Basics Bond issuers Javier Estrada Federal/state/local - PDF document

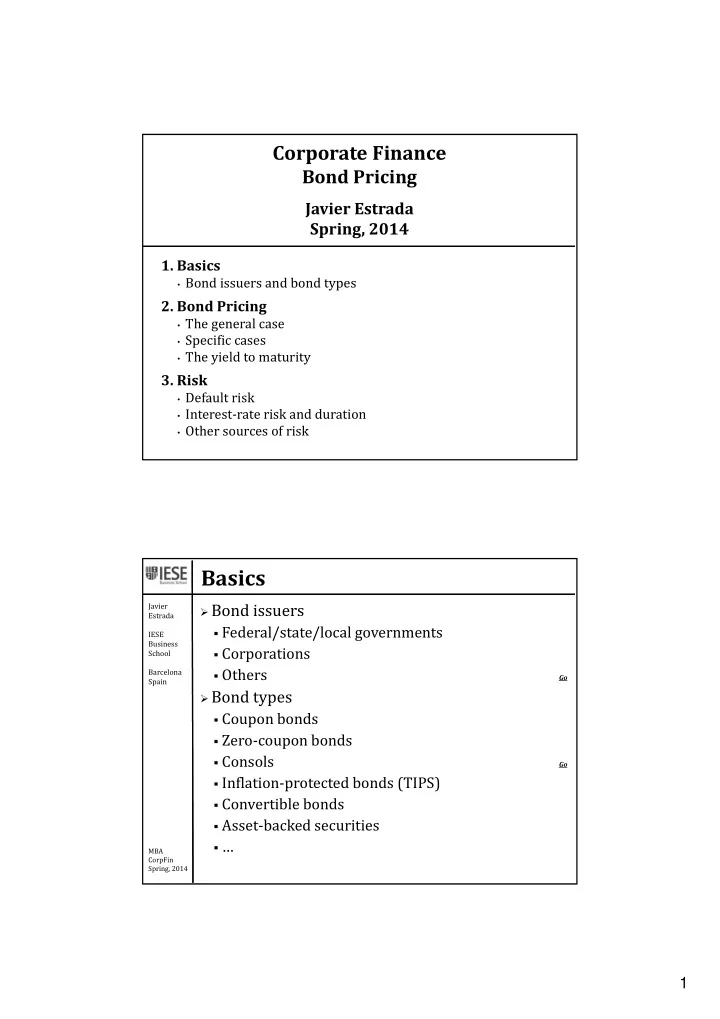

Corporate Finance Bond Pricing Javier Estrada Spring, 2014 1. Basics Bond issuers and bond types 2. Bond Pricing The general case Specific cases The yield to maturity 3. Risk Default risk Interestrate risk and duration

Corporate Finance Bond Pricing Javier Estrada Spring, 2014 1. Basics • Bond issuers and bond types 2. Bond Pricing • The general case • Specific cases • The yield to maturity 3. Risk • Default risk • Interest‐rate risk and duration • Other sources of risk Basics Bond issuers Javier Estrada Federal/state/local governments IESE Business Corporations School Others Barcelona Go Spain Bond types Coupon bonds Zero‐coupon bonds Consols Go Inflation‐protected bonds (TIPS) Convertible bonds Asset‐backed securities … MBA CorpFin Spring, 2014 1

Pricing – The General DCF Model Javier Estrada IESE Business School Beginning from the general DCF model Barcelona Spain Expected cash flows • ‘Certain’ cash flows (Coupons and principal) • Typically with finite maturity ( T ) Discount rate • R = R f + RP R f : Compensates the expected loss of purchasing power RP : Compensates risk bearing → RP = f ( Default risk, Interest ‐ rate risk, …) → There may be many other sources of risk MBA Go CorpFin Spring, 2014 Pricing – General and Special Cases Coupon bond Javier Estrada IESE Business School Barcelona Spain Zero‐coupon bond Zeros always trade at a discount Consols MBA CorpFin Spring, 2014 2

What Is the ‘Current’ Situation? Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 GoXls The Yield to Maturity (YTM) Javier Estrada IESE Business Definition School Barcelona Annualized return from buying the bond at the Spain market price ( p 0 ) and holding it until maturity ( T ) • The bond’s internal rate of return ‘Causality’ of the expression Note what are the inputs and outputs in each case • Pricing: C , P , and R are inputs / p 0 is the output • YTM: C , P , and p 0 are inputs / y is the output MBA CorpFin Spring, 2014 3

The Yield to Maturity Elaborating … Javier Estrada YTM v . interest rate IESE Business Annual YTM v . Effective annual YTM School Barcelona Yield curve Spain • Relationship between YTM and maturity • Typically refers to (risk‐free) government bonds Go Current yield • ‘Quick and dirty’ YTM • Similar to the dividend yield for stocks Back to YTMs in the case, a critical question: • What do the differences in yields reflect? Go MBA CorpFin Spring, 2014 Default (Credit) Risk Issues Javier Estrada How is default risk typically assessed? IESE Business Credit ratings School Barcelona • Investment‐grade bonds v . High‐yield (junk) bonds Spain • Key drivers • AAA status • Reliability Go MBA CorpFin Spring, 2014 4

Interest ‐ Rate (Market) Risk Issues Javier Estrada Definition IESE Business Estimation School GoXls Barcelona A basic but critical point Spain • The negative relationship between interest rates and bond prices Hence about inflation and prices Go Two questions • What is the main determinant of interest‐rate risk? Go • Any way to assess it simpler than what we did? Is there any variable that an individual, unsophisticated investor could use to quickly assess this risk? MBA CorpFin Spring, 2014 Interest ‐ Rate Risk – Duration Javier Estrada IESE Business School Two definitions Barcelona Spain 1. Related to when CFs are received (Expressed in years ) • Weighted‐average time to receive a bond’s cash flows Weights: Proportion of PV received in each period GoXls 2. Related to interest‐rate risk (Expressed in percent ) • Sensitivity of a bond’s price to a 1% change in the interest rate Go MBA CorpFin Spring, 2014 5

Appendix Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Bond Issuers Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Back 6

Consols Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Very Long ‐ Term Bonds Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Back 7

Liquidity Risk Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Back Even the Safest Bonds Are Risky! Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 8

Even the Safest Bonds Are Risky! Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 YTMs and Risk Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Back 9

Ratings – Scales Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Ratings – Key Drivers Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 10

Ratings – AAA Status Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Ratings – AAA Status Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 11

Ratings – AAA Status Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Ratings – AAA Status Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 12

Ratings – Reliability Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Ratings – Reliability Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 13

Ratings – Reliability Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Ratings – Reliability Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 14

Ratings – Reliability Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Ratings – Reliability Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Back 15

Interest Rates and Bond Prices Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Back Maturity and Interest ‐ Rate Risk Javier Estrada $1,102.7 $1,064.2 IESE $1,038.9 Business School Barcelona Spain $963.0 $941.1 $913.1 MBA CorpFin Spring, 2014 16

Maturity and Interest ‐ Rate Risk Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Back Duration and Interest ‐ Rate Risk Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 17

Duration and Interest ‐ Rate Risk Javier Estrada IESE Business School Barcelona Spain MBA CorpFin Spring, 2014 Back 18

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.