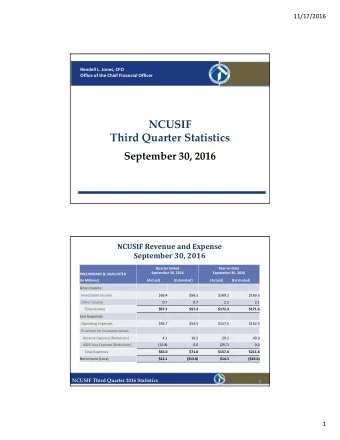

September 2016 Disclaimer This presentation is confidential and is - PowerPoint PPT Presentation

Management Presentation (TSXV:ED.UN) September 2016 Disclaimer This presentation is confidential and is being supplied to you solely for your information and may not be reproduced or distributed to any other person or published, in whole or in

Management Presentation (TSXV:ED.UN) September 2016

Disclaimer This presentation is confidential and is being supplied to you solely for your information and may not be reproduced or distributed to any other person or published, in whole or in part, for any purpose. No reliance may be placed for any purpose whatsoever on the information contained in this presentation or the completeness or accuracy of such information. No representation or warranty, express or implied, is given by or on behalf of Edgefront REIT (the “REIT”), or its unitholders, trustees, officers or employees or any other person as to the accuracy or completeness of the information or opinions contained in this presentation, and no liability is accepted for any such information or opinions. This presentation contains forward-looking statements which reflect the REIT’s current expectations and projections about future results. Often, but not always, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not expect”, “is expected”, “estimates”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the REIT to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Actual results and developments are likely to differ, and may differ materially, from those expressed or implied by the forward-looking statements contained in this presentation. Such forward-looking statements are based on a number of assumptions that may prove to be incorrect, including, but not limited to: the ability of the REIT to obtain necessary financing or to be able to implement its business strategies; satisfy the requirements of the TSX Venture Exchange with respect to the plan of arrangement; obtain unitholder approval with respect to the plan of arrangement; the level of activity in the retail, office and industrial commercial real estate markets in Canada, the real estate industry generally (including property ownership and tenant risks, liquidity of real estate investments, competition, government regulation, environmental matters, and fixed costs, recent market volatility and increased expenses) and the economy generally. While the REIT anticipates that subsequent events and developments may cause its views to change, the REIT specifically disclaims any obligation to update these forward-looking statements. These forward-looking statements should not be relied upon as representing the REIT’s views as of any date subsequent to the date of this presentation. Although the REIT has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward- looking statements. The factors identified above are not intended to represent a complete list of the factors that could affect the REIT. This presentation includes industry data and forecasts obtained from independent industry publications, market research and analyst reports, surveys and other publicly available sources and in certain cases, information is based on the REIT’s own analysis and information or its analysis of third-party information. Although the REIT believes these sources to be generally reliable, market and industry data is subject to interpretation and cannot be verified with complete certainty due to limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in any statistical survey. Accordingly, the accuracy and completeness of this data is not guaranteed. The REIT has not independently verified any of the data from third party sources referred to in this presentation nor ascertained the underlying assumptions relied upon by such sources. 1

Overview of the REIT • Edgefront REIT (TSXV:ED.UN) (“Edgefront” or the “REIT”) is a unique industrial-focused REIT that owns 20 properties and has a current market capitalization of ~$77 million • Focused on acquiring single tenant industrial properties leased to high quality tenants with long-term leases and embedded rent escalations (approximately $175K in 2016 escalations) (1) • Strong sponsorship from TriWest Capital Partners (“TriWest Capital”) • Founded in 1998, TriWest Capital is one of Canada’s leading private equity firms having raised over $1.25 billion of committed capital with a track record of strong equity returns • Provides the REIT with a pipeline of attractive investment opportunities to acquire on a non-marketed basis through TriWest Capital’s portfolio companies 1) Represents an approximate 1.5% increase over 2015 property revenue of $12.0M 2

Investment Highlights • Unique Growth-Oriented REIT with an Established Pipeline of Acquisition Opportunities – Industrial- focused REIT supported by TriWest Capital, one of Canada’s leading private equity firms • Experienced Management Team with a Proven Track Record of Success – Edgefront’s CEO, Kelly Hanczyk, is the former CEO of TransGlobe Apartment REIT • Strong Sponsorship from TriWest Capital – Indirectly own over 50 properties through current ownership of companies, with 14 of the 20 properties in the REIT’s portfolio sourced through TriWest • High Quality Portfolio Focused on Strategic Single Tenant Properties – Consists of 100% occupied industrial real estate that is primarily mission critical to its tenants • Attractive Yield Through Stable Distributions; Strong Fundamentals – ~8.6% cash distribution yield with a YTD Q2 AFFO payout ratio of 74.5%, down from 78.4% for 2015 – Consistent AFFO per unit growth with 2015 AFFO per unit 3.0% higher than 2014 3

Capitalization and Trading Overview Capitalization Unit Price Performance Values in $M except per share amounts Share Price (September 2, 2016) $1.85 Shares Outstanding 41.5 Market Capitalization $76.7 Add: Net Debt $80.5 Enterprise Value $157.3 52 Week High $1.90 52 Week Low $1.40 Share Price as a % of 52 w eek high 97.4% Key Financial Metrics Price to 2016E FFO 9.5x Commentary Price to 2016E AFFO 9.3x A. 14-JAN-14 Completed a $68M acquisition of ten industrial properties located in Western Canada Price to 2017E FFO 9.0x totaling 436,412 square feet and ~122 acres of land Price to 2017E AFFO 8.4x B. 15-JUL-14 Completed a $19.2M public equity offering and a $35.7M acquisition of three industrial properties in Alberta totaling 277,748 square feet and 57 acres of land 2016E AFFO Payout Rat 80.6% Debt to GBV 49.2% C. 6-JUL-15 Announces agreement to acquire two industrial properties for $16M in BC and Ontario financed by a VTB of $12.3M and $3.7M in cash Distribution Yield 8.6% D. 20-JUL-15 Announces agreement to acquire an industrial property in Alberta for approximately $22M NAV per unit $2.15 financed by a VTB of $2.0M, assumption of $11.6M in mortgages, and $8.5M in cash Premium (Discount) to N (14.0%) E. 04-NOV-15 Announces agreement to acquire two industrial properties for $12.1M in BC and Saskatchewan financed by a VTB of $5.3M and $6.8M in cash Implied Cap Rate 8.3% F. 27-JUL-16 Announces agreement to acquire an industrial property in Cambridge, Ontario for $8.4M 2016E AFFO Yield 10.7% financed by a VTB of $1.9M and $6.5M in cash 4 Source: FactSet, Bloomberg, and Consensus Research

$50 Million of Acquisitions in 2015 The transactions added $50M of asset value, increasing total assets to over $160M and added $19.6M of market capitalization via vendor take-backs at a premium to the then market price 455 Welham Road, Barrie, ON 4700 & 4750 102 Avenue SE, Calgary, AB Date: July 2015 August 2015 Date: GLA: 109,366 GLA: 29,471 Price: $21.9M Price: $8.5M Canada Tenant: Tenant: Prodomax Cartage * Going-in cap rate of 7.6%; financed with a VTB of $2.0M, the assumption of a * Combined going-in cap rate for the Barrie and Kelowna acquisition of 7.6%. $11.5M mortgage and cash of $8.5M. Both acquisitions were financed with a VTB of $12.3M and cash of $3.7M. 555 Adams Road, Kelowna, BC 4271-5 Avenue East, Prince Albert, SK December Date: July 2015 Date: 2015 GLA: 94,594 GLA: 24,600 Price: $7.5M Price: $4.6M Tenant: Various Tenant: Broda * Going-in cap rate of 8.0%; financed with a VTB of $3.2M and $1.4M in cash. * Multi-tenant industrial property; tenants include Reidco Metal Industries, Concept Manufacturing, and OPT Precision Tool Manufacturing (average lease terms of 3.8 years). 1) Edgefront also completed the acquisition of a multi-tenant industrial property in Prince George, BC at a going-in cap rate of 7.9% on December 1, 2015 for $7.5M 5

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.