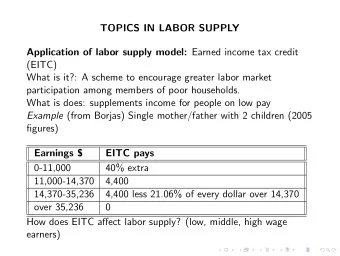

Classical Labor Supply: Partial Insurance ECON 34430: Topics in - PowerPoint PPT Presentation

Classical Labor Supply: Partial Insurance ECON 34430: Topics in Labor Markets T. Lamadon (U of Chicago) Winter 2016 Heathcote Storesletten and Violante (2013) Consumption and Labor Supply with Partial Insurance Intro HSV 2013 The paper

Classical Labor Supply: Partial Insurance ECON 34430: Topics in Labor Markets T. Lamadon (U of Chicago) Winter 2016

Heathcote Storesletten and Violante (2013) Consumption and Labor Supply with Partial Insurance

Intro HSV 2013 • The paper wants to answer 3 broad questions: 1 Fraction of individual shocks that transmits to consumption 2 Insurability nature of the recent increase in US inequality 3 Life-cylce shocks vs initial conditions in determining inequality

Intro HSV 2013 • To do so they develop an island model • two sources of permanent shocks: island level and individual • allow for certain insurance claimed to be traded within and between • solve for the equilibrium, show that close form solution exist • estimate on data

The Model: preferences HSV 2013 • perpetual youth model, constant survival probability δ • the economy is composed of an infinite number of individuals in an infinite number of islands • preferences over consumption and hours ∞ � ( βδ ) t − b u ( c t , h t ; φ ) E b t = b u ( c t , h t ; φ ) = c 1 − γ − exp ( φ ) h 1+ σ − 1 t t 1 − γ 1 + σ • cohort born at time t draws φ t ∼ F φ t

The Model: productivity HSV 2013 • productivity is composed of an idiosyncratic and island specific components: log w t = α t + ǫ t ���� ���� island ind. • the island level follows a random walk α t = α t − 1 + ω t with ω t ∼ F ω t • the individual component is formed by a random walk and an iid transitory ǫ t = κ t + θ t with θ t ∼ F θ t κ t = κ t − 1 + η t with η t ∼ F η t • agents entering at time t draw α 0 , κ 0 , φ from cohort specific distributions

The Model: production and taxes HSV 2013 • large number of individual and island means no aggregate uncertainty • production of the final good takes place through a constant return to scale technology → individuals are paid their productivity • given gross income y t = w t h t net earnings are given by: y t = λ ( y t ) 1 − τ ˜ • this achieves some redistribution and approximates the US tax system

The Model: market structure HSV 2013 • all assets are in 0 net supply • at birth agents have 0 financial asset • α 0 and φ are drawn before trading starts • agents are attached to an island with unknown ω t realized sequence • within island, agents can trade a complete set of insurance contracts - at t ≥ b they can trade s t +1 = ( ω t +1 , η t +1 , θ t +1 ) - contracts pay δ − 1 unit of consumption in state s t +1 • between island, more limited - at t ≥ b they can trade s t +1 = ( η t +1 , θ t +1 ) - can’t condition on ω t +1 • note that agents can trade a risk free bond by buying δ of each ( η t +1 , θ t +1 ) contracts

The Model: agent’s problem HSV 2013 • call s t = s b , s b +1 , ... s t the individual history of shocks � ( b , φ, α 0 , κ 0 , θ b ) for j = b s j = ( ω j , η j , θ j ) for j > b • Q t ( S ; s t ) is price of insurance bought at time t by agent with s t for event set S ⊆ S . • B t ( s t +1 ; s t ) is the quantity purchased t ( Z ; s t ) and B ∗ t ( z t +1 ; s t ) are equivalent for price and • Q ∗ quantity for agents from other islands. • Z and z do not include ω .

The Model: agent’s budget constraints HSV 2013 � 1 − τ + d t ( s t ) = c t ( s t ) � w t ( s t ) h t ( s t )) λ � Q t ( s t +1 ; s t ) B t ( s t +1 ; s t ) ds t +1 + S � t ( z t +1 ; s t ) B ∗ t ( s t +1 ; s t ) dz t +1 + Q ∗ Z where the realized wealth is given by d t ( s t ) = δ − 1 � � B t − 1 ( s t ; s t − 1 ) + B ∗ t − 1 ( z t ; s t − 1 )

The Model: equilibrium HSV 2013 • Given sequences { F φ t , F α 0 t , F κ 0 t , F ω t , F η t , F θ t } a competitive equilibrium is a set of allocations { c t ( s t ) , h t ( s t ) , d t ( s t ) , B t ( · , s t ) , B ∗ t ( · , s t ) } and prices { B t ( · , s t ) , B ∗ t ( · , s t ) } such that 1 allocation maximize expected utility 2 insurance markets clear 3 final good and labor market clear • oveview of the results: 1 no bond traded in equilibrium between islands 2 close form solution for hours and consumption 3 close form solution for insurance claims prices 4 sharp dichotomy between individual shocks and island shocks

Main result HSV 2013 • No insurance trade between islands B ∗ T ( Z ; s t ) = 0 for all Z • Consumption and hours are given by: φ + (1 − τ )1 + ˆ σ log c t ( s t ) = − (1 − τ )ˆ σ + γ α t + C a t ˆ φ + 1 − γ σ + γ α t + 1 log h t ( s t ) = − ˆ σǫ t + H a t ˆ ˆ σ ˆ where C a t and H a t are age-date specific constant, ˆ φ are tax-modified constants. • bond prices are given by where ∆ C a t is independent of a and F st integrates over ( ω, η, θ )

Intuition behind no trade HSV 2013 • first, agents can trade a risk free bond across island if they want to • however they all value this bond in the same way, why? - multiplicative and i.i.d. structure makes claim price history independent - the idiosyncratic part ( η t , θ t ) is perfectly insured within island, - the common part ω t is shocking everyone within island - the island shock ω t can’t be traded across Island - the island level shocks are the same in all Islands • nevertheless, we get an environment with labor supply, insurable and no insurable shocks, and every thing in close form.

Intuition behind asset no entering the state space HSV 2013 • within island, allocation can be derived using the planner solution (no reference to individual asset position) • yet asset holding is non-degenerate • between island, we have the no-trade outcome

Consumption and Labor Supply Decisions HSV 2013 φ + (1 − τ )1 + ˆ σ log c t ( s t ) = − (1 − τ )ˆ σ + γ α t + C a t ˆ φ + 1 − γ σ + γ α t + 1 log h t ( s t ) = − ˆ σǫ t + H a t ˆ ˆ • hours and ǫ t = κ t + θ t - hours work is increasing in the insurable component ǫ t - the response is scaled by the Frisch elasticity - insurability of ǫ rules out income effect • hours and α t - γ > 1 means income effect dominates substitution: hours ց • consumption is independent of ǫ t because it is fully insured - consumption follows a random walk - pass-through depends on σ , γ and tax-schedule

Data and estimation HSV 2013 • Use a combination of CEX and PSID • Use PSID with fine age groups for - moments in level involving hours and wages - same moments in difference - same moments in second difference • Use CEX with fine age groups for - moments in level involving consumption • estimate parameters using minimum distance ( 11 , 532 moments and 164 parameters)

Some Moments HSV 2013

More Moments HSV 2013

Parameter estimates HSV 2013 • δ = 0 . 996 and τ = 0 . 185 ( R 2 = 0 . 92 ) • 1 / ˆ σ = 0 . 35 broadly consistent with the litterature • 45% of permanent innovation appears to be insurable

Passthrough coefficient HSV 2013 • pass-through from permanent wage shocks to consumption • progressive taxation 0 . 815 • labor supply 0 . 845 • private insurance 0 . 63 • overall φ w , c = 0 . 386 t • the pass-through from pre-tax earnings is 0 . 272 , very similar to Blundell, Pistaferri and Preston which found 0 . 225

Wages and consumption growth variance HSV 2013 • the ratio of consumption growth to wage growth: • we see even more smoothing due to taxes and labor supply here • at baseline, increase in variance of consumption is 25% of increase in log-wages even though 40% of wage shocks transmit to consumption.

Life cycle variance decomposition HSV 2013 • initial heterogeneity accounts for 40% to 50% for all variables • insurable versus uninsurable differ for different variables • no simple answer, depends on var of interest • when simulating life-time earnings, they find that initial conditions account for 63% of the dispersion

Conclusion HSV 2013 • developed a micro-founded very tractable model of partial insurance • includes labor-supply decision • close form consumption and hours • do we learn more than BPP? • how realistic/useful is the market structure?

Arellano, Blundell, Bonhomme (WP) Earnings and Consumption Dynamics: A Nonlinear Panel Data Framework

Model for earnings ABB WP • Earnings follow: y it = η it + ǫ it η it = Q t ( η i , t − 1 , u it ) • note that unit root is a particular case: η it = η i , t − 1 + F − 1 ( u it ) • Estimation and identification: - identification is akin Hidden Markov Chains - estimation is akin the EM but - latent variable is continuous and dim ≥ 1 - uses Gibbs sampling in the E-step - uses quantile regression in the M-step (not strictly likelihood)

Non-linear dynamics ABB WP • the paper allows for the persistence of the sock to differ at different quantiles ρ t ( η i , t − 1 , τ ) = ∂ Q t ( η i , t − 1 , τ ) ∂η • the persistence of η can differ depending on the values of η and the shock u . • the model allows for conditional skewness and conditional kurtosis. • in the unit root model ρ = 1 everywhere.

Results - Earning process ABB WP

Results - Error terms ABB WP

Results - Earning process - conditional skewness ABB WP

Results - Earning process - conditional skewness mobility

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.