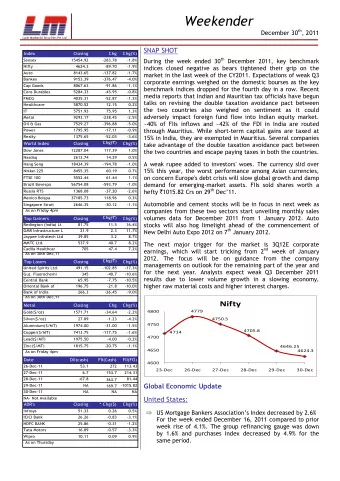

3Q10 Results FLRY3 The most valuable brand in the Brazilian - PowerPoint PPT Presentation

3Q10 Results FLRY3 The most valuable brand in the Brazilian healthcare industry The 6th most valuable brand among the service companies The 25th most valuable Brazilian brand Millward Brand / BrandAnalytics The Company of the Year

3Q10 Results FLRY3 “ The most valuable brand in the Brazilian healthcare industry The 6th most valuable brand among the service companies The 25th most valuable Brazilian brand ” Millward Brand / BrandAnalytics “The Company of the Year” “ Gestão RH” magazine 1st in the sector Financial Sustainability and Corporate Governance “ Istoé Dinheiro ” magazine 1st in the sector Value Generation and Margin from Operations “Valor 1000 ” magazine November, 2010 TODOS OS DIREITOS RESERVADOS – 2010

Disclaimer This presentation may contain forward-looking statements. Such statements are not statements of historical facts and reflect the beliefs and expectations of the Company s management. The words “anticipates”, “believes”, “estimates”, “expects”, “forecasts”, “plans”, “predicts”, “project”, “targets” and similar words are intended to identify these statements, which necessarily involve known and unknown risks and uncertainties. Known risks and uncertainties include but are not limited to the impact of competitive services and pricing market acceptance of services, service transactions by the Company and its competitors, regulatory approval, currency fluctuations, changes in service mix offered, and other risks described in the Company s registration statement. Forward-looking statements speak only as of the date they are made and the Fleury Group does not undertake any obligation to update them in light of new information or future developments. All mentioned comparisons are against the same period in 2009 – 3Q09 - except when stated differently.

Highlights Fleury Group growth rate accelerates to 20.7% YoY. EBITDA expands to R$ 60 million (25.9% margin). Net Income reaches R$ 44.6 million (19.2 margin), year to date achieves R$ 100 million. During 2010, 60 PSCs will receive some form of intervention in order to be better prepared to meet increasing demand and improve the Group´s asset usage efficiency. In 2011 the number of PSCs under intervention will be lower (40) but total area (m 2 ) in scope will be 3 times larger than 2010 (including 17.500 m 2 of additional space). More details about 2010 / 2011 CapEx will be presented later in this presentation. 3

Gross Revenue Evolution (R$ million) Organic growth has achieved 11.9% 24.0% growth excluding discontinued operations and Lab-to-Lab services portfolio review. 4

Gross Revenue - Breakdown Patient Service Centers, a 19.6% increase in revenues. 68.6% growth in Diagnostic Operations in Hospitals. Preventive Medicine (ex-FHD) has increased by 45.9%. Gross Revenue breakdown by business line 3Q10 3Q09 r R$ million % R$ million % Patient Service Centers 208.0 83.7% 173.9 84.5% 19.6% Diagnostic Operations in Hospitals 25.8 10.4% 15.3 7.4% 68.6% Lab-to-lab and Clinical Trials 9.6 3.9% 10.6 5.1% -9.3% Lab-to-lab 8.7 3.5% 8.6 4.2% 1.8% Clinical Trials 0.9 0.4% 2.0 1.0% -56.5% Preventive Medicine 5.1 2.1% 6.0 2.9% -14.7% Preventive Medicine (ex-FHD) 5.1 2.1% 3.5 1.7% 45.9% Fleury Hospital-Dia (Day-Hospital) 0.0 0.0% 2.5 1.2% -100% 5

Patient Service Centers 19.6% increase in gross revenue (15.9% in 9M10), amounting R$ 208 million in the quarter. The average revenue per square meter grew 13.4%. The average revenue per PSC grew 10.2%. Expansion in the number of patients by 15.6% compared to 3Q09. “Same store sales” (only same existing PSCs during the comparison period), has grown 12%. Average revenue per square meter and Average revenue per PSC total square meters (R$ million) Number of PSCs 6

Diagnostic Operations in Hospitals A 68.6% increase in the 3Q10 compared to the 3Q09, achieving R$ 26 million , 10.4 share in the total revenue of Fleury Group due to: Organic Growth – volume and mix have been improving significantly, a consequence from the strong demand over the past 12 months; The acquisition of Weinmann brought 2 leading hospitals in Rio Grande do Sul. The acquisition of Di enabled the expansion of partnership with Hospital Alemão Oswaldo Cruz (São Paulo). Number of tests and average revenue per test Thousands and R$ Average revenue per test Number of tests 7

Lab-to-Lab and Clinical Trials 1.8% variation in the 3Q10 compared to 3Q09 in Lab-to-Lab, R$ 8.7 million in the quarter . There was a 0.7% increase compared to the previous quarter. Progressive discontinuation of the Clinical Trials business. The R$ 2.0 million revenue of the 3Q09 decreased to R$ 0.9 million in the 3Q10. The total revenue considering both business lines decreased 9.3%. Number of tests and average revenue per test (ex-Clinical Trials) (Thousands and R$) Average revenue per test Number of tests 8

Gross Revenue – breakdown by type of test Imaging tests & Other Diagnostic Specialties increased 17.5%, driven by continuous organic expansion of Imaging Services in the PSCs and mix improvement. +7% in number of tests. Clinical Analysis’ revenue grew 24.9%, mainly driven by Operations in Hospitals and Weinmann’s acquisition. +27.9% in number of tests. Breakdown in PSCs: 14,4% Organic growth in Imaging tests & Other Specialties Revenue; Clinical Analysis’ Revenue increased 23,0%, driven by organic growth and Weinmann’s acquisition. 9

Preventive Medicine 45.9% increase excluding Fleury Hospital-Dia operations . The Chronic Disease Management service has reached 27.0 thousand lives under contract. The Executive Health Assessment revenue increased by 28.1%, with a 31.6% growth in the number of assessments. Quarterly gross revenue – Preventive Medicine (R$ millions) 10 10 10 10

Costs of Services % Net Revenue 3Q09 R$ Million % Net New Previous 3Q10 Revenue criterion criterion Personnel and medical services 65.5 28.2% 28.0% 28.4% General services, Rent and Utilities 25.9 11.2% 11.1% 13.8% Materials and Outsourcing 25.9 11.2% 11.1% 11.7% General Expenses 12.7 5.5% 5.4% 3.1% 110.0 TOTAL 130.1 56.0% 55.5% 56.9% 11 11

Gross Margin (% of Net Revenue) 12 12

Operational Expenses General and Administrative Expenses (excluding the provisions for Profit Sharing Plan and Depreciations) amounted to R$43.6 million , 18.8% of the Net Revenue – which includes R$ 5,2 million in marketing expenses for the midia campaign. Depreciations amounted R$ 8.0 million, PSP R$ 2.5 million. Other Operational Revenues (Expenses), net amounted R$0.9 million: R$ 8.8 million (revenue): tax credit; R$ 5.4 million (expense): bad debt provisions; R$ 2.2 million (expense): provision adjustments for ICMS – state tax for imported machines; R$ 0.2 million (expense): other expenses; 13 13

Income Tax and Social Contribution 1- Other: Non Recurring Provisions, Non-Deductible Expenses, Equity in Subsidiaries 14 14

Net Income 29.4% growth , adding up to R$ 44.6 million. The profit margin represented 19.2% of net revenue . R$ 100 million in 9M10 , 56.9% growth. Net Income and Profit Margin (R$ million) 10.9% 15.3% 19.2% 4.6% 6.2% 11.2% 17.8% 6.6% 15 15

EBITDA R$ % net million revenue Net Income 44.6 19.2% EBITDA margin of 25.9%, 136 basis points higher than 2Q10 and 192 basis points below Financial Expenses (Income) (8.0) (3.4%) than 3Q09. Depreciation and amortization 8.0 3.5% Income Tax and Social Contribution 15.3 6.6% 11.7% increase, achieving R$ 60.0 million. EBITDA 60.0 25.9% EBITDA and EBITDA margin on net revenue (R$ million) 19.5% 17.9% 22.9% 23.3% 24.2% 25.9% 24.4% 27.8% 16

EBITDA Analysis Item % of Net Revenue 25.9% EBITDA Reported R$ 60.0 MM Acquisitions +20 bps Cost of Services – +75 bps Non recurring and pre-operational R$ 1.7 MM Administrative Expenses – +225 bps Fleury brand marketing expenses R$ 5.2 MM Other Operating – -380 bps Prefis tax credit R$ 8.8 MM Other Operating – + 95 bps Provision adjustments for ICMS R$ 2.2 MM -215 bps Reserve for contingencies R$ 5.0 MM ADD-BACK TOTAL -180 bps 17

Investments CAPEX amounted R$ 13.7 million in 3Q10 CAPEX Breakdown - 9M10 Movements related to investments in PSCs achieved 1.6 thousand square meters CAPEX demand 2010-2011 adjusted to R$ 40.8 million R$ 269 million: 9M10 = R$ 40.8 million 4Q10 + 1H11= R$ 135 million 2H11 = R$ 93 million 18 18

Cash Flow, Accounts Receivable and Debt Accounts Receivable R$ MM Cash Flow R$ MM June 30th 200.1 Net Income 44.6 Quarter´s Revenue 248.5 Collection from Customers (217.9) Op. Cash Flow 39.6 September 30th 230.7 Net Cash Flow 4.7 Bad Debt Provision (31.8) Accounts Receivable (net) 198.9 Debt Position Total (R$ MM) Next 12m Loans 99.7 35.8 Acquisitions 41.0 7.7 Taxes 79.1 11.1 TOTAL DEBT 219.9 54.6 Cash and Equivalents 572.9 19

Capital Market FLRY3 Shares and Market Cap - 09/30/2010 Stock performance Shares Outstanding 131,298,550 Close (09/30/2010) R$ 21.00 3Q10 +5.1% Free Float 41,792,510 (31.8%) 3Q10 High R$ 23.17 9M10 +14.2% Market Cap R$ 2.76 billion 3Q10 Low R$ 19.82 IPO +31.3% +31.3% +1.2% 20 20

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.