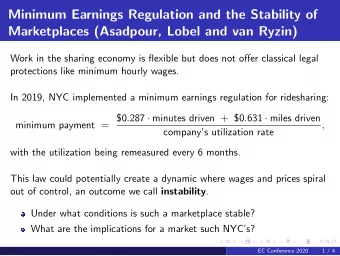

ECON 202: Macroeconomics I Lecture 18 - Review John Grigsby March - PowerPoint PPT Presentation

ECON 202: Macroeconomics I Lecture 18 - Review John Grigsby March 8, 2017 Grigsby Lecture 18 - Review March 8, 2017 1 / 33 Measurement Measurement 1 Finding Equilibrium 2 Growth 3 Solow Growth Neoclassical Growth Modern Growth

ECON 202: Macroeconomics I Lecture 18 - Review John Grigsby March 8, 2017 Grigsby Lecture 18 - Review March 8, 2017 1 / 33

Measurement Measurement 1 Finding Equilibrium 2 Growth 3 Solow Growth Neoclassical Growth Modern Growth Business Cycles 4 RBC Model Labor Markets 5 Labor Supply Frictions and Unemployment Inflation and Money 6 Baumol-Tobin CIA & Friedman Rule IS-LM Uncertainty and Asset Pricing 7 Grigsby Lecture 18 - Review March 8, 2017 2 / 33

Measurement Section 1 Measurement Grigsby Lecture 18 - Review March 8, 2017 2 / 33

Measurement Measuring GDP Nominal GDP calculated as sum of prices times quantities � GDP NOM = p it q it t i Only include goods sold to end users to avoid double counting Real GDP fixes prices at a particular point in time b � GDP REAL = p ib q it t i Chain-weighting (averaging subsequent time periods’) reduces substitution bias and better measures new products Grigsby Lecture 18 - Review March 8, 2017 3 / 33

Finding Equilibrium Section 2 Finding Equilibrium Grigsby Lecture 18 - Review March 8, 2017 4 / 33

Finding Equilibrium The Cookbook to find equilibrium 1 Write down household maximization problem 2 Write down household Lagrangean, take FOCs, solve for Marshallian Demand MRS = MRT 3 (If applicable) write down firm’s maximization problem. Unless explicitly stated, firm’s problem does not have constraint. 4 Write down FOCs, solve for input (a.k.a. factor) demands Marginal Revenue Product = Marginal Cost 5 Impose market clearing by equating supply and demand Grigsby Lecture 18 - Review March 8, 2017 5 / 33

Finding Equilibrium Permanent Income Hypothesis In the absence of frictions (e.g. consumers can borrow), fluctuations in consumption will be driven by fluctuations in permanent income, not transitory income Thus temporary shocks should not affect consumption greatly in the absence of large propagation mechanisms. Came from a problem like max c 0 , c 1 ln c 0 + β ln c 1 s . t . c 0 + b 1 = y 0 c 1 = y 1 + (1 + r ) b 1 to yield Euler equation u ′ ( c 0 ) β u ′ ( c 1 ) = 1 + r Grigsby Lecture 18 - Review March 8, 2017 6 / 33

Growth Section 3 Growth Grigsby Lecture 18 - Review March 8, 2017 7 / 33

Growth Empirics 1 Growth in per capita output of about 2% per year in the U.S. 2 Poorer countries converge to richer countries on average 3 Savings rate highly correlated with wealth 4 Innovation positively correlated with growth Grigsby Lecture 18 - Review March 8, 2017 8 / 33

Growth Solow Growth Solow Growth - Set up Output produced with capital and labor according to t L 1 − α Y t = A t K α t for Y t aggregate output (GDP), A t total factor productivity (TFP), K t capital, L t labor, and α the capital share in production Capital evolves according to law of motion: K t +1 = (1 − δ ) K t + I t for δ the (constant) depreciation rate of capital and I t investment Agents save a fixed share s of their income so that I t = sY t C t = (1 − s ) Y t Grigsby Lecture 18 - Review March 8, 2017 9 / 33

Growth Solow Growth Solow Growth - Dynamics Over time, converge to a steady state value of capital, output, and consumption. 1 � � sAL 1 − α 1 − α ¯ Y = A ¯ ¯ K α L 1 − α C = (1 − s ) ¯ ¯ K = Y δ If productivity or labor increasing, converge to steady state value of capital etc. per effective labor unit 1 � � s 1 − α ¯ Y = ¯ ¯ k = c = (1 − s )¯ ¯ k α y δ + g A + g L + g A g L for g A growth rate in productivity, g L growth rate of labor. Increases in savings rate will not lead to higher consumption unambiguously: have more stuff but eat less of it. Optimal s ∗ = α Only source of long run growth in per capita output: productivity Grigsby Lecture 18 - Review March 8, 2017 10 / 33

Growth Neoclassical Growth Neoclassical Growth Same premise as Solow, but people choose savings: Consumers solve ∞ � β t u ( c t ) t L 1 α max s . t . Y t = A t K α t { c t } ∞ t =0 t =0 K t +1 = (1 − δ ) K t + I t I t = Y t − c t Substitute constraints into each other to get t L 1 − α K t +1 = (1 − δ ) K t + A t K α − c t t Get Euler Equation a before. Savings rate is δα s = s ∗ = α ⇔ ρ = 0 s = ρ + δ ⇒ Grigsby Lecture 18 - Review March 8, 2017 11 / 33

Growth Modern Growth Modern Growth Growth only comes from increases in productivity This requires innovation/input improvements Knowledge is a public good Thus have strong intellectual property rights (patent law) Public goods tend to be underprovided relative to social optimum Grigsby Lecture 18 - Review March 8, 2017 12 / 33

Business Cycles Section 4 Business Cycles Grigsby Lecture 18 - Review March 8, 2017 13 / 33

Business Cycles Economic Fluctuations Cycles happen recurrently but not periodically Multiple indicators fall at the same time ⇒ Output, investment, consumption, wages, etc. Investment and other highly income elastic goods fluctuate more over the cycle People predict with leading indicators , including the yield curve. Need propagation mechanism to make small shock large People get poorer so invest less, have less capital, thus less output next period Granularity: shocks to large firms can have aggregate effects Network: shocks to highly connected sectors can have aggregate effects Grigsby Lecture 18 - Review March 8, 2017 14 / 33

Business Cycles RBC Model Real Business Cycles - Firms Firms solve t L 1 − α max L t , K t A t K α − w t L t − r t K t t so that w t = A t (1 − α ) L − α r t = A t α L 1 − α K α − 1 K α t t t t � �� � � �� � MP L MP K Grigsby Lecture 18 - Review March 8, 2017 15 / 33

Business Cycles RBC Model Real Business Cycles - Households Two generations: old and young Households solve ln c t t + ln c t c t max s . t . t + k t +1 = w t t +1 c t t , c t t +1 , k t +1 c t t +1 = (1 − δ ) k t +1 + r t +1 k t +1 Writing Lagrangean and FOC eventually yields k t +1 = w t 2 Higher w t ⇒ higher k t +1 ⇒ higher Y t +1 Grigsby Lecture 18 - Review March 8, 2017 16 / 33

Business Cycles RBC Model Equilibrium Labor market clearing implies L t = 1 Plug firms’ FOC into household maximization problem to get � A t (1 − α ) K α � t K t +1 = 2 If A t ↑ , w t ↑ , K t +1 ↑ Define I t = K t +1 − (1 − δ ) K t , C t = Y t − I t . Plugging in for Y t = A t K α t , K t +1 , take derivative with respect to A t to get elasticity: ǫ IA > 1 > ǫ CA so investment moves more than consumption through the cycle Grigsby Lecture 18 - Review March 8, 2017 17 / 33

Business Cycles RBC Model Dynamics 1 A t ↓ so labor and capital demand falls 2 w t ↓ and r t ↓ 3 K t +1 ↓ 4 A t +1 rebounds, so labor and capital demand rebound 5 Lower K t +1 implies lower marginal product of labor, so wage doesn’t rebound all the way 6 Lower K t +1 and old labor supply means r t +1 jumps above old steady state Grigsby Lecture 18 - Review March 8, 2017 18 / 33

Labor Markets Section 5 Labor Markets Grigsby Lecture 18 - Review March 8, 2017 19 / 33

Labor Markets Labor Supply Labor Supply Labor supply comes from people trading off leisure and consumption Two forces when wages rise: Substitution effect: higher wage makes labor more expensive ⇒ work 1 more Income effect: higher wage means higher income; leisure normal good 2 ⇒ work less If leisure and consumption substitutes, strong substitution effect ⇒ upward-sloping labor supply If leisure and consumption complements, weak substitution effect ⇒ downward-sloping labor supply (possibly) Short run changes in wages do not affect permanent income ⇒ small income effect Grigsby Lecture 18 - Review March 8, 2017 20 / 33

Labor Markets Labor Supply Size of effects Income Substitution Slope of Uncompensated Effect Effect Labor Supply Permanent w ↑ Large ? Less positive Temporary w ↑ Small ? More positive c , l substitutes ? Large More positive c , l complements ? Small Less positive Grigsby Lecture 18 - Review March 8, 2017 21 / 33

Labor Markets Labor Supply Labor Supply Shifters Non-labor income ↑ shifts labor supply in Taxes: unclear as makes people poorer but leisure cheaper Population growth: add more supply curves together Increased value of leisure (e.g. improved leisure technology) Laffer Curve: revenue maximizing income tax does not equal 0 or 1. Grigsby Lecture 18 - Review March 8, 2017 22 / 33

Labor Markets Frictions and Unemployment Unemployment comes from frictions Wage stickiness Search and matching frictions Individuals need time to find a job Suppose a fraction λ of unemployed U t find a job each period A fraction δ of employed lose their job each period Yields law of motion U t +1 = (1 − λ ) U t + δ E t Divide by L , get u t +1 = (1 − λ ) u t + δ (1 − u t ) At steady state, natural unemployment rate is δ u n = δ + λ > 0 Grigsby Lecture 18 - Review March 8, 2017 23 / 33

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.