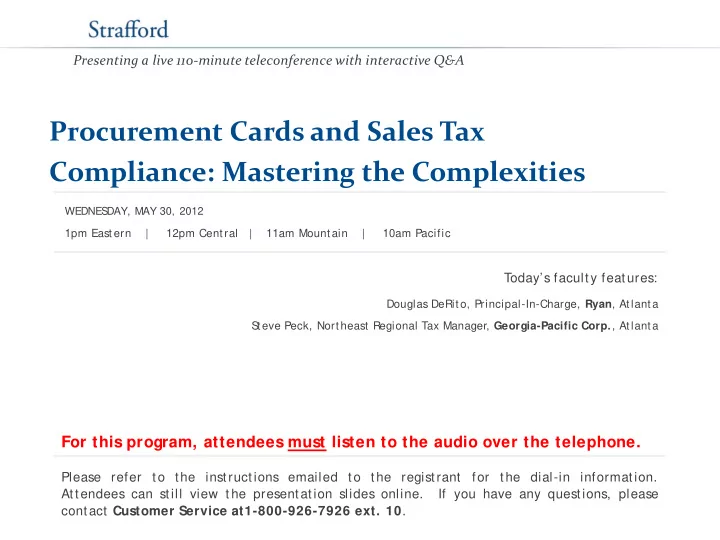

Presenting a live 110-minute teleconference with interactive Q&A Procurement Cards and Sales Tax Compliance: Mastering the Complexities WEDNES DAY, MAY 30, 2012 1pm East ern | 12pm Cent ral | 11am Mount ain | 10am Pacific Today’s faculty features: Douglas DeRit o, Principal-In-Charge, Ryan , At lant a S t eve Peck, Nort heast Regional Tax Manager, Georgia-Pacific Corp. , At lant a For this program, attendees must listen to the audio over the telephone. Please refer to the instructions emailed to the registrant for the dial-in information. Attendees can still view the presentation slides online. If you have any questions, please contact Customer Service at1-800-926-7926 ext. 10 .

Conference Materials If you have not printed the conference materials for this program, please complete the following steps: • Click on the + sign next to “ Conference Materials” in the middle of the left- hand column on your screen. • Click on the tab labeled “ Handouts” that appears, and there you will see a PDF of the slides for today's program. • Double click on the PDF and a separate page will open. • Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY Attendees must listen to the audio over the telephone . Attendees can still view the presentation slides online but there is no online audio for t his program. Attendees must stay on the line for at least 100 minutes in order to qualify for a full 2 credits of CPE. Attendance is monitored as required by NAS BA. Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10 .

Tips for Optimal Quality S ound Qualit y For this program, you must listen via the telephone by dialing 1-866-873-1442 and entering your PIN when prompted. There will be no sound over the web connection. If you dialed in and have any difficulties during the call, press *0 for assistance. Y ou may also send us a chat or e-mail sound@ straffordpub.com immediately so we can address the problem. Viewing Qualit y To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

Procurement Cards and Sales Tax: Mastering the Complexities Seminar May 30, 2012 Douglas DeRito, Ryan S teve Peck, Georgia-Pacific doug.derito@ ryan.com smpeck@ gapac.com

Today’s Program P-Card Compliance Difficulties, And Options S lide 7 – S lide 11 [Douglas DeRit o] Working With Issuers Of P-Cards S lide 12 – S lide 13 [Douglas DeRit o] P-Card Experiences, Best Practices At Georgia-Pacific S lide 14 – S lide 24 [S t eve Peck]

Douglas DeRito, Ryan P-CARD COMPLIANCE DIFFICULTIES, AND OPTIONS

Use Of Corporate Procurement Cards • Overview • Procurement card operations/ background • S ales and use tax issues • S tate practices for verification of sales tax paid and use tax accrual and remittance • Tax compliance issues • Current card user practices/ best practices 8

Sales And Use Tax Issues • Level of data (Level 1, 2, 3) • Merchant community responsibility • Determining if sales/ use tax is due, and rate application • S ales and use tax information must be retained for verification on state audit. • S ometimes, it is difficult to determine when and where a sale took place. • Internal controls for, and procedures around, P-card usage will determine the sales/ use tax compliance needs of an enterprise. 9

State Practices For Verification Of Sales Tax Paid, Use Tax Accrual And Remittance • Manual review and verification • Estimation methods • Combination approaches • Vendor requirements • Card user requirements • Card issuer requirements 10

Tax Compliance Issues • Tax-sensitized documentation for each transaction • Information and documentation required • What information is currently available? • What internal controls are in place? • P-card processes and integration with compliance procedures • How P-cards are used can drive tax decision needs. 11

Douglas DeRito, Ryan WORKING WITH ISSUERS OF P-CARDS

Working With P-Card Issuers • Level 1, Level 2, Level 3 data complexities • Currently, P-Card issuers are not focused on providing sufficient data for tax rate application and tax management. How P-Cards are used can drive tax decision needs. • The merchant community is inconsistent with the level of data being provided. • Card brand name can provide the infrastructure for transaction management. • Discounts are provided for proactive tax management, in some cases. • S eparate P-Card usage: Exempt and non-exempt purchases. 13

Steve Peck, Georgia-Pacific P-CARD EXPERIENCES, BEST PRACTICES AT GEORGIA- PACIFIC

Background I. Georgia-Pacific was a Fort une 500 company until its purchase by Koch in late 2005; it is now privately held. II. Manufacturer of cellulose tissue, paper, corrugated/ packaging and building products including lumber, plywood, OS B, gypsum and chemicals III. Manufacturing/ converting locations, as well as offices, warehouses domestically in about 35 states IV . Began using P-cards in the early 1990s but for years (until turn of the millennium) only for office products and inconsequential, low-dollar purchases V . About 3,000 P-cards are now in use, with significant annual spending (about 250,000 transactions) VI. Usage is ramping up, both in terms of dollars, types of purchase activity and across all business units 15

Overview Of Sales And Use Factors I. 75% of merchants are Level 1. Charge is transmitted to bank to pass to the company, and does not include a separate tax charge. A. Primary challenge is to ascertain what transactions have not been taxed by the merchant. B. S ome merchants that have Level II capabilities are not sending the separate tax amount; expeditious vs. tax accuracy. II. P-cards are widely distributed to users for a wide array of purchase activities. A. Not limited to vendors [or super-vendors] or restricted to certain types of goods/ services B. No leverage to sales and use tax based on specific merchant or type of spending 16

Overview Of Sales And Use Factors (Cont.) III. Burden is on the P-card holder to review receipts for tax and input in allocation program, if tax was indeed part of the Level I gross amount. IV . Key point : If cards were designat ed for cert ain “ super” vendors or assigned t o cert ain spending, t hat would aid and abet t ax review and cont rol t ax exposure. This has not been our pat t ern or experience. 17

P-Card Technical Tax Configuration I. Banks, in our experience, have not programmed allocat ion programs t o address t ax considerat ions. II. Georgia-Pacific designed a cust om sales and use funct ionalit y t o int egrat e wit h our Vert ex TDM AP syst em. A. Paid bank modified it s user allocat ion program t o accommodat e. B. Tax codes incorporat ed: 1. ME = Manufact uring exempt 2. S E = S ervice exempt 3. MS = Manufact uring special rat e 4. GT = General t axable “ GT” default s, if user leaves blank 18

P-Card Technical Tax Configuration (Cont.) III. Tax amount must be keyed by P-card holder, if tax amount sent by bank was left blank or zero. If receipt shows no tax paid, then 0.00 must be keyed. IV . Users must select the appropriate tax code at the line level, during the monthly allocation to the GL account. A. S ome accounts are pre-set with exclusively exempt or taxable settings; TC has no impact. B. Automated validation: If taxable with 0.00 in sales tax amount, a use tax will be accrued 1. Use tax based on cardholder-assigned location 19

P-Card Technical Tax Configuration (Cont.) C. Unsatisfactory level of compliance with user tax coding 1. Encourage behavior modification, but it’s difficult to monitor and change since so often they wait until the last minute, have many transactions, do not keep receipts handy and do not feel the sting of the tax accrual D. Key point : If merchant / bank does not capt ure t ax [Level 1], a high burden is creat ed on t he user, and high- risk t ax will not be capt ured in program. Even if cust omized, it ’s difficult t o enforce appropriat e t ax code select ion. 20

Georgia-Pacific Procurement Initiative, ‘Procure To Pay’ I. Efficiency, economy-of-scale centralization, multi-year effort II. Obj ectives for cost containment are not congruent with sales and use compliance exposure limitation. A. PO => ERS (evaluated receipt settlement) B. Other/ non-PO => P-card 21

Georgia-Pacific Procurement Initiative, ‘Procure To Pay’ (Cont.) III. Both are fraught with tax complications. A. ERS : Facilitated by direct pay permit, but we only have ~half of facilities on direct pay B. P-card: Only 25% Level II or III, hence burden is on user; often falls short IV . Increase in P-card expectancy – enterprise-wide and dollar- wise. . Key point : Procurement direct ion can exacerbat e sales and V use t ax difficult ies. Be a part of t hat t eam; prepare economic response/ j ust ificat ion for t ax cust omizat ion, including t ax packages. 22

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries