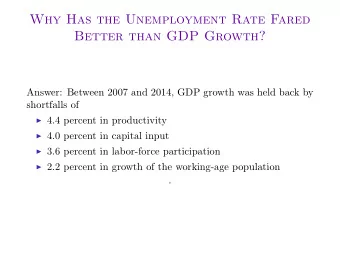

Comments on Bob Hall “Why Has the Unemployment Rate Fared Better than GDP Growth?” John Fernald October 14, 2016 My thanks to FRBSF colleagues for helpful conversations in recent years about the issues in this discussion. But the views expressed here are my own and do not necessarily reflect the views of the Federal Reserve Bank of San Francisco or the Federal Reserve System

Unemployment rate is where it was in 2007 …but output growth has disappointed Business-sector output growth Average annualized growth rate Percent Paper 4.5 • Uses Okun’s Law to control 4 for the cycle 3.5 • Growth-accounting for non- 3 cyclical output shortfall: 2.5 – Labor (LFPR, working-age 2 population) – TFP 1.5 – Capital 1 0.5 0 1947-73 1973-95 1995-04 2004-07 2007-16 Source: Fernald (2014a), BEA, BLS. Quarterly; samples end in Q4 of years shown except 1973 (end Q1) and 2016 (ends Q2). Output averages income and expend.

My take: Slow growth from demographics and productivity— not Great-Recession Business-sector output growth Average annualized growth rate Percent 4.5 4 • Okun’s Law was normal (with 3.5 low potential) 3 • Demographics and 2.5 productivity are slow 2 • Best guess: slow growth the new reality 1.5 1 0.5 0 1947-73 1973-95 1995-04 2004-07 2007-16 Source: Fernald (2014a), BEA, BLS. Quarterly; samples end in Q4 of years shown except 1973 (end Q1) and 2016 (ends Q2). Output averages income and expend.

My take: Slow growth from demographics and productivity— not Great-Recession Business-sector output growth Average annualized growth rate Percent 4.5 4 • Okun’s Law was normal (with 3.5 low potential) 3 • Demographics and 2.5 Hours productivity are slow 2 • Best guess: slow growth the new reality 1.5 Labor 1 Prod. 0.5 0 1947-73 1973-95 1995-04 2004-07 2007-16 Source: Fernald (2014a), BEA, BLS. Quarterly; samples end in Q4 of years shown except 1973 (end Q1) and 2016 (ends Q2). Output averages income and expend.

Okun’s Law consistent with low potential

Hall, p.2: “U.S. Experience since the crisis is a major deviation from [Okun’s] Law” (From Daly, Fernald, Jorda, and Nechio, 2013)

Hall, p.2: “U.S. Experience since the crisis is a major deviation from [Okun’s] Law” (From Daly, Fernald, Jorda, and Nechio, 2013)

Okun like previous recessions…but with low potential growth (From Daly, Fernald, Jorda, and Nechio, 2013)

Okun like previous recessions…but with low potential growth (From Daly, Fernald, Jorda, and Nechio, 2013)

Okun like previous recessions…but with low potential growth (From Daly, Fernald, Jorda, and Nechio, 2013)

Okun like previous recessions…but with low potential growth (From Daly, Fernald, Jorda, and Nechio, 2013)

Okun “loops” come from TFP

Okun “loops” come from TFP 13

Why has potential growth been so slow since 2007?

Has cyclical become structural? Maybe for hours… 975 1985 1995 2 975 1985 1995 ource: BLS

Has cyclical become structural? Maybe for hours… 975 1985 1995 2 975 1985 1995 ource: BLS

Has cyclical become structural? Maybe for hours… 975 1985 1995 2 975 1985 1995 ource: BLS

Has cyclical become structural? Maybe for hours… • Oulton and Sebastia-Barriel (2013) – For advanced economies, financial crises do not permanently affect level of TFP or labor productivity – Employment per capita is permanently lower • Huang, Luo, and Startz (2015) – TFP level recovers rapidly after all U.S. recessions – Hours worked no longer recovers (L-shaped) • But U.S. employment growth would have slowed anyway – Krueger (2016), Gagnon, Johannsen, and Lopez-Salido (2016)

Slowing labor-force growth not (just) the Great Recession 3.5 3.0 2.5 2.0 1.5 1.0 labor force 0.5 0.0 -0.5 950 1960 1970 1980 1990 2000 2010 2020 2030

TFP has been consistent (and slow) Contributions to growth in U.S. output per hour Business sector, percent change, annual rate Percent 3.5 3 2.5 2 1.5 1 0.5 0 -0.5 1947-73 1973-95 1995-04 2004-07 '07-10 '10-16 Source: Fernald (2014a). Quarterly; samples end in Q4 of years shown except 1973 (end Q1) and 2016 (end Q2). Capital deepening is contribution of capital relative to quality-adjusted hours. Total factor productivity measured as a residual.

TFP has been consistent (and slow) Contributions to growth in U.S. output per hour Business sector, percent change, annual rate Percent 3.5 Labor quality 3 Capital deepening 2.5 2 TFP 1.5 1 0.5 0 -0.5 1947-73 1973-95 1995-04 2004-07 '07-10 '10-16 Source: Fernald (2014a). Quarterly; samples end in Q4 of years shown except 1973 (end Q1) and 2016 (end Q2). Capital deepening is contribution of capital relative to quality-adjusted hours. Total factor productivity measured as a residual.

Capital: Unwinding of dynamics of Great Recession 110 105 100 Pre-Crisis Projection 95 90 85 80 970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Low growth is the new normal

Demographics: Low growth the new normal • Demographics: Slow hours growth – Gagnon et al (2016): 1-1/4 percent slowdown since 1980 • If GDP per hour like 1973-95: GDP growth around 1¾ % • Likely optimistic: Plateau in educational attainment means less growth in labor quality (Goldin-Katz, 2009; Jorgenson) – Bosler, Daly, Fernald, Hobijn (2016): Around ¼ pp less growth from that source, implying GDP growth around 1½ %

Takeaway: Was the Great Recovery really ‘Elusive’? • Paper finds that growth in recovery exceeded (slow) potential • Since 2007, TFP growth at its “typical” pace of past 40 years, plus demographics, can explain disappointing GDP growth • May have to accept the new reality

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries