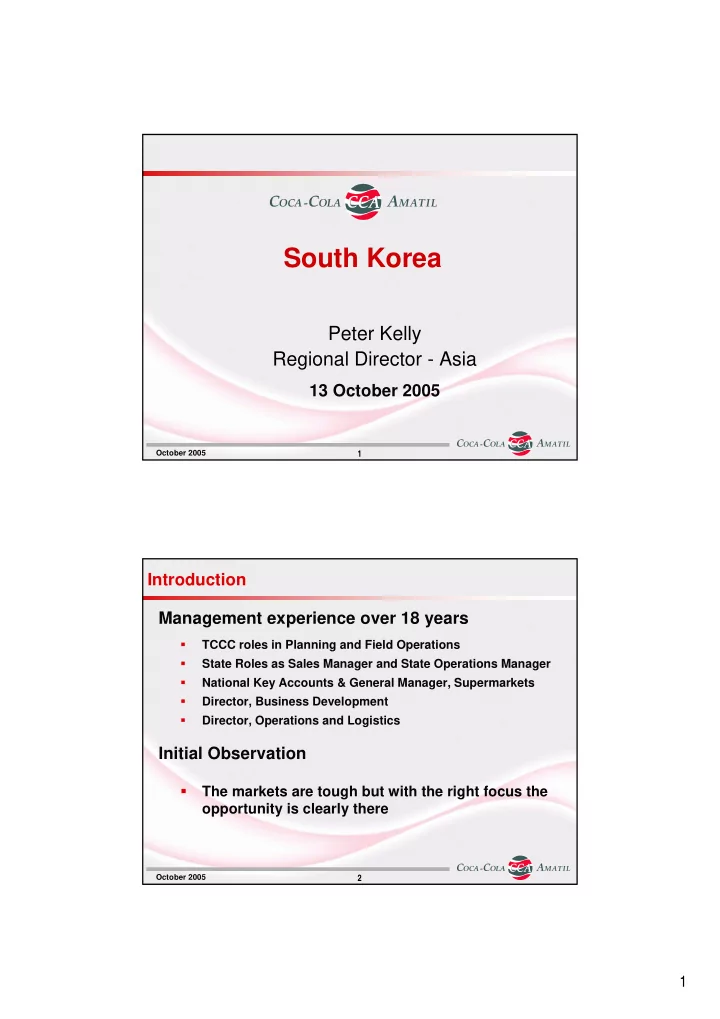

South Korea Peter Kelly Regional Director - Asia 13 October 2005 October 2005 1 Introduction Management experience over 18 years � TCCC roles in Planning and Field Operations � State Roles as Sales Manager and State Operations Manager � National Key Accounts & General Manager, Supermarkets � Director, Business Development � Director, Operations and Logistics Initial Observation � The markets are tough but with the right focus the opportunity is clearly there October 2005 2 1

Korea � New Executive Team, focused on the simple drivers of growth that will turn the business around � The key issues are being addressed � Results in Qtr 3 are very encouraging – best Qtr for growth since the start of 2004 � CCA and TCCC are confident that investments being made in Korea will deliver improved performance October 2005 3 Our expectations for Korea in the 2 nd half… � 2005 2 nd Half Volume Growth 5-7% � 2005 2 nd Half EBIT KRW broadly in line with last year � Examples of trade execution for full year 2005 � Net New Outlets 16,000+ � Net Coolers placed 21,000+ � Minute Maid 15% of 100% Juice segment October 2005 4 2

Consumer Spending and CCA sales are highly Correlated – both are returning to growth 35% 150 144 140 27% 138 Sales Volume Million Unit Cases 19% 126 Percentage 123 122 122 11% 114 8% Consumer 5% Spending 2% 3% 102 -1% -1% -5% 90 2001 2002 2003 2004 2005 June Source : The Bank of Korea October 2005 5 Consumer confidence appears to be recovering Korean Consumer Confidence Index 120 110 Index 100 90 80 Jul 99 Jan 00 Jul Jan 01 Jul Jan 02 Jul Jan 03 Jul Jan 04 Jul Jan 05 Jul Source : Korea National Statistical Office October 2005 6 3

GDP per capita growth, at 18% is growing faster than both consumer confidence and spending 18000 (Unit: %) 16,740 GDP per capita +18.2% 15000 14,162 12,720 +11.3% (Unit: Million US$) 11,499 12000 +10.6% 10,841 10,160 +13.2% 9,438 +14.9% -6.3% 9000 +28.3% 7,355 6000 3000 1998 1999 2000 2001 2002 2003 2004 2005 (E) Source : The Bank of Korea, 2005(E) from Economic Intelligence Unit October 2005 7 Competitors show 10% EBIT margins are achievable � Biggest competitor, Lotte H105 results � Revenue declined by -9% � EBIT Margin at 10% down from 16% � EBIT Margin decline driven by un-recovered COGS � Operating income down by 45% � Implication for CCA Korea – we believe an opportunity exists to improve pricing and recover COGS increases, however we will not be uncompetitive October 2005 8 4

It’s a competitive market – CCA is holding share CCA NARTD Share 30.0% 25.2% 25.0% 24.9% 24.4% 25.0% 20.0% 15.0% 10.0% 5.0% 0.0% June / July YTD JJ 2004 2005 (Source: AC Ni e: AC Niels elsen) n) October 2005 9 Recap - CCA Performance in the 1 st Half HY 05 HY 04 % Chg Volume (m unit cases) 63 64 -1% Sales revenue / case KRW 3,859 3,902 -1% EBIT KRW (m) 346 10,581 -97% � Brand Coke related volume/pricing accounts for 2/3rds of our EBIT decline. (Coke 1 st Half -10% vs Qtr 3 +4%) � We will be managing both our costs and pricing tightly in an effort to recover COGS inflation � There is a lag in getting the benefits from our increased investments in Direct Marketing Expense and Coolers October 2005 10 5

Significant increase in TCCC marketing investment � 2005 TCCC direct marketing investment is double 2004 levels � CCA expects at least this level of brand investment to continue for 2006 � Both companies are aligned around fewer, bigger activities on the core brands 2006 October 2005 11 Excellent Main Media on air since April Eg Supporting our E&D Focus October 2005 12 6

Minute Maid - We are now in all the major categories Korea Key Categories 15% Percentage of NARTD Market 12% 9% 6% 3% 0% Cola Flavoured CSD Cider Fruit Juice Fruit Juice - Sports 100% Non 100% CCA Category (Source: AC Ni e: AC Niels elsen) n) October 2005 13 Update on the activation of the 5 Pillars Our trade execution results are on track for 2005 across the 5 pillars 1. Product and pack innovation 2. Non-carbonated beverage and food expansion 3. Growing product availability through cold drink placements and outlet expansion 4. Customer service improvement 5. Revenue management and cost discipline October 2005 14 7

New Brands and Packs delivering growth � Our brands are returning to growth and profit for our retailers � Non-Carbonate Innovation � 3 New Non-Carb Brands � Minute Maid � Minute Maid Fresh Mix � Powerade Ionade � 10 New Non-Carb Brand / Flavour Extensions � Nestea Lemon Green and Ice Rush � Minute Maid Tomato and Grape � Nescafe Mistra (6 flavours) October 2005 15 Non Carbonates - Minute Maid doing well � 15% Share of 100% Juice after 4 months 30 � Record Repeat Purchase levels 25 24 20 19 15.2 15 9.4 10 3 5 1.1 0 FM05 AM05 JJ05 Sales Share in 100% Fruit Juice Availability (Source: AC Ni e: AC Niels elsen) n) October 2005 16 8

Minute Maid – Getting the Key Components Right � Innovative product range and packs � Huge sampling campaign 500,000+ Consumers � Excellent advertising and Media weights � Excellent execution and trade support October 2005 17 With Food – Eating & Drinking sales up 28% YTD � Menu boards, branding, staff incentives and Combo meals � Building the connection between Korean Food and CSD’s October 2005 18 9

Cold drink – By December 21,000 new coolers � Coolers drive consumption � More is required to capture the opportunity Cooler Penetration per 10k Population 100,000 18 15.8 16 14.5 80,000 76,499 13.5 14 13.0 70,106 11.9 65,014 12 11.2 62,712 10.5 10.4 60,000 57,219 9.9 9.8 53,943 10 50,375 49,698 46,712 46,476 8 40,000 Total Cooler in Market (# of unit) 6 4 20,000 2 0 0 Dec 01 Dec 02 Dec 03 Mar 04 Jun Sep Dec 04 Mar 05 Jun Sep October 2005 19 By Year end 16,000 more customers than 2004 Total Active Outlet Outlets 12,000 Numbers Total 120,000 90,000 8,000 E&D 60,000 Wholesale 4,000 30,000 M&P Super CVS Hyper 0 0 Jan 02 Jul Jan 03 Jul Jan 04 Jul Jan 05 Jul October 2005 20 10

Product availability - Forward inventory drives sales � We have gained forward inventory share of NARTD and are targeting 10% more cases on the shop floor 30% CCA Forward Inventory Share 22.6% 22.3% 20% 10% Jan 02 Jul Jan 03 Jul Jan 04 Jul Jan 05 Jul (Source: AC Ni e: AC Niels elsen) n) October 2005 21 Forward Inventory- attractive merchandising October 2005 22 11

Quality availability - 135 Model Markets +35% up � We now have 135 model markets up and running in Korea � They prove again that superior execution can drive incremental beverage sales for all customers in a region � The model markets are a test bed for our trade marketing concepts and training ground for our sales employees October 2005 23 Customer Service Improvements We are focused on driving customer volume and profit and giving the customer a greater voice in our business � Customer and category business management � Customer Satisfaction Call program � Servicing the needs of smaller outlet October 2005 24 12

Efficiency and Cost Reduction – an opportunity � When benchmarked against comparable CCA operations, Korea has a KRW 20b higher indirect cost base � Through a combination of workplace reform, redeployment and downsizing we can begin to close this gap � Despite the historically difficult industrial relations environment in Korea, there is a general consensus among our employees for the need for change � Our preference is to retrain and redeploy people into market facing roles rather than dramatically downsize the organisation � The success of our suggested workplace reforms will determine the eventual number of employees our business can sustain, any restructuring costs and the associated savings October 2005 25 Korean Nationals now make up 2/3 rds of the Executive Team October 2005 26 13

Our expectations for Korea in the 2 nd half… � 2005 2 nd Half Volume Growth 5-7% � 2005 2 nd Half EBIT KRW broadly in line with last year October 2005 27 Our plans for 2006 � Major Investments in Marketing, Trade and Product innovation behind Coke and Minute Maid � 1 Major Non-Carbonate New Product Launch � Cooler penetration increasing to 20 per 10K population � CCA executing in 18% of all outlets � Workplace reforms targeting indirect savings � Redeployment of up to 200 people to market facing roles October 2005 28 14

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries