. Rate 41% usually increases after the first year. • interest ceiling may require discount points • http://homeloans.va.gov/veteran.htm Specialize Mortgage Formats Comparing and getting a mortgage Graduated Payment Mortgage (GPM) Interest rate, points, and other fees APR – most important for comparison Scheduled increases in monthly payments Points: 1 point = 1% of loan over the term of the loan Lender required settlement costs Shared Appreciation Mortgage Appraisal Lender shares in home’s appreciated Credit report market value Mortgage insurance (if down payment < 20%) and title insurance Processing fees

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries

![Phase I Property Assessment [SLIDE 1] Phase I Property Assessment I will be presenting the Ohio](https://c.sambuz.com/763490/phase-i-property-assessment-slide-1-phase-i-property-s.webp)