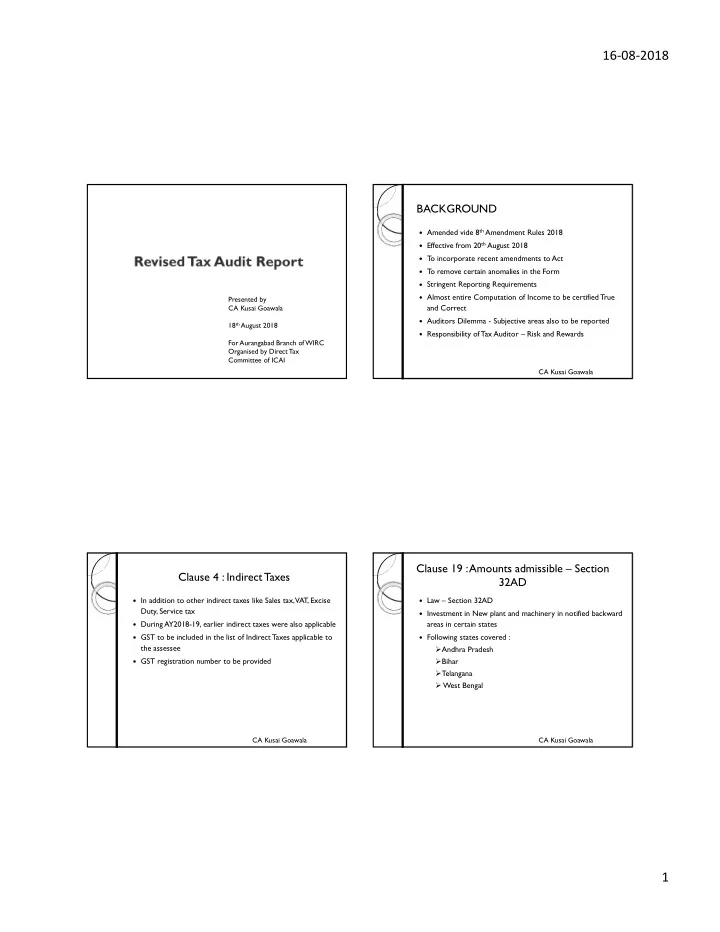

16-08-2018 BACKGROUND Amended vide 8 th Amendment Rules 2018 Effective from 20 th August 2018 To incorporate recent amendments to Act To remove certain anomalies in the Form Stringent Reporting Requirements Almost entire Computation of Income to be certified True Presented by and Correct CA Kusai Goawala Auditors Dilemma - Subjective areas also to be reported 18 th August 2018 Responsibility of Tax Auditor – Risk and Rewards For Aurangabad Branch of WIRC Organised by Direct Tax Committee of ICAI CA Kusai Goawala Clause 19 : Amounts admissible – Section Clause 4 : Indirect Taxes 32AD In addition to other indirect taxes like Sales tax, VAT, Excise Law – Section 32AD Duty, Service tax Investment in New plant and machinery in notified backward During AY2018-19, earlier indirect taxes were also applicable areas in certain states GST to be included in the list of Indirect Taxes applicable to Following states covered : the assessee Andhra Pradesh GST registration number to be provided Bihar Telangana West Bengal CA Kusai Goawala CA Kusai Goawala 1

16-08-2018 Clause 19 – Amount admissible – Section 32AD Investment after 1.4.2015 but before 1.4.2020 To report under Tax Audit 15% of cost of new asset allowed as deduction Amount Debited to Profit and Loss (all costs incurred on acquisition of new asset are not debited Condition – cannot sell within 5 years from date of to Profit & Loss A/c except depreciation) acquisition except under mergers and acquisitions. Amount admissible Whether all conditions fulfilled CA Kusai Goawala CA Kusai Goawala Clause 24-Deemed profits u/s 32AD Clause 26 – Section 43B If the new asset in respect of which deduction u/s 32AD Clause (g) added claimed Any sum payable to Indian Railways for the use of Railway Assets Sold within 5 years, deduction allowed will be deemed Scope of Section 43B expanded. income Payments to railways for use of Railway assets like lease rentals, etc allowable on payment basis Cross check of later non compliances leading to income The scope of 43B initially started with Statutory payments expanded to contractual payments CA Kusai Goawala CA Kusai Goawala 2

16-08-2018 Clause 29A – Forfeiture of advance received Whether any amount is to be included as income chargeable This clause was inserted in AY 2015-16 – however, has been under the head “Income from Other Sources” as referred to brought in tax audit report now. in clause (ix) of Section 56(2) Earlier the forfeited amount was deducted from cost of The clause refers to income on forfeiture of advance in asset. course of negotiations for transfer of asset. Tax was deferred now preponed Amount forfeited and If applicable, report: Negotiations do not result in transfer Nature of Income ◦ The above conditions to be complied for the forfeiture to Amount be added as income. CA Kusai Goawala CA Kusai Goawala Clause 29B – Section 56(2)(x) – Tax on Understanding Law – Section 56(2)(x) Deemed Gift Sections 56(2)(vii) and (viia) substituted. Any amount by any person from any person – All entities covered as recipient or givers Scope of earlier section expanded considerably a) Amount of money in excess of Rs.50000 in aggregate – All entities covered – earlier AOP, BOI were not covered without adequate consideration- Gift taxable Earlier some entities were covered for some of the assets b) Immoveable property Widely held companies and shares of widely held companies Without consideration were not covered With inadequate consideration If applicable, report: Difference greater than 50000 Nature of Income 5% difference between Stamp Duty Value and Amount Market Value permitted. If above 5% entire difference taxable CA Kusai Goawala CA Kusai Goawala 3

16-08-2018 Exemptions Moveable Property c) ◦ Property Defined Shares and Securities Any sum of money/property received – Jewellery 1. From any relatives Archaeological Collection 2. On the occasion of marriage of an individual Drawings 3. Under a will or by way of inheritance Paintings Sculptures 4. Contemplation of death of the payer or donor Work of Art 5. From any Local Authority Bullion 6. From any fund or foundation or university or educational ◦ Without Consideration institution or a hospital or medical institution or any ◦ With Inadequate Consideration trust or institution referred to in clause (23C) of ◦ Difference greater than 50000 section10. CA Kusai Goawala CA Kusai Goawala Transfers not considered From or by any trust or institution u/s 12A or 12AA Total or partial partition of a HUF 7) By any fund or foundation or university or educational Gift or will or an irrevocable trust 8) institution or a hospital or medical institution referred to in A company to its subsidiary sub clause(iv)/(v)/(vi)/(via) of clause (23C) of section 10 A subsidiary to its holding By way of transaction not regarded as transfer under 9) Amalgamation clause(i)/(iv)/(v)/(vi)/(via)/(viaa)/(vib)/(vic)/(vica)/(vicb)/(vid)/( Demerger vii) of section 47. Business reorganization 10) From an Individual by a trust created solely for benefit of Agricultural land in India, etc. relative CA Kusai Goawala CA Kusai Goawala 4

16-08-2018 Clause 30A – International Transaction – RELATIVES Associated Enterprises In relation to an individual, means the- Whether any primary adjustment made under 92CE(1) ? ◦ Husband If Yes ◦ Wife Whether excess amount repatriated to India within time ◦ Brother or Sister of an individual/spouse limit (90days) ◦ Brother or Sister of either parents If no – whether imputed interest – Amount as per rule10CB ◦ Any lineal ascendant or descendant of individual/spouse a) Denominated in Indian currency- lending rate of SBI as ◦ Spouse of relatives mentioned above on 1 st day of april of PY + 325 basis points. b) Denominated in foreign currency – 6 months LIBOR as on 30 th september of PY + 300 basis points. Poser- Alimony received on a monthly basis from ex-husband by a person as per Divorce Decree- taxable? CA Kusai Goawala CA Kusai Goawala Law relating to Section 92CE(1): -Transfer Pricing The assessee who undertakes International Transaction with As per Scheme – 92CC e) Associated Enterprises. The above is binding on Department as well as Assessee – If it makes primary adjustment in the transfer price – for five years following options. Unless law changes or facts changes a) Suomoto by the Assessee Safe Harbour Rules – 92CB e) b) By AO and accepted by the assessee (determination of arm’s length price u/s 92C or 92CA c) Determined by an Advanced Pricing Agreement – Section Apply Rule 10TD –Various percentages of income and 92CC conditions in respect of various types of income) d) Board makes Advance Price Agreement – Arms length Result of resolution of an assessment by mutual agreement e) Price procedure under DTAA. CA Kusai Goawala CA Kusai Goawala 5

16-08-2018 Clause 30B – Expenditure by way of Interest or any similar nature If applicable, report: Associated Enterprises to Non Resident Enterprise a) Expenditure of Interest b) EBIDTA By way of Interest or any similar nature paid by Assessee c) Interest > 30% of EBIDTA (Not applicable to Banking Company) d) Interest expense brought forward from earlier years e) Interest expense carried forward to subsequent years. Exceeding 30% of EBIDTA Excess to be disallowed and carried for 8 Assessment Years. CA Kusai Goawala CA Kusai Goawala Clause 30C – GAAR – Impermissible Law on GAAR – Section 95 to 98 Transactions – Section 96 Section 95 – An arrangement may be declared as If applicable, report: impermissible (section 96) and consequences (section 98) in Nature relation to tax arising may be determined. Amount of the tax benefit aggregate to all the parties in Section 96 – Impermissible Transactions the transaction a) Create rights obligations – not ordinarily created – arms length b) Directly/Indirectly misuse or abuse of any provisions of the Act c) Lacks Commercial Substance (section 97) d) Which are not ordinarily employed for the bonafide purposes. CA Kusai Goawala CA Kusai Goawala 6

16-08-2018 Section 97 – Lacks commercial substance Section 98 – Consequences a) Inconsistent with/differs substantially with steps a) Disregarding ,combining or recharacterising any step b) Involves round tripping/disguises value/location/source or b) Treating arrangement as non existing ownership c) Disregarding any accommodating party c) Location of an asset/place of residence/transaction – with d) Deeming persons as one person substantial commercial substance. e) Reallocating receipt or expenditure d) No significant business risk or impact on cash flow f) Treating place of residence except tax benefits. g) Looking through h) Equity may be treated as debt i) Capital items may be considered as revenue CA Kusai Goawala CA Kusai Goawala Exemptions Clause 31 – Section 269ST The transactions having tax benefit up to 3 crore not Receipts/Payments of Rs.2 lakh or more. covered. From a person : Transactions with FII not covered. a) In a day b) In a single transaction c) Transactions relating to one event d) Any amounts received by an assessee or paid by an assessee to any person. CA Kusai Goawala CA Kusai Goawala 7

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries