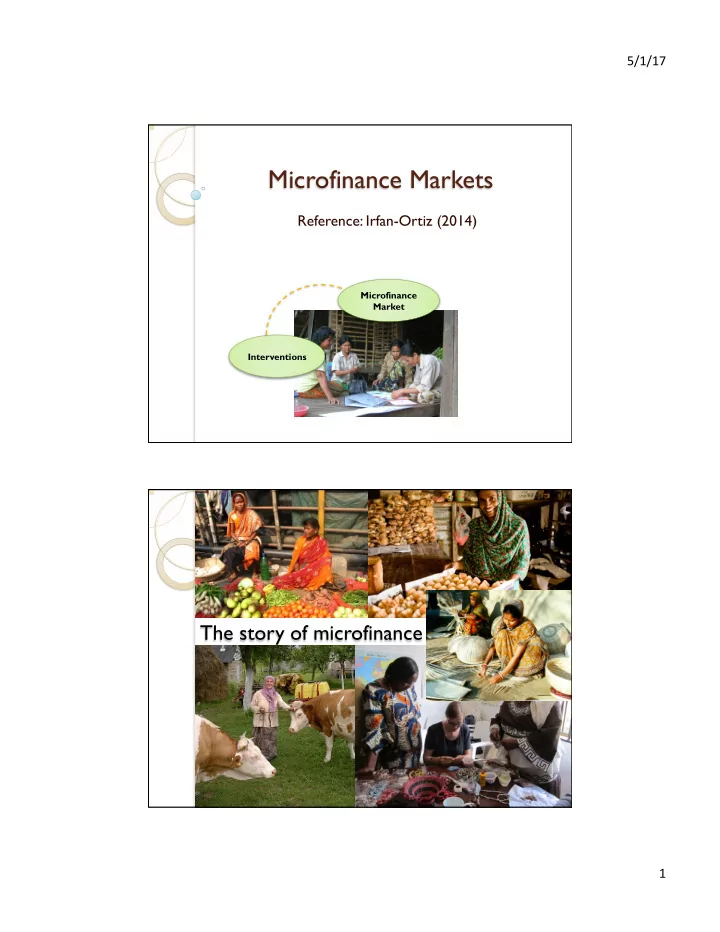

Microfinance Markets Reference: Irfan-Ortiz (2014) Microfinance - PDF document

5/1/17 Microfinance Markets Reference: Irfan-Ortiz (2014) Microfinance Market Interventions The story of microfinance 1 5/1/17 Story of microfinance movement 1970s to today Story of microfinance movement 2 5/1/17 Story of microfinance

5/1/17 Microfinance Markets Reference: Irfan-Ortiz (2014) Microfinance Market Interventions The story of microfinance 1

5/1/17 Story of microfinance movement 1970s to today Story of microfinance movement 2

5/1/17 Story of microfinance movement Dr. Muhammad Yunus Congressional Gold Medal (2013) Nobel Peace Prize (2006) Loan without collateral! Yet very low default rate What makes it work: ◦ Group lending with joint-liability contract ◦ Group lending mitigates "moral hazard" Also reduces monitoring costs ◦ Assortative matching mitigates "adverse selection problem" 3

5/1/17 Interest rates Not "weapon for competition" among banks (Porteous, 2006) Other factors ◦ Loan size ◦ Shorter waiting period ◦ Flexibility in repayment ◦ Savings account ◦ Health care More on microfinance The Economics of Microfinance (Armendariz and Morduch, 2010) 4

5/1/17 What do we want to do? Model microfinance markets Goal: assist policy makers Questions • Shut down loss-making banks? • Set a cap on interest rates? • Subsidize banks? Causal Strategic Inference (CSI) Causal probabilistic inference (Judea Pearl) ◦ Prediction ◦ Intervention ◦ Counterfactual Interventions in game-theoretic settings ◦ Set the actions of certain players (Irfan & Ortiz, AI Journal, 2014) ◦ Change the structure of the game (this work) Modeling Learning Computation 5

5/1/17 Our model of microfinance market MFI = Microfinance institution Banks/MFIs Villages ✔ Equilibrium MFIs want ◦ Set interest rates s.t. supply = demand Villages want ◦ Maximize amount of loan s.t. repayment Related: Graphical Economics (Kakade, Kearns, & Ortiz, 2004) Diffusion of Microfinance (Jackson et al., 2013) Learning, Computation, Intervention Data: Bangladesh and Bolivia Example of Intervention: Shut down a loss-making bank Learn parameters before intervention 1 Learning method: bi-level optimization 2 Compute equilibrium: iterative algorithm 3 Remove the bank from model 4 Compute equilibrium again 6

5/1/17 Model of microfinance market T i Banks/MFIs i r i x ji Villages j k Revenue generated j k [slope: e k ] d k Amount of Loan Model of microfinance market Market clearance MFI side Nash Equilibrium: <interest rates, allocations> 1. MFI side is satisfied 2. Village side is optimized Village side 7

5/1/17 Special case: no diversification ( λ = 0) Assume: Villages have the same revenue function Equilibrium point exists; unique interest rates ◦ Proof: Equivalent Eisenberg-Gale convex program ◦ Polynomial-time algorithm to compute an equilibrium [Vazirani, 07] General case An equilibrium point exists ◦ Constructive proof: Use properties of strategic complementarity and strategic substitutability 8

5/1/17 Algorithm for equilibrium computation Using the model in the real world Data from Bangladesh and Bolivia MFIs Villages 9

5/1/17 Estimating model parameters Problem ◦ Learn the parameters from data ◦ Capture (approximately) the real-world scenario as a Nash equilibrium T i i r i Solution approach x ji ◦ Optimization j k Revenue generated j k [slope: e k ] d k Amount of Loan Optimization in machine learning 10

5/1/17 Equilibrium vs. observed allocations (Bolivia) 45000 40000 35000 Equilibrium Loan Allocations 30000 25000 20000 15000 10000 5000 0 0 5000 10000 15000 20000 25000 30000 35000 40000 45000 Observed Loan Allocations Observations Bias vs. variance ◦ Does not overfit Equilibrium selection ◦ Robust in the presence of noise 11

5/1/17 Bias vs. variance Add noise to data è Training set Calculate equilibrium Distance to observation è Test error Bias vs. variance Gaussian noise model 0.064 0.062 Training error Test Error Average Relative Deviation 0.06 0.058 0.056 0.054 0.052 0.05 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1 Noise Level 12

5/1/17 What do we want to do? Model microfinance markets Goal: assist policy makers Causal Strategic Inference (CSI) Questions • Shut down loss-making MFIs? • Set a cap on interest rates? • Subsidize banks? Shut down loss-making MFIs Competition vs. interest rates 16 [D. Porteous, 2006] Observed interest rates Learned interest rates 14 Equilibrium interest rates 12 Interest Rates 10 8 6 4 2 0 1 2 3 4 5 6 7 MFIs BRAC ASA PKSF GRAM BRDB PDBF Other 13

5/1/17 Cap on interest rates 16 Observed interest rates 13.4975% Learned interest rates 14 Equilibrium interest rates 12 Interest Rates 10 [July 2011] 8 Cap on interest 6 rates 13.5% 4 2 0 1 2 3 4 5 6 7 MFIs BRAC ASA PKSF GRAM BRDB PDBF Other Role of subsidies 26 Before giving subsidies 25 After giving subsidies Interest Rates 24 23 22 21 1 2 3 4 5 6 7 8 MFIs 14

5/1/17 Other inference questions New branches How to make loans more affordable by subsidies Major bank going out of business In brief… Model microfinance markets Economics Learn the parameters Machine Learning Answer CSI questions Algorithms Extensions (with Lucy Luo & Marcus Christiansen) ◦ Diminishing marginal returns on investing loan ◦ Model village side preference ◦ Model group lending ◦ Consider MFI-level characteristics 15

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.