Mastering Form 990 Schedule L: Reporting Transactions With - PowerPoint PPT Presentation

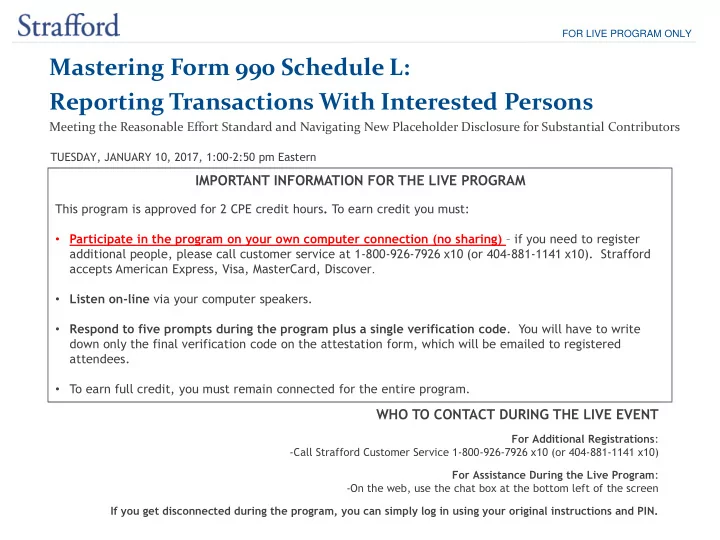

FOR LIVE PROGRAM ONLY Mastering Form 990 Schedule L: Reporting Transactions With Interested Persons Meeting the Reasonable Effort Standard and Navigating New Placeholder Disclosure for Substantial Contributors TUESDAY, JANUARY 10, 2017,

FOR LIVE PROGRAM ONLY Mastering Form 990 Schedule L: Reporting Transactions With Interested Persons Meeting the Reasonable Effort Standard and Navigating New Placeholder Disclosure for Substantial Contributors TUESDAY, JANUARY 10, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is approved for 2 CPE credit hours . To earn credit you must: • Participate in the program on your own computer connection (no sharing) – if you need to register additional people, please call customer service at 1-800-926-7926 x10 (or 404-881-1141 x10). Strafford accepts American Express, Visa, MasterCard, Discover . • Listen on-line via your computer speakers. • Respond to five prompts during the program plus a single verification code . You will have to write down only the final verification code on the attestation form, which will be emailed to registered attendees. • To earn full credit, you must remain connected for the entire program. WHO TO CONTACT DURING THE LIVE EVENT For Additional Registrations : -Call Strafford Customer Service 1-800-926-7926 x10 (or 404-881-1141 x10) For Assistance During the Live Program : -On the web, use the chat box at the bottom left of the screen If you get disconnected during the program, you can simply log in using your original instructions and PIN.

Tips for Optimal Quality FOR LIVE PROGRAM ONLY Sound Quality When listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory, please e-mail sound@straffordpub.com immediately so we can address the problem.

Mastering Form 990 Schedule L Jan. 10, 2017 Frank Giardini, Principal, Tax Services Jennifer Becker Harris, CPA, Principal Grant Thornton, Philadelphia Clark Nuber, Bellevue, Wash. frank.giardini@us.gt.com jharris@clarknuber.com Michele Melchior, Tax Director Grant Thornton, Charlotte, N.C. michele.melchior@us.gt.com

Notice ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN. You (and your employees, representatives, or agents) may disclose to any and all persons, without limitation, the tax treatment or tax structure, or both, of any transaction described in the associated materials we provide to you, including, but not limited to, any tax opinions, memoranda, or other tax analyses contained in those materials. The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through consultation with your tax adviser.

Mastering Form 990 Schedule L: Reporting Transactions With Interested Persons PRESENTERS Frank Giardini, Principal – Grant Thornton, LLP Jennifer Becker Harris, Shareholder – Clark Nuber Michele Melchior, Director – Grant Thornton, LLP

Agenda Organization Governance, Policy and Form 990 Purpose of Schedule L Governance and board independence Conflicts of Interest Policy Reporting and Documentation Schedule L 2014 changes to interested persons 2016 guidance (substantial contributors) Parts I – IV: A practical over-view Circling back: Board Member Independence Questions 6

Organization Governance, Policy and Form 990 7

Governance and Form 990 Purpose of Schedule L 1. Provide information on certain financial transactions or arrangements between the exempt organization and "Disqualified Individuals". 2. Used to determine whether a member of the exempt organization's governing body or "Board" is independent 8

Governance and Form 990 Disqualified Person under IRC § 4958 include: 1. Current or former officers, trustees, directors and key employees 2. Create a Founder of Exempt Organizations 3. Substantial Contributor ($5,000 or more contributions per year) 4. A family member of any individual described above 5. A 35% controlled entity of one or more individuals/or organization described above. NOTE: A more detailed discussion of the application of IRC § 4958 will be made later in the presentation 9

Governance and Form 990 Observations: While certain policies may not be required by the Internal Revenue Code, the IRS has the authority to ask all of these questions. IRS sees a link between governance and tax compliance Answers contrary to conventional wisdom will likely create a negative impression Many questions require additional disclosures , explanations, and descriptions on Schedule O 10

Governance & Policy – Form 990 Board Member Independence Form 990 asks about 'voting' members and how many were 'independent' Lack of Independence of voting members is caused by: Compensation for services (as employee or officer) Compensation for service (as independent contractor) The member or his/her family member being disclosed on Schedule L of this or a related organization 11

Governance & Policy – Form 990 Conflict of Interest Form 990 asks about your conflict of interest (COI) policy Applicable to: Officers, Directors & Trustees, Key Employees Is it written ? Is there annual disclosure? Closely tied to Schedule L Key disclosure that is required in response to yes answer at 12c MUST read instructions for REQUIRED Schedule O disclosure elements Who COI policy covers How potential conflicts are monitored and disclosed Who is charged with review of and determining whether a conflict exists when a question exists, and What restrictions are effected in decision making when a conflict is determined to be present 12

Governance & Policy – Form 990 Conflict of Interest Policy content: Define conflicts of interest (COI) Identify who is covered (by class) Facilitate how to identify a COI (monitoring / questionnaires) Specify procedures to manage COI if identified Requires sufficient disclosures as to governing individual's or key employee's as well as family members' businesses and employment interest that may be related to the exempt organization Does your policy properly encompass the areas on Schedule L? Excess benefits Loans Grants or assistance Business Transactions including employment relationships 13

Governance & Policy – Form 990 Conflict of Interest What causes a conflict of interest? Person in authority (Officer, Director/Trustee, Key Employee or other manager) may benefit financially from the decision includes indirect benefits (family member / businesses / etc.) does not include competing duties to the same organization or another organization (such as serving on the board of both organizations) as long as it does not involve a material financial interest that could benefit the person 14

Governance & Policy – Form 990 Reporting and Documentation Policy enforcement: Who is responsible? Everyone! Self reporting Education is key Responsible parties for data gathering: Board: Governance committee (best), Executive committee or similar Management: Compliance officer, internal audit , other…. Other interested persons per Schedule L: Joint effort Also consider review of internal data (trial balance, loans, compensation, grants, contributions…..) – who will handle this? 15

Governance & Policy – Form 990 Reporting and Documentation Policy enforcement: Use of a COI questionnaire: Annual disclosure and sign off Be sure include schedule L disclosure areas Use to meet the Form 990 'reasonable efforts ' requirement Timing of the COI questionnaire? New board members and employees End of year (think retrospectively as well as prospectively) There were changes in 2014 to the definition of interested person Has your COI questionnaire been updated? 16

Governance & Policy – Form 990 Reporting and Documentation COI questionnaire & Schedule L 'Reasonable Efforts': Form 990 requires a 'reasonable' level of effort to obtain information on conflicts for Schedule L purposes Reasonable Efforts: Distribute a questionnaire to all interested persons (including those who 'may' be interested persons) Include pertinent definitions and instructions explaining potential types of transactions & listing who is considered an interested person Request disclosure and description from such persons describing the transaction Provide a place for name, title, date and signature If these 'reasonable efforts' are followed, then even if there is a transaction that should have been mentioned, but the interested person does not report it, the organization is clear 17

Schedule L Interested Persons - 2014 Changes 18

Schedule L – Transactions with Interested Persons Schedule L is all about In 2014 the definitions of interested persons for Parts II – IV were harmonized for consistency For example: All four parts now include 'substantial contributors' as interested persons Before we dive into Schedule L details……. 19

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.