Britvic Duration: 00:49:24 Gerald Corbett: Good morning everyone, - PDF document

25 th November 2009 Britvic Duration: 00:49:24 Gerald Corbett: Good morning everyone, welcome to the Britvic results. You all know John and Paul, and John is now going to take us through the details. John Gibney: Thank you Gerald, morning

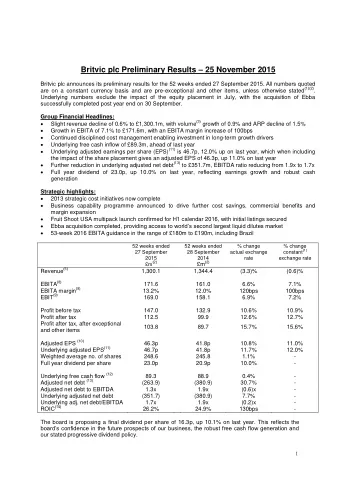

25 th November 2009 Britvic Duration: 00:49:24 Gerald Corbett: Good morning everyone, welcome to the Britvic results. You all know John and Paul, and John is now going to take us through the details. John Gibney: Thank you Gerald, morning everybody. Before we get into the details of the presentation, if you please note that we will be making available a copy of the transcript and the webcast on the Investor Relations site at Britvic.com. Both of those will be available at some point tomorrow afternoon. Today we report our results for the 52 weeks ended 27 th September 2009. This year has been another excellent year for Britvic, building on our strong financial track record led by revenue growth again. Key headlines are revenue for the Group up nearly 6% with GB and international revenues up by nearly 9% despite the economic headwinds, as Gerald described. Group EBIT margin is up 80 basis points while the GB and international margin is actually up ahead of this by around 110 basis points. Earnings are up 21% with free cash flow reaching £70 million, and these results have delivered an increase in our ROIC of 160 basis points to 17.9%. The repeated strength of our performance gives the Board confidence, as Gerald said, to propose a final dividend increase of 24% to 10.9 pence, bringing the full year dividend to 15 pence, which is an increase of 19% on 2008. This now brings us in line with our stated ambition of 2 times dividend cover – a measure we anticipate maintaining in the future. The Group revenue growth of 5.6%, which we announced last month, has translated into an EBIT of just over £110 million. This is in line with market forecasts that were significantly upgraded in July and the EBIT growth represents 14% build on last year. 1

As I mentioned, we have improved Group operating margin by 80 basis points to 11.2%, and GB and International have now totalled margin improvement of 170 basis points over the last three years, and Paul will talk later on what this means for margin guidance in the medium term. We continue to grow earnings, this time increasing by 21%. Free cash flow has again improved this year, resulting in a cumulative delivery now of £250 million free cash flow over the last four years. We continue to pay down debt, this time by a further 6%. Moving onto our strong track record, the performance again this year has added to a track record of consistent delivery on all of our key metrics. A 5.6% revenue CAGR in the underlying business since 2006 leverages down at the EBIT level to growth of around 11%. It’s also worth noting that the business has now developed revenue growth CAGR of over 4.5 percentage points since the year 2000. We now have a very strong and consistent cash flow record over this period of time, helping to drive Group EPS to a CAGR of over 17%. I’ll now move on to take you through the different reporting segments. Starting with our Carbonates portfolio, we have seen a volume outperformance of the market of 7%. Alongside this we have also achieved ARP growth of 2.7%, which combined with the volume has delivered revenue growth of 11%. Brand contribution is in excess of £150 million, representing growth of over 5% on last year. The brand contribution margin has declined by 190 bps this year, firstly due to an increased A&P spend behind our Carbonates brand, but also as a result of product and channel mix. We have driven significant growth of dispense in licensed trade and also large pack in the off-trade where the margin in these products is inherently lower than the rest of our portfolio. However, we do expect margin improvement from Carbonates in 2010. Our Stills portfolio has delivered a strong performance with growth on all of our key metrics. The volume of 3.6% increase means an outperformance of the Stills category by over 6%. We’ve achieved an ARP improvement of 2%, leading to a revenue growth of nearly 6% in the year. This increase in Stills ARP comes as a result of a number of factors including successful price accretive innovation, price management and improving our pack and product mix over time. Brand contribution is up by 7% with a margin improvement here of 40 basis points despite direct costs rising by 6%, although Stills also benefit from a lower proportion of our ARP spend this year. 2

Turning now to our International division, 2009 has once again been a year of double-digit growth. This increasingly important part of the Group saw a revenue growth of 19%, again driven by both ARP and by volume. You may recall from this time last year International achieved a brand contribution growth of 29%, and this year we have achieved further growth on top of that of 55%. In addition to the flow-through from the volume and ARP growth, the increase in Brand contribution has benefited from the lower A&P spend in the Nordics due to the brand now establishing itself in that region. As well as the success of Fruit Shoot in the Netherlands and Robinsons in the Nordics, we’ve also secured a number of new contracts in the travel sector and are actively exploring franchise and export opportunities across the world. This will principally be with Fruit Shoot and Robinsons propositions, and we’ll update you on that activity in due course. Overall volumes in Ireland are down nearly 11% this year and reflect the continuing difficult trading conditions in that market. ARP is 62 pence per litre, includes the benefit of currency movements, with the underlying Euro ARP down by 3.6%, as consumers continue to focus on value as a priority. Despite this, some synergies gained in areas such as Procurement meaning continued growth of the Bank contribution margin. Before amortisation, the EBITDA of the business was down by £2.3 million, as trading conditions directly affected the bottom line. This year we’ve continued to deliver against our stated synergy plan. As we complete the implementation of our business transformation programme in Ireland in 2010, we are confident in our ability to deliver further incremental synergies of €10 million next year. We continue to invest in the Irish business both operationally and in our people, and as a result we are confident we are shaping a business that will be well placed to take advantage of growth when it returns to the market. Moving onto out fixed costs, we’ve seen the benefit of Group supply chain restructure and synergies come through this year with fixed supply chain costs down by over 6%. We’ve also delivered top line growth of nearly 6% whilst controlling our selling costs. The increase in overheads and other costs on the face of the P&L account actually masks an underlying flat performance. The variance of £12 million you can see there is driven by the translation of Irish costs into Sterling of around £2 million. The movement on foreign exchange conversion year-on-year of £3 million and additional bonus provisions covering bother short-term and long-term schemes of £6 million. 3

A&P spend was down, though this was not due to a lowering of activity. Indeed our very successful brand equity programmes were a real driver of our volume performance this year. We have benefited from media deflation and our increasing focus on digital and viral marketing has led to a lowering of our A&P spend. We have seen TV, print, radio and outdoor media deflation in excess of 10%. Targeted investment behind our brands will remain a priority and we’ll continue to exploit the most effective channel going forward. As we move down the P&L account, a lower interest environment and another reduction in net debt has led to an 11% decrease in our interest charge this year. This is despite a significantly higher margin this year under our bank facility that was renegotiated in March of this year. The effective tax rate this year is 25.8%, an increase on last year, which is primarily due to the profit mix effect coming from a lower proportion of our profits out of Britvic Ireland. At an earnings level we’ve delivered a 21% improvement on last year with profit after tax of over £64 million, despite the economic headwinds faced in the year. Exceptional items are £20.3 million, primarily due to the business restructuring in Ireland. This charge is higher than we guided at the interims; however, the primary driver of this has been a write-down of the value of properties held for sale in Ireland. This is around a charge of €4 million, unsurprising given the current state of the Irish property market. A further 2.4 million charge relates to onerous leases on vacant properties; again, the majority of that coming through Ireland. The carrying value of our Ireland assets has been reviewed again at the year-end, and with the exception of the property assets I've already mentioned there is no impairment to value. However, we do recognise that should the Irish economy not return to growth in 2011, as widely expected, then we may need to revisit those carrying values again. There remains ample headroom in the values and sensitivities are included in note 15 to the accounts. Finally, the Group structure that we announced at the March Investor Seminar has now been implemented and the associated costs are reflected here. 4

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.