To Whither or Wither ? To Whither or Wither ? Observations on the - PDF document

Dr Roderick Deane - 1 May 2007 To Whither or Wither? To Whither or Wither ? To Whither or Wither ? Observations on the State of the Economy Roderick Deane* An address to the Treasury Group Lecture Series, Wellington 1 May 2007 *Dr Roderick

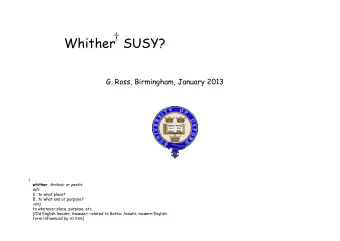

Dr Roderick Deane - 1 May 2007 To Whither or Wither? To Whither or Wither ? To Whither or Wither ? Observations on the State of the Economy Roderick Deane* An address to the Treasury Group Lecture Series, Wellington 1 May 2007 *Dr Roderick Deane is Chairman of Fletcher Building Ltd and the NZ Seed Fund, and a Director of Woolworths Ltd in Sydney. He is also Patron and Chairman of the IHC Foundation. Until 30 June 2006 he was Chairman of ANZ National Bank, Telecom Corporation of NZ Ltd, Te Papa Tongarewa (The Museum of NZ), City Gallery Wellington Foundation, and a Director of the ANZ Banking Group Ltd in Melbourne. Dr Deane is very appreciative of the assistance he was given in preparing this material by the Economics Group of the ANZ National Bank and by Bryce Wilkinson and Roger Kerr. A long-run perspective on New Zealand’s economic growth GDP per Capita ( 1 8 6 6 -2 0 0 6 ) Real Com m odity Prices ( 1 9 0 0 -2 0 0 6 ) $, 1995/96 prices, March yrs Index 200 $35,000 $30,000 150 $25,000 $20,000 100 $15,000 $10,000 50 $5,000 $0 0 1866 1886 1906 1926 1946 1966 1986 2006 1900 1920 1940 1960 1980 2000 The rise and fall of NZ’s relative NZ’s Current Account History place in the w orld: ( 1 8 2 0 -2 0 0 5 ) ( 1 9 5 5 -2 0 0 6 ) OECD rank in terms of GDP per capita % of GDP, March yrs 1 5 6 0 11 -5 16 -10 21 -15 1820 1870 1913 1950 1973 1990 1998 2005 1955 1965 1975 1985 1995 2005 2 Sources: Statistics NZ; IMF; ANZ National Bank; OECD (Luxembourg and Iceland are excluded due to lack of data).

Dr Roderick Deane - 1 May 2007 To Whither or Wither? Current macroeconomic settings have improved significantly GDP Grow th per Capita ( 1 9 6 6 -2 0 0 6 ) Consum er Price I nflation ( 1 9 6 6 -2 0 0 7 ) Annual % change Ann % chg (March yrs) 20 6 15 4 2 10 0 5 -2 0 -4 -5 -6 1966 1971 1976 1981 1986 1991 1996 2001 2006 1966 1971 1976 1981 1986 1991 1996 2001 2006 Fiscal Balance ( 1 9 7 2 -2 0 0 6 ) Unem ploym ent Rate ( 1 9 6 6 -2 0 0 6 ) % of GDP, June yrs % 8 12 6 10 4 8 2 0 6 -2 4 -4 2 -6 -8 0 1971 1976 1981 1986 1991 1996 2001 2006 1966 1971 1976 1981 1986 1991 1996 2001 2006 3 Sources: Statistics NZ; Treasury; ANZ National Bank. Terms of trade, productivity Productivity – Labour Term s of Trade ( 1 9 6 6 -2 0 0 6 ) ( 1 9 9 1 -2 0 0 6 March yrs) Index % (growth, 3 yr average) 1500 6 1300 4 1100 2 900 0 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 -2 700 1966 1971 1976 1981 1986 1991 1996 2001 2006 -4 Productivity – Capital Productivity – Multifactor ( 1 9 9 1 -2 0 0 6 March yrs) ( 1 9 9 1 -2 0 0 6 March yrs) % (growth, 3 yr average) % (growth, 3 yr average) 6 6 4 4 2 2 0 0 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 -2 -2 -4 -4 4 Sources: Statistics NZ; ANZ National Bank.

Dr Roderick Deane - 1 May 2007 To Whither or Wither? Multifactor Productivity Trend Average Annual Growth Rate Clark-Cullen 2000-2006 0.7 Years ended March After the Employment Contracts Act and 1991 Budget 1992-2000 2.3 During "The 'Failed' Policies of the Past" 1988-2000 2.0 0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0 2.2 2.4 2.6 Percent 5 Sources: Statistics NZ; Capital Economics Consequently, NZ has transformed itself from a below average performer to an above average performer Distribution of per capita grow th rates for advanced countries, 1 8 7 0 -1 9 9 8 NZ 1970-1976 NZ 1998-2006 1.9% 2.1% NZ 1987-1996 Density estimate 0.7% NZ 1977-1986 0.8% 0 0.9 1.1 1.2 1.3 1.5 1.6 1.7 1.8 1.9 2.0 2.2 2.3 2.4 2.5 GDP growth per capita (%) 6 Sources: Angus Maddison, The World Economy: a millennial perspective , OECD, 2001. Statistics NZ.

Dr Roderick Deane - 1 May 2007 To Whither or Wither? We benefited from the mid-80’s to mid-90’s reforms A rem inder on the Reform s • Monetary and fiscal policy vastly improved • Dollar floated • Low inflation achieved • Labour market transformed • Internal regulatory structures dismantled • Income taxes reduced • Size of government scaled back • Government offshore debt eliminated • Budget moved to surplus • Corporatisation/ privatisation delivered • Exchange controls/ import licensing abolished • Tariffs greatly reduced • Price, wage and dividend controls abolished Outcom e: Business sector adaptability hugely increased 7 The decline has been arrested GDP per capita GDP per capita (US$) 30,000 OECD 1970-2005: 25,000 OECD average growth = 2.0% per annum NZ average growth = 1.3% per annum 20,000 NZ 15,000 10,000 5,000 0 1970 1975 1980 1985 1990 1995 2000 2005 8 Sources: OECD; ANZ National Bank.

Dr Roderick Deane - 1 May 2007 To Whither or Wither? But closing the gap requires something a lot more I t took us 2 0 years to fall dow n the ladder. Assum ing OECD real GDP per capita grow th of 2 .0 percent, NZ needs to grow at 2 .7 percent to close the gap by 2 0 2 5 GDP per capita (US$) 40,000 OECD 35,000 For NZ to catch up by 2025 requires: OECD average growth = 2.0% per annum 30,000 NZ NZ average growth = 2.7% per annum 25,000 20,000 15,000 10,000 For NZ to catch up by 2015 requires NZ average growth of 3.4% per annum 5,000 0 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 9 Sources: OECD; ANZ National Bank. We are here, but we need to be there… Distribution of real per capita grow th rates for advanced countries, 1 8 7 0 -1 9 9 8 NZ 1998-2006 2.1% Density estimate 0 0.9 1.1 1.2 1.3 1.5 1.6 1.7 1.8 1.9 2.0 2.2 2.3 2.4 2.5 GDP growth per capita (%) 10 Sources: Angus Maddison, The World Economy: a millennial perspective , OECD, 2001. Statistics NZ.

Dr Roderick Deane - 1 May 2007 To Whither or Wither? Work harder or work smarter GDP / hours worked ($) 90 Luxembourg 80 Norway Belgium 70 France Ireland United States Productivity Netherlands 60 Denmark UK Germany Austria Sweden Canada Switzerland 50 Finland Spain Italy Australia Iceland GDP per Japan 40 capita Greece level New Zealand 30 Portugal Turkey 20 10 10 11 12 13 14 15 16 17 18 19 20 Hours worked per capita per week Population and Participation 11 Source: OECD OECD We continue to rank lowly in the OECD stakes OECD Nation Rankings Richest nation: Luxem bourg High incom e: Norw ay, USA, I reland, Sw itzerland Middle/ high incom e: 1 4 nations including Australia, UK, Canada, France, Japan Low / m iddle incom e: New Zealand, Spain, Greece, Korea, Portugal Low est incom e: Turkey Rankings based on purchasing power, taking into account the cost of 3000 items, from a litre of milk to building a house 12

Dr Roderick Deane - 1 May 2007 To Whither or Wither? Are we in fact starting to go backwards? Econom ic Freedom I ndex ( 1 9 7 0 -2 0 0 4 ) W ork Stoppages ( 1 9 9 1 -2 0 0 6 ) Index Person days of work lost 9 New Zealand 120000 8 100000 7 80000 6 60000 40000 5 20000 4 0 1970 1975 1980 1985 1990 1995 2000 2004 1991 1993 1995 1997 1999 2001 2003 2005 Labour Productivity Multifactor Productivity Compound annual average growth rate Compound annual average growth rate 5 3 4 2 3 2 1 1 0 0 '88-'90 '90-'95 '95-'00 '00-'06 '88-'90 '90-'95 '95-'00 '00-'06 13 Sources: Statistics NZ; ANZ National Bank; Economic Freedom Annual Report 2006 (The Fraser Institute). Core public service employment growth All other sectors 2.8 2000-2006 Government Administration and Defence 4.1 Calendar years 1.9 1995-2000 -2.5 2.7 1990-1995 -2.6 -3 -2 -1 0 1 2 3 4 5 Percent 14 Source: Statistics NZ; ANZ National Bank.

Dr Roderick Deane - 1 May 2007 To Whither or Wither? Working less but wanting more Hours w orked per full tim e em ployee Core crow n spending ( 1 9 8 6 -2 0 0 6 ) ( 1 9 9 7 -2 0 1 1 June yrs) Hours (s.a.) % of GDP 40.5 Forecasts 34 40.0 33 39.5 32 39.0 31 38.5 30 38.0 29 37.5 28 1986 1991 1996 2001 2006 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 Unem ployed and beneficiary num bers Current Account Deficit ( 1 9 8 0 -2 0 0 6 ) ( 1 9 8 0 -2 0 0 6 June yrs) 1980 1984 1988 1992 1996 2000 2004 (000) 0 200 Unemployed -2 150 -4 100 -6 50 Sickness and invalid -8 Beneficiaries 0 % of GDP -10 1980 1984 1988 1992 1996 2000 2004 15 Sources: Statistics NZ; Treasury; Ministry of Social Development, ANZ National Bank. Household borrowing sky-rocketing Household debt I nterest servicing % of disposable income % of disposable income 15 170 150 130 10 110 90 70 50 5 1991 1994 1997 2000 2003 2006 1991 1994 1997 2000 2003 2006 Housing affordability Bank & NBFI lending to households NZ$ billion NZ$ billion 60 % Index (92Q1=100) 160 160 18 Proport ion of weekly wage required 140 50 16 t o service mort gage(LHS) 140 Tot al lending t o 120 14 households (LHS) 120 40 100 12 100 10 30 80 80 8 60 60 20 6 Banks (LHS) NBFI s (RHS) House price- t o- income adjust ed for 40 40 4 10 int erest rat es (RHS) 20 20 2 1998 2000 2002 2004 2006 0 0 16 1992 1994 1996 1998 2000 2002 2004 2006 Sources: Reserve Bank of NZ; ANZ National Bank.

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.