Economic Crisis Economic Crisis (In INR millions) and and A - PDF document

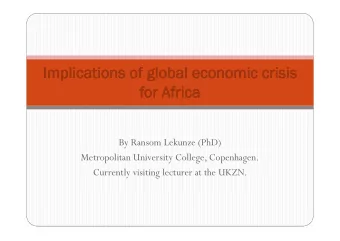

2/7/2009 Actual EBIT vs. Plan Excluding Special Items Economic Crisis Economic Crisis (In INR millions) and and A Strategy A Strategy 400 350 300 250 250 A K Chaudhuri A K Chaudhuri 200 Actual Director, ADAAP Process Solutions

2/7/2009 Actual EBIT vs. Plan Excluding Special Items Economic Crisis Economic Crisis (In INR millions) and and A Strategy A Strategy 400 350 300 250 250 A K Chaudhuri A K Chaudhuri 200 Actual Director, ADAAP Process Solutions Pvt. Ltd. Director, ADAAP Process Solutions Pvt. Ltd. 150 Plan 100 Visiting Faculty, Indian Statistical Institute Visiting Faculty, Indian Statistical Institute 50 & 0 Chairman, National Institution for Quality & Reliability, Chairman, National Institution for Quality & Reliability, 2004 2005 2006 2007 2008 Bangalore Bangalore 2 Don’t be blind to the need to change…….. Need to break existing paradigms “Iraqi Information Minister Mohammed “Our targets/business plan is a tremendous stretch, Saeed al-Sahhaf, standing on the roof of there is Baghdad's Palestine Hotel, denied his city no further opportunity to be had” had been invaded. “We are engaged and doing everything possible to meet our business goals” Sirens could be heard as he spoke and clouds of dust blew past.” “We have identified tactics to bridge the gap” Source: AP, April 7, 2003 3 4 • The Bubble has burst • We will emerge from this crisis • The world of economics will have changed forever • Future is probably brighter than ever Who controls the money? • Engineering • Sustainable accounting practices and business • Finance transparency becomes more prevalent. • Manufacturing • Manufacturing • During the good times it is very easy to be • Order Fulfillment successful and the opposite is equally true in a • Purchasing downturn situation. • Sales • Technology • Pedestrian managers make cut-backs in the traditional way – they reduce expenses in all “non- core” activities 5 6 1

2/7/2009 Quality Management Quality Management • Prudent organisations use the good times to prepare • In difficult times, you must be innovative – you must improve efficiency for the bad. and effectiveness. • Many have long predicted a bursting economic bubble; simply because • The companies that maintained that diligent focus history shows that the good times never roll forever. are the ones best positioned to ride this wave of uncertainty. During the good times it is very easy to • Regardless of the causes, we can safely predict that we will emerge be successful. But the opposite is true in a downturn. pp from this crisis. • The world of economics will have changed forever. • You must do a GREAT job at a GREAT price AND you • Business leaders will have been forced to adopt new processes and must provide GREAT service. strategies. We might suffer through a few difficult years. • But the future is probably brighter than ever as sustainable accounting practices and business transparency becomes more prevalent. Quality Management • Let’s not focus on cost reduction • Strategic plan as a positive business development • In difficult times, you must be innovative. You must exercise as opposed to a negative cost-slashing improve efficiency and effectiveness. process. • These times that we see great business leaders emerge and distinguish themselves from “pedestrian • Cost containment will be a feature of the plan, but managers.” only in so far as it supports the business • Core activities are considered to be customer development strategy. acquisition (sales, etc.) and production. acquisition (sales etc ) and production • A good strategy will plan for reduced competition, • The first areas to be downsized tend to be marketing, increased market share and increased customer quality analysis, training, etc. But this is, in my loyalty post-recession opinion, the wrong approach – it creates opportunities for competitors. It is overly simplistic. • The operational targets and KPIs assigned to operational business units. An approach to efficiency is very different from an approach to minimize headcount & transport costs. 10 Enterprise cost reduction is a wider approach Definition of Insanity? towards controlling the company's expenses and leading the organization towards improvement It does not only imply focusing on isolated cost “ Doing the same thing over and reduction exercise. Enterprise cost reduction over again and expecting a different addresses a number of key cost-aspects that span the enterprise, such as the business configuration, th t i h th b i fi ti result.” organizational structure and design, business and process complexity, external expenses and the Ben Franklin benefits. Politician 11 12 2

2/7/2009 Quality Management in Nineties and The importance of a management there after system Vision and Strategy Finally, engage in the above process as a dynamic, ongoing plan of service and customer experience innovation. In reality, the experts have mixed views about In reality, the experts have mixed views about Management System how long this downturn will last – so you must be prepared to continually innovate in a recessed economy for the foreseeable future. Fundamentals Projects Initiatives Quality Management in Nineties and Translating Strategy Into there after •Strategic planning processes now involve employees at every Results level and from every part of an organization. They also include customers, suppliers and even competitors. Hierarchical management structure is beginning to change dramatically with the introduction of self-directing work teams. --a systematic method to y •Service Level Agreements have created completely new Service Level Agreements have created completely new measure, analyze and improve working relationships for the internal service providers like business processes to identify laboratories, archives, IT functions etc. to expand the organization and focus on performance results and customer critical areas that can cause satisfaction measurements. breakthrough results in •Self-directing work teams. Organizations, increasingly process- market penetration, focused, are destroying the former barriers in the form of Quality organizational speed and the specialists that limited their progress. cost of doing business. 16 Introduction Haul up sail fast and right to stand on course ! Traditional Financial Reporting: � Focus only on financial indicators, not the business KPI’s � Story of past events � Overwhelming dataflow, limited information � No link with the strategy “Less than 10% of the formulated strategies are really implemented” 17 18 3

2/7/2009 WHAT IS THE PURPOSE OF A W E NEED TO MAKE I T BUSINESS ORGANISATION? � focused on the future • Investors are moving towards total shareholder return on � derived from the strategy their investment in a company. � not only a controlling system , but not only a controlling system , but also a m anagem ent system , • A strategy geared towards value creation is an essential part of forward-looking business. incorporating all KPI ’s • This will enable a business to attract and retain further capital for growing businesses. 19 20 Operational decisions affect value VALUE DRIVERS? Efficient Operations → Managing costs within threshold parameters → Understanding the impact of cycle times on value •Volume growth → Focussing the right resources on the right issues → Balancing innovation with risk and return •Margin growth •Optimum working capital O ti ki it l Value Target •Reduce value destroyers Optimal Business Mix → Evaluating / segmenting •Lower cost of capital the Value Potential of Products/ Optimal Capital Base → Managing existing and planned capital needs Services → Focussing on differentiating → Creatively taking advantage of tax rates ………. core competencies → Managing Fixed Assets 21 22 • Design Corrective Action, Rew ork-Design • Poor Docum entation • Excess W I P, Excess RM I nventory, Excess FG Change, Scrap-Design Change I nventory,Excess Tool Consum ption ,Excess Die • Purchasing Failure Costs Consum ption ,Custom er Com pliant I nvestigation • Purchased Material Reject Disposition • Returned Goods ,Retrofit Costs ,W arranty Claim s • Purchased Material Replacem ent Costs • Recall Costs ,Liability Costs ,Penalties • Other External Failure Costs ,Purchasing Appraisal • Supplier Corrective Action,Rew ork of Costs ,I ncom ing I nspection and Test ,Measurem ent Supplier Rejects ,Uncontrolled Material Equipm ent Qualification of Supplier Product Losses ,Manufacturing Failure Costs Source I nspection and Control Program s • Material Review / Corrective Action M t i l R i / C ti A ti Manufacturing Appraisal Costs Disposition Costs Planned I nspections, Tests, Audits Troubleshooting/ Failure Analysis Checking Labor Product or Service Quality Audits I nvestigation Support Costs I nspection and Test Materials Operations Corrective Action Set-Up I nspections and Tests ,Depreciation Allow ances Failure to Transfer from Design to Maintenance and Calibration Manufacturing ,Rew ork and Repair Outside Certifications Re-inspection/ Retest Costs, Failure to Scale External Appraisal Costs Field Perform ance Evaluations Up 23 24 4

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.