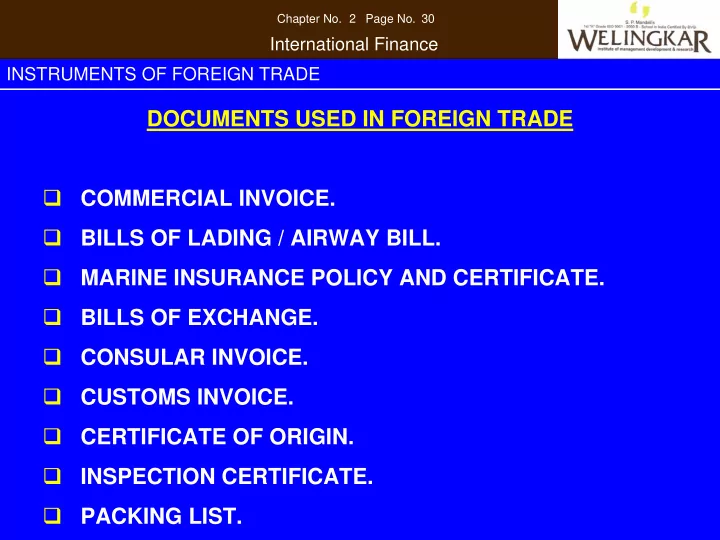

Chapter No. Page No. 2 30 International Finance INSTRUMENTS OF FOREIGN TRADE DOCUMENTS USED IN FOREIGN TRADE � COMMERCIAL INVOICE. � BILLS OF LADING / AIRWAY BILL. � MARINE INSURANCE POLICY AND CERTIFICATE. � BILLS OF EXCHANGE. � CONSULAR INVOICE. � CUSTOMS INVOICE. � CERTIFICATE OF ORIGIN. � INSPECTION CERTIFICATE. � PACKING LIST.

Chapter No. Page No. 2 30 International Finance INSTRUMENTS OF FOREIGN TRADE BILL OF LADING ( B / L ) � IT IS THE MOST IMPORTANT DOCUMENT IN FOREIGN TRADE. � IT IS A DOCUMENT OF TITLE TO THE GOODS. � IT IS A RECEIPT FROM THE SHIPPING COMPANY. � IT IS AN EVIDENCE OF TRANSPORTATION OF GOODS.

Chapter No. Page No. 2 31 International Finance INSTRUMENTS OF FOREIGN TRADE TYPES BILL OF LADING � FREIGHT PAID AND FREIGHT COLLECT : IF THE SALE OF GOODS IS ON “c.i.f.”, TERMS THE EXPORTER MUST PAY THE FRIGHT AND GET A FREIGHT PAID BILL OF LADING. AND IF THE SALE IS ON “f.o.b.”, TERMS THE FREIGHT IS NOT PREPAID THEN THE BILL IS CALLED FREIGHT COLLECT BILL OF LADING. THE FREIGHT IS COLLECTED FROM THE IMPORTER. � CLEAN VS. CLAUSED BILL OF LADING: B / L MUST BE CLEAN. IT MEANS NO ADVERSE NOTATION OF ANY KIND MUST APPEAR ON IT WITH REGARD TO THE APPARENT ORDER AND CONDITION OF GOODS. IF THE GOODS SHOW SIGN OF DAMAGE B / L CONTAINS AN ENDORSEMENT TO THIS EFFECT. THIS IS A CLAUSED B / L. CONT….

Chapter No. Page No. 2 32 International Finance INSTRUMENTS OF FOREIGN TRADE TYPES BILL OF LADING � THROUGH BILL OF LADING :WHERE THERE IS NO DIRECT SHIPPING LINK BETWEEN SELLER’S AND BUYER’S PORT, AND THE TERMS OF SALE IS c.i.f. BUYER’S PORT THE EXPORTER WILL ARRANGE TO GET B / L TO ENSURE NECESSARY THROUGH TRANSSHIPMENT AND SUBSEQUENT CARRIAGE BY A SECOND VESSEL FROM THE INTERMEDIARY PORT. � TRANSMISSION OF THE BILL OF LADING TO IMPORTER: BILLS OF LADING ARE MADE OUT IN SETS HAVING NUMBER OF COPIES AS PER THE REQUIREMENTS OF THE PARTICULAR TRANSACTION AND THE IMPORTER. IT IS IMPORTANT THAT THE FULL SET OF B/L TOGETHER BE PRESENTED BY THE SHIPPER TO THE BANK.

Chapter No. Page No. 2 32 International Finance INSTRUMENTS OF FOREIGN TRADE TYPES BILL OF LADING � CHARTER PARTY BILL OF LADING : FOR THE TRANSPORT OF BULK CARGOES, A SHIPPER OR A GROUP OF SHIPPER MAY LEASE A VESSEL FOR A PARTICULAR TRIP OR A ROUND OF TRIPS OR FOR A SPECIFIED PERIOD OF TIME. THE B / L ISSUED BY THE PARTY, WHICH LEASES OR CHARTERS TO THIRD PARTY SHIPPERS IS CALLED A CHARTER PARTY B / L.

Chapter No. Page No. 2 33 International Finance INSTRUMENTS OF FOREIGN TRADE AIRWAY BILL � IT IS AN ACKNOWLEDGEMENT ISSUED BY AN AIRLINE COMPANY OR THEIR AUTHORIZED AGENT. � AIRWAY BILL IS NOT A DOCUMENT OF TITLE TO GOODS. � IT IS NOT A NEGOTIABLE DOCUMENT. � IT IS NOT NECESSARY FOR A CONSIGNEE TO POSSESS THE AIRWAY BILL FOR TAKING DELIVERY OF GOODS. � FOR A SHIPPER THE AIRWAY BILL IS NOT AS SAFE A DOCUMENT AS A BILL OF LADING. � HOUSE AIRWAY BILL IS A RECEIPT FOR GOODS ISSUED NOT BY THE ACTUAL CARRIERS OR THEIR AGENTS BUT AN INTERMEDIARY CARGO CONSOLIDATING AGENT.

Chapter No. Page No. 2 33 International Finance INSTRUMENTS OF FOREIGN TRADE MARINE INSURANCE POLICY � IF THE TERMS OF SALE ARE c.i.f OR c.i. THE INSURANCE WILL BE TAKEN BY THE EXPORTER. � IF THE TERMS OF SALE ARE f.o.b. THE INSURANCE WILL BE TAKEN ON ACCOUNT OF THE OVERSEAS BUYER. � THE USUAL PRACTICE IN INTERNATIONAL TRADE IS TO COVER THE GOODS FOR FULL c.i.f. VALUE PLUS 10%. � A MARINE POLICY CAN BE TAKEN EITHER BY AN OPEN POLICY OR A SPECIFIC POLICY. � RISKS COVERED ARE : PERILS OF THE SEA, FIRE, PIRACY, JETTISONING, BARRATRY, PERILS OF WAR, THEFT, PILFERAGE, EXPLOSION, DAMAGE TO MACHINERY, BREAKAGES, LEAKAGES, HEATING etc.

Chapter No. Page No. 2 36 International Finance INSTRUMENTS OF FOREIGN TRADE CLAIMS � IN THE EVENT OF ANY LOSS OF OR DAMAGE TO THE INSURED GOODS, AS PER THE PROVISIONS OF THE CARRIAGE OF GOODS BY SEA ACT OF 1925. DOCUMENTS TO BE SUBMITTED FOR CLAIMS � THE INSURANCE POLICY. � THE ORIGINAL INVOICE AND THE PACKING LIST. � A COPY OF THE BILL OF LADING. � COPIES OF CORRESPONDENCE WITH THE SHIPPING COMPANY. � TIME LIMIT FOR FILING A SUIT AGAINST THE SHIPPING COMPANY IS ONE YEAR.

Chapter No. Page No. 2 37 International Finance INSTRUMENTS OF FOREIGN TRADE BILL OF EXCHANGE � IT IS AN UNCONDITIONAL ORDER IN WRITING, ADDRESSED BY THE DRAWER TO THE DRAWEE REQUIRING THE DRAWEE TO PAY ON DEMAND A STATED SUM OF MONEY TO THE BEARER / SPECIFIED PERSON OR ORGANIZATION. � A BILL OF EXCHANGE IS A NEGOTIABLE INSTRUMENT. � IN INTERNATIONAL TRADE THE NORMAL PRACTICE IS TO SEND DOCUMENTS IN TWO SETS, AS WELL AS BILL OF EXCHANGE.

Chapter No. Page No. 2 37 International Finance INSTRUMENTS OF FOREIGN TRADE TYPES OF BILL OF EXCHANGE � CLEAN AND DOCUMENTARY BILLS: A CLEAN BILL IS NOT ACCOMPANIED BY THE RELATIVE SHIPPING DOCUMENTS. AFTER THE SHIPMENT THE DOCUMENTS ARE SENT DIRECTLY TO THE IMPORTER AND THE BILLS ARE SENT TO THE BANK FOR COLLECTING THE PAYMENT. DOCUMENTARY BILL IS ACCOMPANIED BY THE RELATIVE SHIPPING DOCUMENTS. � SIGHT & USANCE BILLS: A SIGHT BILL IS PAYABLE “AT SIGHT” OR DEMAND OR ON PRESENTATION, AND A USANCE BILL IS REQUIRED TO BE PAID WITHIN THE PERIOD SPECIFIED. � D/P & D/A BILLS: (DOCUMENTS ON PAYMENT & DOCUMENTS ON ACCEPTANCE).

Chapter No. Page No. 2 37 International Finance INSTRUMENTS OF FOREIGN TRADE CONSULAR INVOICE � IT IS A SPECIAL TYPE OF INVOICE REQUIRED FOR THEIR IMPORTS BY SOME COUNTRIES SUCH AS U.S.A. , CANADA, PHILIPPINES AND SOME MIDDLE EAST COUNTRIES. � A CONSULAR INVOICE IS MADE OUT ON A PRESCRIBED FORMAT CERTIFIED BY THE CONSULATE OF THE IMPORTING COUNTRY STATIONED IN THE EXPORTER’S COUNTRY. � IMPORTING COUNTRY WANTS TO HAVE AUTHENTICATED PARTICULARS OF THE GOODS THAT ARE IMPORTED INTO THEIR COUNTRY.

Chapter No. Page No. 2 38 International Finance INSTRUMENTS OF FOREIGN TRADE CUSTOMS INVOICE � CERTAIN COUNTRIES SUCH AS CANADA AND U.S.A. NEED CUSTOMS INVOICE. CANADA HAS PRESCRIBED A SPECIFIC FORM OF CUSTOMS INVOICE FOR ALLOWING ENTRY OF MERCHANDISE AT PREFERENTIAL TARIFF RATES.

Chapter No. Page No. 2 38 International Finance INSTRUMENTS OF FOREIGN TRADE CERTIFICATE OR ORIGIN � IN MANY COUNTRIES, PERMISSION TO IMPORT IS REFUSED UNLESS A CERTIFICATE OF ORIGIN IS PRODUCED BY THE BUYER. � IT MAY FORM THE PART OF INVOICE ITSELF. � THE ESSENTIAL FEATURE IS CERTIFICATION OF THE COUNTRY OF ORIGIN INDICATING WHERE THE GOODS WERE ORIGINALLY PRODUCED. � THERE MAY BE PREFERENTIAL TARIFF IN FAVOUR OF GOODS FROM PARTICULAR COUNTRIES. � A CERTIFICATE MAY BE NEEDED WHERE GOODS OF A PARTICULAR TYPE FROM CERTAIN COUNTRIES ARE BANNED.

Chapter No. Page No. 2 38 International Finance INSTRUMENTS OF FOREIGN TRADE INSPECTION CERTIFICATE � INSPECTION CERTIFICATE BY AN ESTABLISHED INSPECTION AUTHORITY IS NEEDED UNDER SOME CONTRACTS OR BY SOME COUNTRIES. � THIS CERTIFICATE IS ISSUED BY ONE OF THE AUTHORIZED INSPECTION AGENCIES IN THE EXPORTER’S COUNTRY BY THE AGENCY NOMINATED BY THE IMPORTER.

Chapter No. Page No. 2 38 International Finance INSTRUMENTS OF FOREIGN TRADE PACKING LIST IT SHOULD GIVE � ITEM BY ITEM, THE CONTENTS OF THE CONTAINERS. � THE DESCRIPTION OF THE GOODS. � NUMBER AND MARKS ON THE PACKAGES. � QUANTITY PER PACKAGE. � NET WEIGHT AND GROSS WEIGHT. � MEASUREMENT.

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries