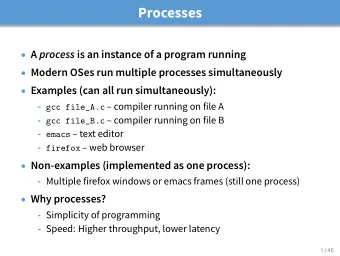

Chapter 4: Video 1 - Supplemental slides

The Autoregressive Model Autoregressive (AR) processes Let ǫ 1 , ǫ 2 , . . . be White Noise(0, σ 2 ǫ ) innovations, with variance σ 2 ǫ Then, Y 1 , Y 2 , . . . is an AR process if for some constants µ and φ , Y t − µ = φ ( Y t − 1 − µ ) + ǫ t • We focus on 1st order case, the simplest AR process

AR Processes Autoregressive (AR) processes Y t − µ = φ ( Y t − 1 − µ ) + ǫ t • µ is the mean of the { Y t } process • If φ = 0 , then Y t = µ + ǫ t , such that Y t is White Noise( µ, σ 2 ǫ ) • If φ � = 0 , then observations Y t depend on both ǫ t and Y t − 1 • And the process { Y t } is autocorrelated • If φ � = 0 , then ( Y t − 1 − µ ) is fed forward into Y t • φ determines the amount of feedback • Larger values of | φ | result in more feedback

AR Processes: Properties If | φ | < 1 , then E ( Y t ) = µ σ 2 ǫ σ 2 Var ( Y t ) = Y = 1 − φ 2 ρ ( h ) = φ | h | Corr ( Y t , Y t − h ) = for all h • If µ = 0 and φ = 1 , then Y t = Y t − 1 + ǫ t which is a random walk process, and { Y t } is NOT stationary

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries

![Autoregressive Models Autoregressive Models In [1]: from mxnet import autograd, nd, gluon, init](https://c.sambuz.com/996111/autoregressive-models-autoregressive-models-s.webp)

![MARKDOWN SLIDES [EN] MARKDOWN SLIDES [EN] MARKDOWN SLIDES [EN] MARKDOWN SLIDES [EN] MARKDOWN](https://c.sambuz.com/818511/markdown-slides-en-markdown-slides-en-markdown-slides-en-s.webp)