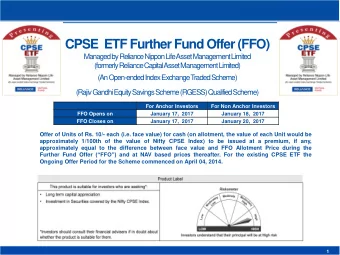

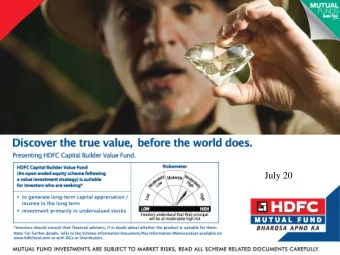

Reliance Capital Builder Fund – Series C (A Close Ended Equity Oriented Scheme) Offer for Sale of Units at Rs.10/- per unit during the new fund offer period Tenure – 3 Years from the date of allotment of units NFO Opens – September 17, 2014 NFO Closes – October 1, 2014

Reliance Capital Builder Fund – Series C is suitable for investors who are seeking*: · Long term capital growth · Investment in diversified portfolio of equity & equity related instruments with small exposure to fixed income securities · High risk. (BROWN) *Investors should consult their financial advisers if in doubt about whether the product is suitable for them. Note: Risk is represented as: (BLUE) investors understand (YELLOW) investors (BROWN) investors that their principal will be at understand that their principal understand that their principal low risk will be at medium risk will be at high risk Slide 2

Market Outlook 3 Slide

India: Nascent Bull Market Stage* Macro economic recovery already visible Decisive political mandate after 30 years Huge pent up demand due to severe domestic under investment in equity markets Valuation still favorable for long term wealth creation 2008 2014 S&P BSE Sensex Levels 20873 26638 Markets At Life Time Highs……But Earnings Per Share (EPS) 833 1418 Trailing P/E (Price To Earnings) ~28x ~19x Forward P/E ~24x ~17x Market Cap To GDP Ratio 103% ~70% Source: Bloomberg, RCAM estimates August 28, 2014. * RCAM Internal View 4 Slide

India: Now & Then Parameter Month 2013^ 2014* Manufacturing PMI August 48.5 52.4 Index of Industrial -1.8% 3.4% June Production 1.3 lacs 1.4 lacs Passenger Car Sales July 9.64% 7.96% CPI Inflation July Exports 25,835 27,728 July (USD million) 4.9% 4.5% Fiscal Deficit March Foreign Reserves 278 319 August (USD billion) 4.7% 5.7% GDP Growth June Source: Bloomberg . * Data is the last published number .^ Data is the numbers a year back from the last published number. 5 Slide

Equity markets perform in the long term S&P BSE Sensex has given positive returns 23 out of the 35 years Markets have given an average return of 25% S&P BSE Sensex Annual Returns (%) 35 year CAGR Out of 35 years: (1979 to 2014): 16.7% 23 years of positive returns 12 years of negative returns Past performance may or may not be sustained in future Source: Bloomberg, Annual returns above refer to absolute returns & are Financial Year returns. 6 Slide

Significant turnaround in equity markets Better macro numbers & stable political environment leading to recovery of equity markets Sharp recovery after prolonged period of sluggish market conditions Performance of Equity Markets 210 (July 2013 – August 2014) 190 S&P BSE Sensex 170 S&P BSE Midcap 150 S&P BSE Smallcap 130 110 90 Jul-13 Jan-14 Mar-14 Jun-14 Sep-13 Nov-13 May-14 Aug-14 Past performance may or may not be sustained in future. Source: MFIExplorer. Index values have been normalized. 7 Slide

Market valuations still favorable for wealth creation Valuations are at long term average level Forward P/E Forward P/BV 25 S&P BSE Sensex S&P BSE Sensex 6 5 20 Average 4 15 Average 3 10 2 5 1 Aug-05 Aug-06 Aug-07 Aug-08 Aug-09 Aug-10 Aug-11 Aug-12 Aug-13 Aug-14 Aug-05 Aug-06 Aug-07 Aug-08 Aug-09 Aug-10 Aug-11 Aug-12 Aug-13 Aug-14 Past performance may or may not be sustained in future Source: Bloomberg Estimates. P/E = Price to Earnings ratio. P/BV = Price to Book Value ratio. 8 Slide

Market Cap to GDP is below 2007-08 levels Current level is lower than the last bull market of 2007-08 Case for expansion in India’s market cap Market Cap to GDP (%) 120 103 95 100 88 Average: 72% 83 82 80 65 72 63 69 55 60 52 42 40 20 0 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15E Past performance may or may not be sustained in future Source: Bloomberg, MOSL estimates 9 Slide

Key Drivers going forward 10 Slide

Pace of Indian GDP growth has improved While the first trillion dollars required 58 years, the next trillion dollars in GDP required only 7 years 4,194 4 th US$ tn India GDP Trend (USD) 3,886 FY51- 08: 7.3% CAGR 4 years 3,601 The Next Trillion Dollar Opportunity FY08- 15: 7.9% CAGR 3,337 3 rd US$ tn 3,092 5 years 2,865 2,655 2,460 2,280 2 nd US$ tn 2,113 7 years 1,879 1,878 1,858 1,708 1 st US$ tn 1,366 58 years 1,239 1,226 948 834 721 618 523 492 464 475 293 150 57 33 21 FY51 FY60 FY70 FY80 FY90 FY00 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E FY18E FY19E FY20E FY21E FY22E FY23E FY24E Past performance may or may not be sustained in future Some of the above data are only estimates & actual data may vary depending on various market & economic factors. Source: Central Statistical Organization, MOSL estimates 11 Slide

India expected to lead in the emerging market space Highest EBITDA & PAT growth for FY14 to FY16 Highest ROE with reasonable average Lowest PEG; cheapest among emerging markets Growth (CAGR FY 14 – 16e) RoE (%) No. of Net Debt/ Country PEG Cos Equity Sales EBITDA PAT 2013 2014 2015e 2016e China 89 6% 9% 12% 13% 13% 13% 13% 47% 1.2 India 123 8% 14% 15% 16% 16% 17% 17% 53% 1.0 Australia 32 4% 6% 6% 10% 16% 16% 15% 38% 1.9 South Korea 47 5% 7% 11% 12% 15% 15% 15% 31% 1.2 South Africa 19 6% 2% 2% 13% 18% 17% 15% 42% 4.9 Taiwan 20 8% 8% 8% 16% 17% 16% 16% -9% 1.6 Saudi Arabia 15 4% 3% 4% 14% 15% 15% 14% 31% 3.5 Singapore 15 9% 9% 10% 11% 10% 11% 11% 23% 1.6 Malaysia 16 5% 8% 8% 12% 11% 12% 12% 13% 1.9 Indonesia 14 11% 10% 12% 20% 19% 19% 19% 8% 1.4 World 1,563 5% 8% 10% 15% 15% 15% 15% 41% 1.3 Past performance may or may not be sustained in future Source: Bloomberg estimates. EBITDA = Earnings before interest, taxes, depreciation & amortization, PAT = Profit before tax, RoE = Return on Equity, PEG = Price to Earnings Growth. The above analysis is done on the top 200 market cap companies of each above mentioned country. From this subset the following filters have been applied excluding companies which are 1) listed in multiple country exchanges 2) do not have published data for the specified years in Bloomberg & 3) financial companies. The above no of companies is the remaining after applying all the above filters. Some of the above data are only estimates & actual data may vary depending on various market & economic factors. 12 Slide

Growth recovery on track Indian GDP growth expected to pick up Recent Budget proposals show the intent of improving growth rates GDP Growth (%) Past performance may or may not be sustained in future Source: Central Statistical Organization, MOSL estimates. 13 Slide

Economic Recovery leads to higher earnings High correlation between company earnings & GDP Growth In the last bull market of 2007-08, Sensex earnings growth had reached a high of 37% 43.0% 12.0% Earnings growth 38.0% Sensex Earnings Growth GDP Growth 10.0% 33.0% 28.0% 8.0% GDP Growth 23.0% 6.0% 18.0% 13.0% 4.0% 8.0% 2.0% 3.0% -2.0% 0.0% Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Past performance may or may not be sustained in future Source: Bloomberg. Earnings growth is of S&P BSE Sensex. 14 Slide

Corporate profits to GDP likely to revert to mean Corporate profits to GDP is below the long term trend Mean reversion of corporate profits to long term average may lead to earnings revival Corporate Profit to GDP (%) 9 7.8 Average: 5.5% 8 7.3 6.5 6.2 7 6.3 5.6 4.9 6 5.4 5.4 4.6 4.3 4.4 4.6 4.9 4.7 5 4 3 3 2 1 0 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E FY18E Past performance may or may not be sustained in future Some of the above data are only estimates & actual data may vary depending on various market & economic factors. Corporate Profit above is Profit after Tax of all listed companies. Source: MOSL Estimates 15 Slide

Earnings Growth expected to propel equity markets After a subdued 8% EPS growth period, Sensex EPS expected to grow 2,500 25,000 EPS 2,190 S&P BSE Sensex FY08-14: 8% CAGR 2,000 20,000 1,836 1,524 Sensex EPS Index Level 1,500 15,000 1,340 FY03-08: 25% CAGR 1,183 1,123 1,024 1,000 10,000 833 820 834 718 450 523 216 236 272 348 500 5,000 0 0 FY2001 FY2002 FY2003 FY2004 FY2005 FY2006 FY2007 FY2008 FY2009 FY2010 FY2011 FY2012 FY2013 FY2014 FY2015E FY2016E FY2017E Past performance may or may not be sustained in future Source: Bloomberg, MOSL estimates. EPS = Earnings per share. 16 Slide

Budget Announcements – Furthering Growth Big sector Reforms in banking, housing, infrastructure reforms & rationalizing tax reforms Opening sectors FDI cap for defence, railways & insurance was raised for FDI Fiscal Fiscal deficit target was left unchanged; roadmap for fiscal consolidation consolidation Focus on Measures to attract capital inflows & to boost household Investments disposable income (higher exemption & tax deduction limit) Commitment to address structural issues in the supply side to Inflation contain inflation; setting up a fund to smoothen out fluctuations in food prices Source: Ministry of Finance 17 Slide

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries