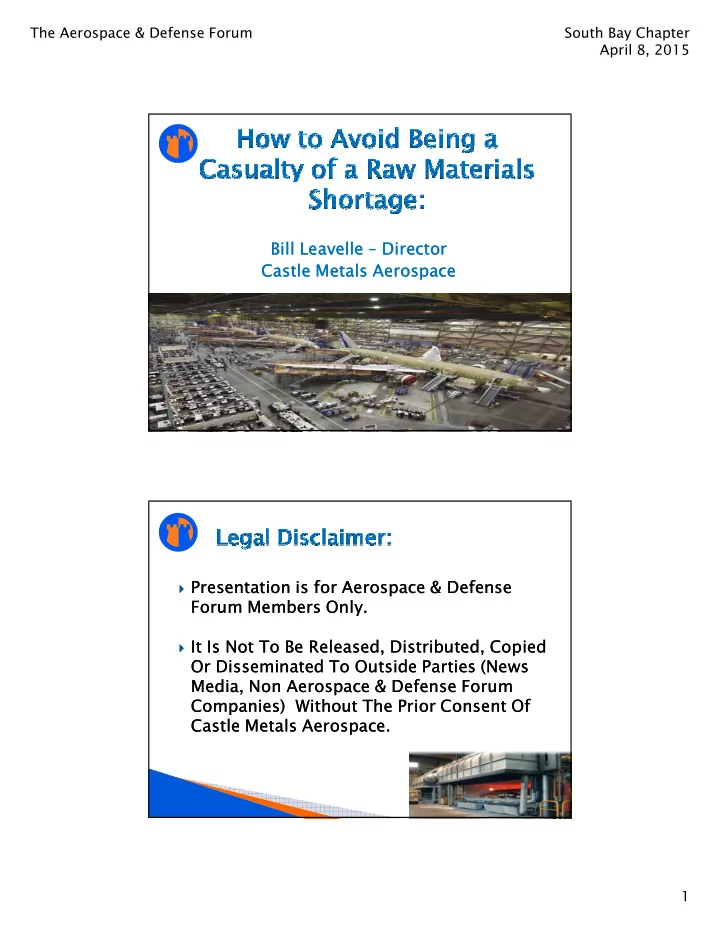

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 Bill Leavelle Bill Leavelle – Director Director Castle Metals Aerospace Castle Metals Aerospace 1 � Presentation is for Aerospace & Defense Presentation is for Aerospace & Defense � Forum Members Only. Forum Members Only. � It Is Not To Be Released, Distributed, Copied It Is Not To Be Released, Distributed, Copied � Or Disseminated To Outside Parties (News Or Disseminated To Outside Parties (News Media, Non Aerospace & Defense Forum Media, Non Aerospace & Defense Forum Companies) Without The Prior Consent Of Companies) Without The Prior Consent Of Castle Metals Aerospace. Castle Metals Aerospace. 1

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 � Introduction Introduction � � Market Market Undercurrents Undercurrents � � Effect of Market Effect of Market Forces and Disruptions Forces and Disruptions � � Aluminum Fundamentals & KPI’s Aluminum Fundamentals & KPI’s � � Titanium Fundamentals & KPI’s Titanium Fundamentals & KPI’s � � Nickel Fundamentals & KPI’s Nickel Fundamentals & KPI’s � � Aircraft Alloy Bar Fundamentals & KPI’s Aircraft Alloy Bar Fundamentals & KPI’s � � Market Predictions Market Predictions � � Summation Summation � 3 4 2

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 3

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 7 8 4

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 9 10 Source: Bill Bihlman- ‘Aerolytics’ 5

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 11 Source: Bill Bihlman- ‘Aerolytics’ 12 Source: Sanford Bernstein Research 6

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 13 14 7

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 � Indonesian Gov’t. Ban on Export of Nickel Ore: demanding Foreign Investment in Down-stream processing within country’s borders. � Further Consolidation in the Specialty Metals Market including: � Alcoa Purchase of RTI � Alcoa Purchase of Firth Rixon � PCC Purchase of Timet, Special Metals, & Caledonian Alloys/SOS. � Continued Political Uncertainty in Russia and the Ukraine 15 � New Titanium Sponge Capacity in India (Adding to Over-Supply) � China Titanium Smelters running at 40% and losing money. (30-35% of Global Supply) � VSMPO represents 30% of Global Supply (Russia) � High Reliance on Titanium Scrap in New Ingot Production (50-55% Recycled Content) driving Scrap prices higher. � Lack of Long Term EX-IM Bank guarantee adds uncertainty. 16 8

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 � Consolidation in the “End User” = Airlines � Oligopoly in Aircraft OEM’s � Raw Material Consolidation � Older, “Traditional” Producers (Alcoa/ATI/CRS) have different philosophies regarding Asset Utilization than newer entrants (PCC) � More likely to idle capacity than to try to “Sell” their way out of bad market. � Greater ‘Directed Supply’ means less flexibility and generally longer lead times. 17 � All are ‘forces’ which are aligning against the Tier II, III, IV suppliers, and could impact profitability. � The New “Reality”: Continuous Cost Cutting and Pricing Pressure is here to stay. � Raw Material Suppliers moving up the Supply Chain: Laser Cutting / Water Jet Cutting / Machining (RTI purchase of Remmele Eng.) � Machining Companies performing Component Assembly � Overall Consolidation of the Supply Chain. 18 9

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 19 � Four North American � Airframe OEM’s both Producers of Hard have Multi-Year Alloy “A&D” Fixed/Firm Aluminum Aluminum Plate Plate Contracts with all Four Producers Products � Kaiser, Aleris, Alcoa & Constellium 10

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 � Aero Aluminum Plate = � Aluminum Extrusions = Hectic Times Ahead ‘Status Quo’ � Three Separate 5% Price � No Major Price Increases Increases in last 18 months � 4 weeks for Small Press � CAGR = 9-1/2% Extrusions 2014 -2018 � 5-8 weeks for Medium � 20 week average Lead-time Press Extrusions for Aerospace Plate / Sheet � 18-30 Weeks for Large (Up 120% in 15 months) Press Extrusions � Longer for the Odd & � Daily P1020 Ingot at Unusual Grades / Sizes $.99/lb. (No Shortages) 21 � Aluminum Manufacturing Capacity – currently @ 78.1% (80-82% is considered ‘Full’ capacity) � Mill Shipments – Heat Treat Plate(Aero & Auto specifically) Up/Down YoY & M/M � Service Center Inventory level in Days of Supply: � 90 DSI +/- is ok. � >120 DSI is good for you, but bad for us. (Mostly) � <=75 DSI is bad for you, but good for us. (Mostly) � LME Pricing of Primary Ingot (P1020) 11

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 23 24 12

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 � Global Producer Market, � Price of Ingot unchanged more so than Aluminum. since June of 2014 at $8.60/lb. � VSMPO = World’s Largest @ 30% (Russia) � Outlook in “Pounds Shipped” is for 3% � China has 16 Large Growth in 2015. Producers – Largest Aerospace = Baoti � North American Major Producers = Timet, ATI, RTI, Carpenter . � Commercial Aerospace = 45% � General Industrial = 35% � Military and Defense = 10% � Medical and Commercial = 8% � Other = 2% 13

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 � Titanium Sponge Capacity Expansion in India & China, resulting in an oversupply situation. � Commercial Build Rate increases and Demand from Titanium “Intensive” Aircraft (787/A350/A380) � Defense Program Build Rate Increases (F35 Lightning II) and Foreign Sales of F-15 Strike Eagle � Increased Scrap ‘Revert’ Contracts and decreased production of Oil & Gas products/applications � Rising Price of 6AL4V Scrap (Base = $3.50/lb.) � Demand improving in Power Generation, Desalination, and other Industrial Markets. � Boeing and United Technologies purchase forward to mitigate risk in Supply Chain.(Greater than 6 months supply) � Sponge Operating Rate of greater than 50%. (Recycled Scrap = 50%-55% of Melt for new Ingot). 28 14

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 29 � Realm of the “Engine Guys” � UTAS – Goodrich � Pratt & Whitney � Rolls Royce � GE � CFM � ITP � IHI � KHI � MHI � High Barriers to Entry… � Deep Desire for Firm Pricing to Year 2030 30 15

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 � Very few Major North American Producers – ATI, Special Metals, Carpenter. � Pricing HIGHLY dependent on the prevailing ‘Trading’ price of Alloy Elements: � Nickel Alloy � Chrome � Molybdenum � Natural Gas / Energy Component � Difficult to predict, and difficult to hedge pricing. � All traded on the LME and other exchanges. � RMS = Raw Material Surcharge 31 32 16

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 33 34 17

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 � Market is EXTREMELY TIGHT! � Producing Mills are routinely 4-8 weeks late � They are all “horrible”… And they don’t care about you! � They don’t care that they are Horrible… They have been that way for almost 20 years. � (Old technology) X (Union workforce) = Disaster!! (It’s a Sellers Market) � Consolidation of the Aerospace Alloy Mills = “BORG”! Resistance is Futile… We will Assimilate you! 35 36 18

The Aerospace & Defense Forum South Bay Chapter April 8, 2015 � Aircraft Alloy – LTA’s don’t mean much.. P.O.’s are a little better. Best to buy ahead and expect “Lateness not Greatness”… � Aluminum Plate – don’t get caught short. LTA’s are worthwhile if you live up to your agreement. � Titanium – Aerospace Grades have extended lead-times due to processing. Availability is not an Issue. � Nickel Sheet – Your supplier should be lowering your transactional price. Best Suppliers will ‘Dollar average’ and lower existing contract pricing. Bottom is close… � Aluminum Extrusion – Life is Good! No Worries unless buying Large Press items. 37 38 19

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries