Review Review Commodity prices have seen a surge in recent years - PDF document

What role for speculators in driving commodity prices? MPDD Seminar April 5, 2012 Margit Molnar and Yusuke Tateno UNESCAP Macroeconomic Policy and Development Division Review Review Commodity prices have seen a surge in recent years

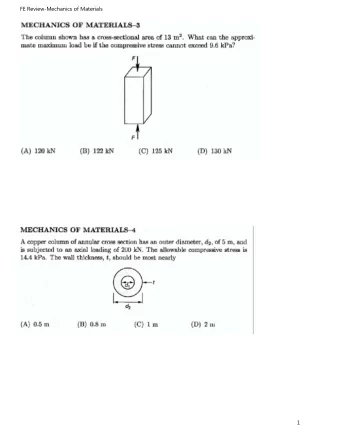

What role for speculators in driving commodity prices? MPDD Seminar April 5, 2012 Margit Molnar and Yusuke Tateno UNESCAP Macroeconomic Policy and Development Division Review Review Commodity prices have seen a surge in recent years 800 All primary commodities 700 Food Price index (1992=100) Agricultural raw materials 600 Metals 500 Energy 400 300 200 100 0 2 4 6 8 0 2 4 6 8 0 2 9 9 9 9 0 0 0 0 0 1 1 9 9 9 9 0 0 0 0 0 0 0 1 1 1 1 2 2 2 2 2 2 2 1

Review Review Economic fundamentals do not fully explain commodity price hikes Physical demand factors have limited role 16% 600 Commodity price index (1992=100) Food imports 14% 500 Fuel imports 12% Food price index (right scale) Import shares 400 Fuel price index (right scale) 10% 8% 300 6% 200 4% 100 2% 0% 0 8 0 2 4 6 8 0 2 4 6 8 0 8 9 9 9 9 9 0 0 0 0 0 1 9 9 9 9 9 9 0 0 0 0 0 0 1 1 1 1 1 1 2 2 2 2 2 2 Review Review What else? – Supply-side constraints – Export restriction – Financial investors 2

Financialisation of commodities of commodities Financialisation Flight to simplicity (exodus from ABS etc. complicated products) Monetary easing – (at lower interest rates producers have lower incentives to increase production so that the proceeds can be invested in high-yield instruments) Speculators Speculators investors not actually holding commodities but seeking arbitrage opportunities in commodities futures and options markets – hedge funds – financial institutions – commodity trading advisors – commodity pool operators – associate brokers – introducing brokers – floor brokers – and other non-commercial traders 3

Do speculators play a role? Do speculators play a role? How to pin down their effect? comparing the price changes in commodities with and without organised futures markets . If speculators play a role, commodity with futures markets should have different price behaviour from non- speculatable commodities. Correlation of price changes Correlation of price changes 0.8 0.6 0.4 0.2 0 -0.2 -0.4 2 4 6 8 0 2 4 6 8 0 9 9 9 9 0 0 0 0 0 1 9 9 9 9 0 0 0 0 0 0 1 1 1 1 2 2 2 2 2 2 Average correlation of speculatable commodities Average correlation of non-speculatable commodities 4

Do speculators play a role? Do speculators play a role? How to pin down their effect? comparing the price changes in commodities with and without organised futures markets . If speculators play a role, commodity with futures markets should have different price behaviour from non- speculatable commodities. Due to substitution and other effects, also non- speculatable commodity prices tend to rise if those with organised futures markets rise, though it should happen with a lag . Korniotis (2009) shows that the comovement between metals with and without futures contracts has not weakened in recent years as speculative activity has risen How to pin down speculators ’ How to pin down speculators ’ effects effects (cont.) (cont.) look at the changes in positions in futures and options markets of non-commercial traders . To what extent position changes by non- commercial traders, in particular hedge funds etc. are associated with price changes? 5

An additional idea An additional idea Framework: cointegration among commodity price inflation, non- commercial trader positions and monetary/financial market conditions Test for the absence of cointegration by determining whether there exists error correction for individual panel members or for the panel as a whole. The tests are general enough to allow for a large degree of heterogeneity, both in the long-run cointegrating relationship and in the short-run dynamics, and dependence within as well as across the cross-sectional units. The relationship exists for several choices of monetary/financial market conditions (currency in circulation, M1, M2, M3, credit, exchange rate, stock price indices) evidence of cointegration for the panel as a whole and for a number of lag choices VECM: check the short- and long-term impacts of speculators on commodity price inflation Estimated equation Estimated equation ln p ln m ln s ln m ln s [ s ](ln p { s } ln m i , t i , t 5 0 1 i , t 1 i , t 1 1 i , t 1 i , t 1 2 , 3 , 4 , 1 2 i t i t i t s T ) T i i , t 2 i , t 1 3 i where p indicates price of a commodity, m is a monetary variable, s is speculation, all in logarithmic forms and T is the time trend. Panel dataset of 9 commodities over Jan 2009-May 2011 6

Preliminary results Preliminary results non- non-commercial reported mzm m3 SP500 mzm Short-term coefficients Money supply (growth) + + + Speculators' net position (change) + + + Money supply (level) - + Speculators' net position (level) + + + + Time trend + + Dynamic coefficient - - - - Long-term coefficients Money supply -(14%) + Speculators' net position + + + +(12%) Trend +(14%) + Interaction term coefficients Speculators' np - price +(15%) + Speculators' np - Money supply + + + Summary – – What What ’ s role for speculators? Summary ’ s role for speculators? Boost commodities prices both in the short and in the long run Tighten the link between monetary/financial variables and commodity prices In some cases decelerate the speed of adjustment of prices back to equilibrium after experiencing a shock 7

Future directions Future directions Demand control – World production biggest demand from countries with low production efficiency Extension of time series and coverage of commodities Explore cross-market linkages and regional dimension Thank you! 8

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.