SLIDE 1

The Numbers Don’t Lie: Interpreting Brookfield Business Partner’s $1.05 Per Unit Offer for Teekay Offshore (NYSE:TOO) June 19, 2019

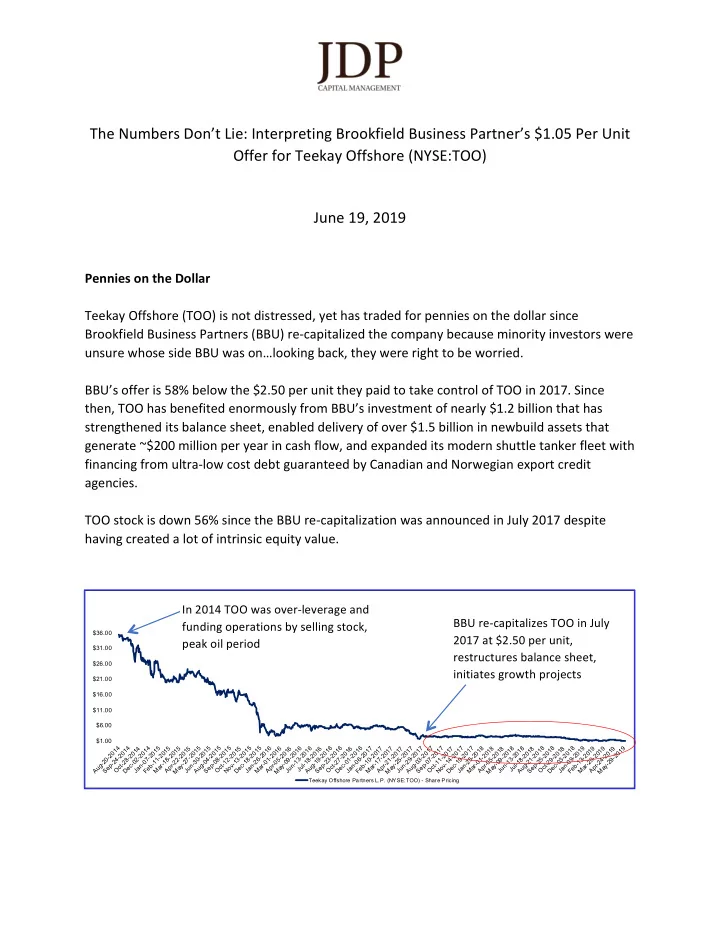

Pennies on the Dollar Teekay Offshore (TOO) is not distressed, yet has traded for pennies on the dollar since Brookfield Business Partners (BBU) re-capitalized the company because minority investors were unsure whose side BBU was on…looking back, they were right to be worried. BBU’s offer is 58% below the $2.50 per unit they paid to take control of TOO in 2017. Since then, TOO has benefited enormously from BBU’s investment of nearly $1.2 billion that has strengthened its balance sheet, enabled delivery of over $1.5 billion in newbuild assets that generate ~$200 million per year in cash flow, and expanded its modern shuttle tanker fleet with financing from ultra-low cost debt guaranteed by Canadian and Norwegian export credit agencies. TOO stock is down 56% since the BBU re-capitalization was announced in July 2017 despite having created a lot of intrinsic equity value.

$1.00 $6.00 $11.00 $16.00 $21.00 $26.00 $31.00 $36.00 Aug-20-2014 Sep-24-2014 Oct-28-2014 Dec-02-2014 Jan-07-2015 Feb-11-2015 Mar-18-2015 Apr-22-2015 May-27-2015 Jun-30-2015 Aug-04-2015 Sep-08-2015 Oct-12-2015 Nov-13-2015 Dec-18-2015 Jan-26-2016 Mar-01-2016 Apr-05-2016 May-09-2016 Jun-13-2016 Jul-18-2016 Aug-19-2016 Sep-23-2016 Oct-27-2016 Dec-01-2016 Jan-06-2017 Feb-10-2017 Mar-17-2017 Apr-21-2017 May-25-2017 Jun-29-2017 Aug-03-2017 Sep-07-2017 Oct-11-2017 Nov-14-2017 Dec-19-2017 Jan-25-2018 Mar-01-2018 Apr-05-2018 May-09-2018 Jun-13-2018 Jul-18-2018 Aug-21-2018 Sep-25-2018 Oct-29-2018 Dec-03-2018 Jan-09-2019 Feb-13-2019 Mar-20-2019 Apr-24-2019 May-29-2019

Teekay Offshore Partners L.P. (NYSE:TOO) - Share Pricing