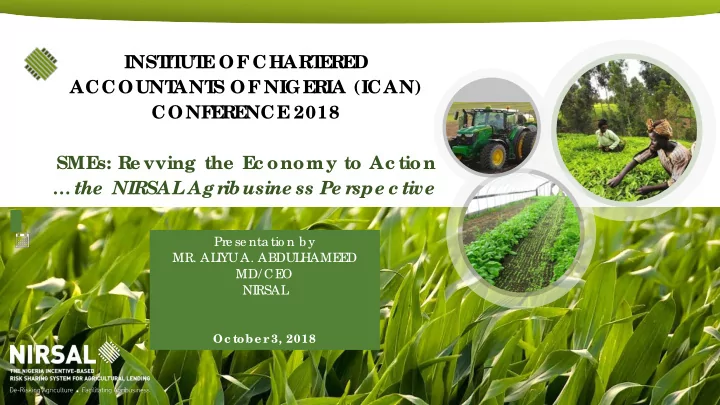

INST IT UT E OF CHART E RE D ACCOUNT ANT S OF NIGE RIA (ICAN) CONF E RE NCE 2018 SME s: Re vving the E c onomy to Ac tion …the NIRSAL Agr ibusine ss Pe r spe c tive Pre se nta tio n b y MR. AL I YU A. ABDUL HAME E D MD/ CE O NI RSAL Oc tobe r 3, 2018

Conte nts I ntro duc tio n 1 Ag rib usine sse s a nd the Nig e ria n 2 E c o no my NI RSAL ’ s Ac tivitie s in F a c ilita ting 3 Ag rib usine ss Co nc lusio n 4 1

Se c tio n 1 INT RODUCT ION 2

T he Nige r ian E c onomic gr owth tr e nds in Nige r ia E c onomy 33.7% 2004 25% 1970 US$2,564 2016 US$2,412 0.83% 2017 2017 - 1.6% 2016 NIGE RIA, GDP GROWT H (% ) (CONST ANT 2010 US$) NIGE RIA, GDP PE R CAPIT A (CONST ANT 2010 US$) 1961 - 2017 2007- 2017 Nig e ria e xpe rie nc e d the hig he st spike s in re a l GDP g ro wth in 1970 (25% ) a nd 2004 (33.7%). • T he na tio n ma na g e d to re c o rd a me a g re 0.8% GDP g ro wth in 2017 re c o ve ring fro m the de pre ssio n in • 2016 with -1.6% g ro wth. Re a l GDP pe r c a pita in Nig e ria g re w b y a Co mpo und Annua l Gro wth Ra te (CAGR) of 3% in the first 7 • ye a rs o f the la st de c a de 2007-2017 a nd de c line d by 2% in the la st 3 ye a rs le a ving GDP pe r Ca pita a t US$2,412 c ompa re d to world a ve ra g e of US$10,634 . So urc e : Wo rld Bank Ope n Data, NI RSAL Analysis 3

Pr ofile of 91 Ac c o rding to Se pte mb e r 2018 Mc K inse y Re po rt, Nig e ria is Countr ie s ra nke d a “Volatile Gr ” with “ No r e lative c hange : No or owe r asse sse d by MGI ove me nt in spite o f the na tio n’ s po te ntia ls inc onsiste nt impr T he se 18 Outpe r for me r c ountr ie s have c umulative ly lifte d 1billion pe ople out of pove r ty be twe e n 1990 and 2013 14 Unde r pe r for me r s 13 ‘Middle r ’ Vola tile 17 ‘Middle r ’ Gr owe r s 20 Hig h Consiste nt Inc ome 7 L ong -te r m 9 ‘Middle r ’ Gr owe r s Countr ie s Out Ve r y r e c e nt 11 Re c e nt pe r for me r s Ac c e le r a tor s Inc luding Out T anzania, Uganda, pe r for me r s Inc luding Mor oc c o Ghana and Rwanda E c o no mie s with Outpac e d US GNI pe r c apita o f g ro wth $6,000 o r mo re in F alle n b e hind: c o nsiste ntly fro m Outpac e d US g ro wth 1987, e xc e pt No re lative c hang e : Slo we r re lative 1965-2016 with c o nsiste ntly fro m Ho ng Ko ng and No o r inc o nsiste nt impro ve me nt re lative to US fro m 1965– 1996-2016 with GDP GDP pe r c apita g ro wth than US Sing apo re whic h 2016 pe r c apita g ro wth g ro wth ab o ve fro m 1965–2016 are Outpe rfo rme rs ab o ve 3.5% annually fo r 5% annually fo r 20 50 ye ars ye ars So urc e : Mc Kinse y Glo b al I nstitute (MGI ), Se pte mb e r 2018, NI RSAL Analysis 4

Pr ofile of 91 Countr ie s asse sse d by MGI So urc e : Mc Kinse y Glo b al I nstitute (MGI ), Se pte mb e r 2018, NI RSAL Analysis 5

L e ssons fr om high Rapid gr owth of Outpe r for ming e c onomie s we r e attr ibute d to gr owth c e r tain ke y fac tor s in the MGI r e por t e c onomie s Go ve rnme nt Po lic ie s Ac kno wle dg e me nt a nd e na b le d a pro- g rowth de lib e ra te Suppo rt to Sma ll Cyc le b a se d o n a nd Me dium E nte rprise s Nume ro us hig hly Pro duc tivity, I nc o me a nd s) : (SME a rg e F irms: Compe titive L De ma nd b y: s ha ve b e e n a po lic y SME • e xpa nsio n o f a vib ra nt • suppo rting c a pita l a nd fo c us o f ma ny • priva te se c to r te c hno lo g y o utpe rfo rme r e c o no mie s c ha ra c te rize d b y hig hly a c c umula tio n Suppo rt is pro vide d c o mpe titive firms • e na b ling c o nne c tio n to tho ug h c re dit g ua ra nte e e me rg ing a s g lo b a l • fo re ig n ma rke ts pro g ra ms, inno va tive pla ye rs. sub sidie s, a ssista nc e with c re a ting e nviro nme nts fo r Co mpe titio n drive n • • inte rna tio na l c e rtific a tio n, inve stme nts, c o mpe titio n inno va tio n a nd dig ita l te c hno lo g ie s, e - a nd ma rke t e ffic ie nc y. inve stme nts in R&D c o mme rc e a nd Huma n c a pita l c o nne c tivity pla tfo rms • de ve lo pme nt a nd hig he r inc o me s So urc e : Mc Kinse y Glo b al I nstitute (MGI ), Se pte mb e r 2018, NI RSAL Analysis 6

F oc us on MSME s ar e a c r itic al c ompone nt of the Nige r ian e c onomy and MSME s in de libe r ate atte mpts must be made to suppor t the ir gr owth Nige r ia In spite of the ir importa nt c ontributions a nd pote ntia ls for 37,000,000 g rowth, SME s fa c e a numbe r of c onstra ints a nd c ha lle ng e s MSME s in Nig e ria a c c o unt fo r: I na de q ua te a c c e ss to fina nc e 50% Po o r infra struc ture o f its GDP L imite d a c c e ss to ma rke ts 84% L imite d use o f mo de rn te c hno lo g y o f E mplo yme nt Hig h le ve ls o f unskille d wo rkfo rc e 7.27% Multiple ta xa tio n o f E xpo rt E a rning s Diffic ult re g ula to ry e nviro nme nt So urc e : E RGP 2017-2020, SME DAN/NBS Surve y 2013 7

Se c tio n 2 Agr ibusine sse s and the Nige r ian E c onomy 8

Nige r ian Agr ibusine ss MSME s, par tic ular ly, r e main one of Nige r ia’s Agr ic ultur al gr e ate st hope s for e c onomic gr owth and de ve lopme nt Pote ntials In 2017 full ye ar By 2020 NGN17.2 T r illio n g re w @ a ra te o f (Re al/ Co nstant Pric e s) T he Agr ic ultur e 3.45% in re a l (c o ntr ibute d 25% to se c tor : RE AL GDP) te rms T he Ag ric ulture se c to r ha s the NGN23.9 T r illio n po te ntia l to g ro w to a ra te o f (No minal/ Curre nt b asic Pric e s) while 8.37% in re a l te rms NGN21 T r illio n (Re al/ Co nstant Pric e s) g re w @ a ra te o f NGN69.2 T r illio n T he e c onomy as (Re al/ Co nstant Pric e s) 0.83% in re a l a whole : NGN114.9 T r illio n te rms (No minal/ Curre nt b asic Pric e s) * So urc e : NBS 2017 Re po rts & E 9 RGP

E c osyste m of Ag rib usine ss MSME s spa n a c ro ss se g me nts o f va rio us a g ric ultura l Ag ribusine sse s va lue c ha ins, a c c o unting fo r 97% of the Agr ic ultur al GDP of Nige r ia as at 2013* Se gme nts AVC Pr e - Upstr e am Upstr e am Midstr e am Downstr e am So me o f the se ibusine sse s Ag ro -pro c e sso rs • Ag rib usine ss Prima ry • • F e rtilize r Ag ro -d e a le rs (e xtra c tio n, milling , e s c a n Pro duc e rs • Se e d , CPP a nd o the r Re ta ile rs drying , c le a ning , e tc .) • g e ne ra te up o f Ce re a ls, Input Distrib uto rs E xpo rt Se rvic e Pro vide rs fo r: • • T ub e rs, to 200% • T ra c to r a nd Ha ula g e b ro ke rs o Aq ua c ultu E q uipme nt Hiring Re tur ns o n ype s o f Agr E xpo rt Ag g re g a tio n • o Ag e nts, Bo o king re , F F V, Inve stme nt Me rc ha nts Sto ra g e o Ag e nts, Ope ra to rs, Po ultry, a nd T ra nspo rta tio n o Me c ha nic s, e tc . Rumina nts, L o g istic s Pa c ka g ing • Re se a rc h F a rme rs o Apic ulture , Middle me n/ • E xte nsio n Ag e nts • e tc . T I nte rme dia rie s 10 *2013 NBS a nd SME DAN Re po rt

Nige r ian Nige r ia is ble sse d with four (4) major oppor tunitie s for Agr ic ultur al agr ibusine sse s to thr ive Pote ntials L AND L ABOUR MARKE T WAT E R Hug e c o nsume r ma rke t o f 84 millio n he c ta re s o f Hug e supply o f la b o ur– Pre dic ta b le ra infa ll pa tte rn; a ra b le la nd with o nly o ve r 90 millio n po pula tio n 200millio n pe o ple with Billio ns c u. m o f surfa c e a nd a b o ut 50% in use a g e d 15-65 ye a rs unsa tisfie d de ma nd unde rg ro und wa te r … whic h if prope rly ma na g e d, would de live r: E mplo yme nt F o o d F o re ig n E c o no mic Ge ne ra tio n Ba la nc e o f Se c urity & Gro wth & E xc ha ng e T ra de & L ive liho o ds Nutritio n E a rning s Dive rsific a tio n Susta ina b ility 11 So urc e : AfDB, 2015, F rie nds o f E uro pe , 2014

Capitals r e quir e d to … but lac ks four (4) c r itic al c apitals maximize the pote ntials of Agr ibusine sse s F INANCE HUMAN T E CHNOL OGY E QUIPME NT Capital Capital Capital Capital Pa tie nt c a pita l I nte lle c tua l a nd Sc ie ntific a nd Hig h-e nd e q uipme nt to po we r a n te c hnic a l c a pa c ity te c hno lo g ic a l fo r me c ha nisa tio n a g ric ultura l fo r a g rib usine ss so lutio ns fo r a nd re vo lutio n inc re a se d c o mme rc ia lisa tio n pro duc tivity 12

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries