Sustainable Bonds Global Market State and Trends Christopher Kaminker, PhD Head of Research SEB Climate & Sustainable Finance christopher.kaminker@seb.se CONFIDENTIAL – NOT FOR DISTRIBUTION This presentation is solely for the use of the intended audience. No part of it may be circulated, quoted or reproduced without prior written approval from SEB. This material was used during an oral presentation; it is not a complete record of the discussion. 1

A decade of Green Bonds

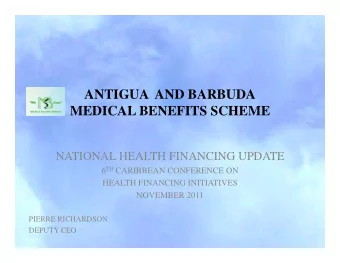

Green bond market growth and sectors of the market shifting: USD 500 bn+ in 10 years 100% 200 Sovereigns 90% 180 185 Supranationals Government agencies 80% 160 Municipal Financials 70% 140 Corporates Project 118 60% 120 ABS/MBS 100 50% 80 40% 60 30% 40 20% 20 10% 0 0% 2010 2011 2012 2013 2014 2015 2016 2017 2018 YTD 2010 2011 2012 2013 2014 2015 2016 2017 2018 YTD : Oct 11 2018 YTD 3

USD 564 billion Sustainable Bond Market Green dominates, but Sustainability and Social Bonds taking off since launch of the Social Bond Principles and Sustainability Bond Guidelines in 2017 Sustainable Bond issuance by type (USD Bn) Sustainable Bond issuance by type (% Share) 200 100% Sustainable Bond 180 90% Cumulative Issuance Green Sustainability Social 160 80% Social Sustainability 3% 6% USD 19 bn 140 70% USD 32 bn 120 60% Social 100 50% Green Sustainability 91% 80 40% Green USD 512 bn 60 30% 40 20% 20 10% 0 0% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2010 2011 2012 2013 2014 2015 2016 2017 2018 YTD YTD Source: SEB analysis based on Bloomberg and SEB data (22 October 2018) * Note: 2018 figures are likely to be revised upwards as undiscoverable US Muni, Chinese ABS/MBS, project bonds and private placements are catalogued

Global Green Bond Market by Sector, Yield and Maturity Reporting on Use of Proceeds (ex-post) 2014-2017 38% 40% (81%) (106%) 55% (22%) 5 Note: Excludes project bonds, ABS and US Municipal Source: SEB analysis using Bloomberg BVAL pricing (Sept 21, 2018)

Green share of total bond issuance by select currency Cumulative green bond issuance by currency (Right Axis) 18.0% AUD 2% CAD 16.4% 2% 160 SEK 16.0% 5% USD CNY 14.0% 15% 41% 133 12.0% EUR 35% 10.0% USD EUR CNY CAD AUD SEK 8.0% 6.5% 6.5% 59 6.0% 4.0% 1.8% 20 2.0% 9 6 0.0% 2015 2016 2017 2018 YTD Source: SEB analysis based on Bloomberg and SEB data 6 YTD as of May18 2018

Drivers of underlying green infrastructure investment Environmental and Biophysical Stress ECONOMIC TECHNOLOGICAL SECURITY INVESTORS FORCES FORCES GREEN INFRA/BOND BANKABLE POLICY SOCIAL SPECIFIC PIPELINES ALIGNMENT FORCES 7 Source: SEB analysis

S&P look-back study of environmental risks Findings S&P found 717 ratings over last 2 years where environment and climate risks were a material factor in the analysis and 106 where these led to a rating action • Of these 106 research updates that listed a climate or Upgrade, 19% environmental factor as a key driver to the rating change, the CreditWatch largest share (41%) were positive, 5% Downgrade, 41% downgrades Outlook to positive, 10% • However analyzing these results further, we see that when grouping results into positive and negative rating actions, the Outlook to stable outcomes are more balanced, from negative, 10% CreditWatch with 44% being in the positive negative, 4% direction and 56% being in the Outlook to stable negative direction. Outlook to from positive, 3% negative, 8% 8 Source: S&P (2018)

For 11 sectors, with $2.2 trillion in rated debt, environmental risks are already ratings-relevant or will be in the coming few years. Breakdown of “Elevated Risk” (Immediate/Emerging) sectors in environmental risks heat map (in USD bn) 9

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries