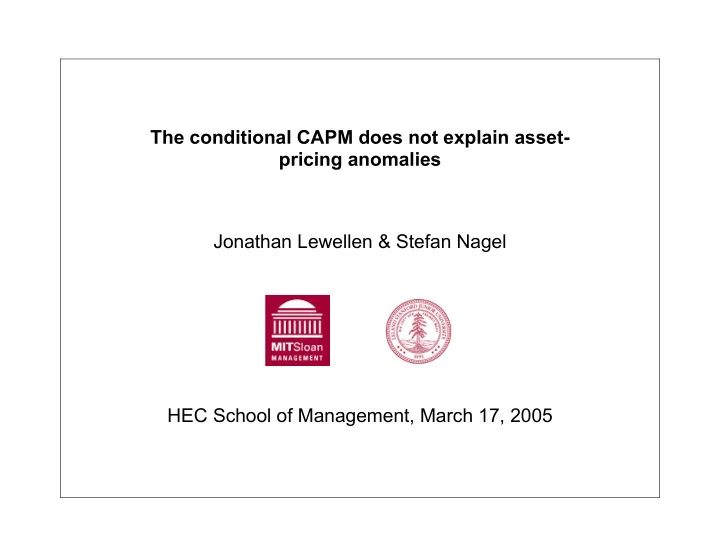

The conditional CAPM does not explain asset- pricing anomalies Jonathan Lewellen & Stefan Nagel HEC School of Management, March 17, 2005

Background Size, B/M, and momentum portfolios, 1964 – 2001 Monthly returns (%) Avg. returns CAPM alphas Portfolio Size B/M R -1,-6 Size B/M R -1,-6 0.17 Low 0.71 0.41 0.07 -0.20 -0.41 2 0.74 0.58 0.51 0.16 0.03 0.04 3 0.70 0.66 0.43 0.19 0.17 -0.01 4 0.69 0.80 0.52 0.21 0.35 0.08 High 0.50 0.88 0.79 0.11 0.39 0.29 Long–short 0.21 0.47 0.61 -0.03 0.59 0.70 t-stat 0.91 2.98 2.76 -0.16 4.01 3.14 2

Background Explained by the conditional CAPM w/ time-varying betas? Theory Jensen (1968) Dybvig and Ross (1985) Hansen and Richard (1987) Application to size, B/M, and momentum Zhang (2002) Jagannathan and Wang (1996) Lettau and Ludvigson (2001) Petkova and Zhang (2004) Lustig and Van Nieuwerburgh (2004) Santos and Veronesi (2004) Franzoni (2004), Adrian and Franzoni (2004) Wang (2003) 3

Rolling betas of value stocks, 1930 – 2000 Franzoni (2004) 4

Background Explained by the conditional CAPM w/ time-varying betas? Theory Jensen (1968) Dybvig and Ross (1985) Hansen and Richard (1987) Application to size, B/M, and momentum Zhang (2002) Jagannathan and Wang (1996) Lettau and Ludvigson (2001) Petkova and Zhang (2004) Lustig and Van Nieuwerburgh (2004) Santos and Veronesi (2004) Franzoni (2004), Adrian and Franzoni (2004) Wang (2003) 5

Background Conditional CAPM R it = α t + β t R Mt + ε t α t = 0 Empirical tests with constant β R it = α + β R Mt + ε t α ≠ 0 6

Intuition 1 Alternate between efficient portfolios A and B 1.40 1.20 B 1.00 Dynamic 0.80 strategy A .5 A + .5 B 0.60 0.40 0.20 0.00 2.0 3.0 4.0 5.0 6.0 7.0 8.0 9.0 7

Intuition 2 R t = β t R Mt + ε t , β t = β + η t , γ t = E t-1 [R Mt ], ρ β , γ > 0 0.12 E[R i | R M ] 0.10 0.08 0.06 0.04 0.02 R M 0.00 -0.08 -0.06 -0.04 -0.02 0.00 0.02 0.04 0.06 0.08 -0.02 -0.04 True -0.06 Uncond. regression -0.08 -0.10 8

Overview Perspective on conditional asset-pricing tests A simple empirical test 9

Overview Perspective on conditional asset-pricing tests A simple empirical test Time-variation in betas / expected returns is too small to explain anomalies 10

Theory Excess returns: R it , R Mt No restriction on joint distribution of returns Notation γ t = E t-1 [R Mt ], σ = var t-1 (R Mt ), β t = cov t-1 (R it , R Mt ) / σ 2 2 t t σ = var(R Mt ), β u = cov(R it , R Mt ) / γ = E[R Mt ], σ 2 2 M M β = E[ β t ] 11

Theory If conditional CAPM holds, what is α u ≡ E[R it ] – β u γ ? E t-1 [R it ] = β t γ t 12

Theory If conditional CAPM holds, what is α u ≡ E[R it ] – β u γ ? E t-1 [R it ] = β t γ t E[R it ] = β γ + cov( β t , γ t ) 13

Theory If conditional CAPM holds, what is α u ≡ E[R it ] – β u γ ? E t-1 [R it ] = β t γ t E[R it ] = β γ + cov( β t , γ t ) ⇒ α u = γ ( β – β u ) + cov( β t , γ t ) 14

Theory If conditional CAPM holds, what is α u ≡ E[R it ] – β u γ ? E t-1 [R it ] = β t γ t E[R it ] = β γ + cov( β t , γ t ) ⇒ α u = γ ( β – β u ) + cov( β t , γ t ) Conditional beta γ 1 1 β u = β + β γ + β γ − γ + β σ 2 2 cov( , ) cov[ , ( ) ] cov( , ) σ t t σ t t σ t t 2 2 2 M M M 15

Theory If conditional CAPM holds, what is α u ≡ E[R it ] – β u γ ? E t-1 [R it ] = β t γ t E[R it ] = β γ + cov( β t , γ t ) ⇒ α u = γ ( β – β u ) + cov( β t , γ t ) Conditional beta γ 1 1 β u = β + β γ + β γ − γ + β σ 2 2 cov( , ) cov[ , ( ) ] cov( , ) σ t t σ t t σ t t 2 2 2 M M M Convexity Cubic Volatility 16

Theory If conditional CAPM holds, what is α u ≡ E[R it ] – β u γ ? E t-1 [R it ] = β t γ t E[R it ] = β γ + cov( β t , γ t ) ⇒ α u = γ ( β – β u ) + cov( β t , γ t ) Conditional beta γ 1 1 β u = β + β γ + β γ − γ + β σ 2 2 cov( , ) cov[ , ( ) ] cov( , ) σ t t σ t t σ t t 2 2 2 M M M Conditional alpha γ γ γ 2 α u = − β γ − β γ − γ − β σ 2 2 1 cov( , ) cov[ , ( ) ] cov( , ) t t t t t t σ σ σ 2 2 2 M M M 17

Magnitude γ γ γ 2 α u = − β γ − β γ − γ − β σ 2 2 1 cov( , ) cov[ , ( ) ] cov( , ) t t t t t t σ σ σ 2 2 2 M M M 18

Magnitude γ γ γ 2 α u = − β γ − β γ − γ − β σ 2 2 1 cov( , ) cov[ , ( ) ] cov( , ) t t t t t t σ σ σ 2 2 2 M M M • γ 2 / σ ? 2 M γ 2 / 1964 – 2001: γ = 0.47%, σ M = 4.5% ⇒ σ = 0.011 2 M 19

Magnitude γ γ γ 2 α u = − β γ − β γ − γ − β σ 2 2 1 cov( , ) cov[ , ( ) ] cov( , ) t t t t t t σ σ σ 2 2 2 M M M • γ 2 / σ ? 2 M γ 2 / 1964 – 2001: γ = 0.47%, σ M = 4.5% ⇒ σ = 0.011 2 M • ( γ t – γ ) 2 ? Suppose γ ≈ 0.5% and 0.0% < γ t < 1.0%. Then ( γ t – γ ) 2 is at most 0.005 2 = 0.000025. 20

Magnitude γ γ γ 2 α u = − β γ − β γ − γ − β σ 2 2 1 cov( , ) cov[ , ( ) ] cov( , ) t t t t t t σ σ σ 2 2 2 M M M • γ 2 / σ ? 2 M γ 2 / 1964 – 2001: γ = 0.47%, σ M = 4.5% ⇒ σ = 0.011 2 M • ( γ t – γ ) 2 ? Suppose γ ≈ 0.5% and 0.0% < γ t < 1.0%. Then ( γ t – γ ) 2 is at most 0.005 2 = 0.000025. γ α u ≈ β γ − β σ 2 cov( , ) cov( , ) t t t t σ 2 M 21

1: Constant volatility α u ≈ cov( β t , γ t ) = ρ σ β σ γ ρ = 0.6 σ β ρ = 1.0 σ β 0.3 0.5 0.7 0.3 0.5 0.7 Monthly alpha (%) Monthly alpha (%) σ γ = 0.1 σ γ = 0.1 0.2 0.2 0.3 0.3 0.4 0.4 0.5 0.5 22

1: Constant volatility α u ≈ cov( β t , γ t ) = ρ σ β σ γ ρ = 0.6 σ β ρ = 1.0 σ β 0.3 0.5 0.7 0.3 0.5 0.7 Monthly alpha (%) Monthly alpha (%) σ γ = 0.1 σ γ = 0.1 0.2 0.2 0.3 0.3 0.4 0.4 0.5 0.5 Economically large Evidence later Fama and French (1992, 1997) 23

1: Constant volatility α u ≈ cov( β t , γ t ) = ρ σ β σ γ ρ = 0.6 σ β ρ = 1.0 σ β 0.3 0.5 0.7 0.3 0.5 0.7 Monthly alpha (%) Monthly alpha (%) σ γ = 0.1 σ γ = 0.1 0.2 0.2 0.3 0.3 0.4 0.4 0.5 0.5 Economically large Evidence from predictive regressions Campbell and Cochrane (1999) 24

1: Constant volatility α u ≈ cov( β t , γ t ) = ρ σ β σ γ ρ = 0.6 σ β ρ = 1.0 σ β 0.3 0.5 0.7 0.3 0.5 0.7 Monthly alpha (%) Monthly alpha (%) σ γ = 0.1 σ γ = 0.1 0.2 0.2 0.3 0.3 0.4 0.4 0.5 0.5 Arbitrary 25

1: Constant volatility α u ≈ cov( β t , γ t ) = ρ σ β σ γ ρ = 0.6 σ β ρ = 1.0 σ β 0.3 0.5 0.7 0.3 0.5 0.7 Monthly alpha (%) Monthly alpha (%) σ γ = 0.1 σ γ = 0.1 0.02 0.03 0.04 0.03 0.05 0.07 0.2 0.04 0.06 0.08 0.2 0.06 0.10 0.14 0.3 0.05 0.09 0.12 0.3 0.09 0.15 0.21 0.4 0.07 0.12 0.17 0.4 0.12 0.20 0.28 0.5 0.09 0.15 0.21 0.5 0.15 0.25 0.35 26

1: Constant volatility α u ≈ cov( β t , γ t ) = ρ σ β σ γ ρ = 0.6 σ β ρ = 1.0 σ β 0.3 0.5 0.7 0.3 0.5 0.7 Monthly alpha (%) Monthly alpha (%) σ γ = 0.1 σ γ = 0.1 0.02 0.03 0.04 0.03 0.05 0.07 0.2 0.04 0.06 0.08 0.2 0.06 0.10 0.14 0.3 0.05 0.09 0.12 0.3 0.09 0.15 0.21 0.4 0.07 0.12 0.17 0.4 0.12 0.20 0.28 0.5 0.09 0.15 0.21 0.5 0.15 0.25 0.35 B/M portfolio: 0.59% Momentum portfolio: 1.01% 27

1: Constant volatility β t ~ N[1.0, 0.7], γ t ~ N[0.5%, 0.5%], ρ = 1.0 0.10 E[R i | R M ] 0.08 0.06 0.04 0.02 R M 0.00 -0.08 -0.06 -0.04 -0.02 0.00 0.02 0.04 0.06 0.08 -0.02 -0.04 True -0.06 Uncond. regression -0.08 -0.10 28

2: Time-varying volatility γ α u ≈ β γ − β σ 2 cov( , ) cov( , ) t t σ t t 2 M Effects of time-varying γ t and σ offset (if they move together) 2 t 29

2: Time-varying volatility γ α u ≈ β γ − β σ 2 cov( , ) cov( , ) t t σ t t 2 M Effects of time-varying γ t and σ offset (if they move together) 2 t Merton (1980): γ t = λ σ 2 t σ 2 γ α ≈ β γ < cov( β t , γ t ) u cov( , ) σ t t 2 M 30

2: Time-varying volatility γ α u ≈ − β σ 2 = – γ ρ σ β σ v (where v t = σ / σ ) 2 2 cov( , ) t t M t σ 2 M ρ = 0.2 σ β ρ = 0.5 σ β 0.3 0.5 0.7 0.3 0.5 0.7 Alpha (%) Alpha (%) σ v = 1.0 σ v = 1.0 -0.03 -0.05 -0.07 -0.06 -0.10 -0.14 1.3 -0.04 -0.07 -0.09 1.3 -0.08 -0.13 -0.18 1.6 -0.05 -0.08 -0.11 1.6 -0.10 -0.16 -0.22 1.9 -0.06 -0.10 -0.13 1.9 -0.11 -0.19 -0.27 2.2 -0.07 -0.11 -0.15 2.2 -0.13 -0.22 -0.31 γ = 0.50 31

Testing the conditional CAPM Traditional tests R it = α it + β it R Mt + ε it β it = b i0 + b i1 Z 1,t-1 + b i2 Z 2,t-1 + … 32

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries