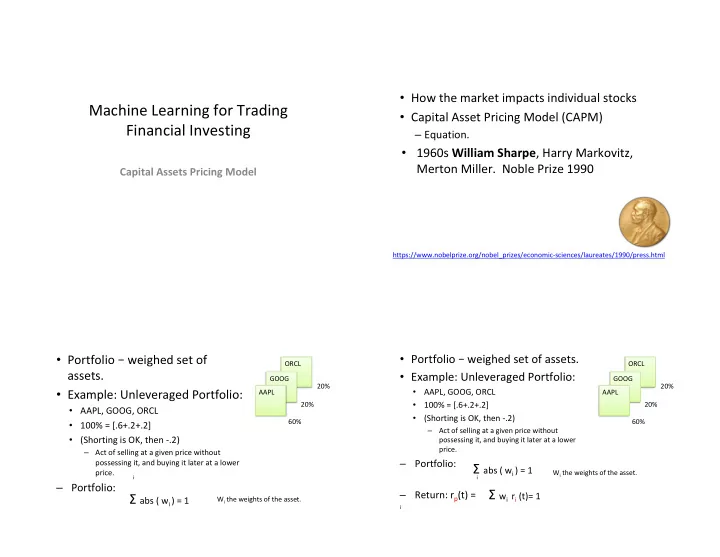

Capital Asset Pricing Model (CAPM) Machine Learning for Trading - PowerPoint PPT Presentation

How the market impacts individual stocks Capital Asset Pricing Model (CAPM) Machine Learning for Trading Financial Investing Equation. 1960s William Sharpe , Harry Markovitz, Merton Miller. Noble Prize 1990 Capital Assets

• How the market impacts individual stocks • Capital Asset Pricing Model (CAPM) Machine Learning for Trading Financial Investing – Equation. • 1960s William Sharpe , Harry Markovitz, Merton Miller. Noble Prize 1990 Capital Assets Pricing Model https://www.nobelprize.org/nobel_prizes/economic-sciences/laureates/1990/press.html • Portfolio – weighed set of • Portfolio – weighed set of assets. ORCL ORCL assets. • Example: Unleveraged Portfolio: GOOG GOOG 20% 20% • Example: Unleveraged Portfolio: • AAPL, GOOG, ORCL AAPL AAPL • 100% = [.6+.2+.2] 20% 20% • AAPL, GOOG, ORCL • (Shorting is OK, then -.2) 60% 60% • 100% = [.6+.2+.2] – Act of selling at a given price without • (Shorting is OK, then -.2) possessing it, and buying it later at a lower price. – Act of selling at a given price without possessing it, and buying it later at a lower – Portfolio: Σ abs ( w i ) = 1 price. W i the weights of the asset. i i – Portfolio: Σ w i r i (t)= 1 – Return: r p (t) = Σ abs ( w i ) = 1 W i the weights of the asset. i

Example Market Portfolio Sectors: Markets: • Stock A : 75% in portfolio +1% (up) • US : S&P 500 • Energy • Stock B: (-)25% in portfolio -2% (down) • UK: FTA • Technology • Return: • Japan: TOPIX Became + • Manufacturing • = .75 * 1 + -.25 (-2) = .75 + .50 = 1.25% . Indexes: Weighted. . Cap Weighted. . Market Cap – Capitalization number of shares available for the stock times its price. Outstanding shares -- stock currently held by all its shareholders/ Towards a CAPM • Weight of any particular stock • r i (t) = β r m (t) + α i (t) – Its market cap and divide it by the sum of the market caps of all the stocks. #shares * price / Σ ( market caps of all stock) • Some Stocks have large weighing's, e.g., Apple and Exons each have about 5% of the S&P 500 • Return of an individual stock on day t: – And strong effect of the market. – equals beta times the return on the market • Return = market + residual.

Alpha and Beta Alpha and Beta r i (t) = β r m (t) + α i (t) r i (t) = β r m (t) + α i (t) • Higher Alpha? [ ] [ ] • Higher Alpha? (Yint) [ ] [ ] • Higher Beta? [ ] [ ] • Higher Beta? (slope) [ ] [ ] Alpha and Beta Recap. r i (t) = β r m (t) + α i (t) • Beta reflects how risky an asset is compared to overall Beta: Baseline = 1 <1 - less volatile than market market =1 - move like the market – A function of the volatility of >1 – more volatile than market the asset and the market (as well as the correlation between the two). – A risk-reward measure (risk worth in return for the reward) • Higher Alpha? [ ] [ Y] • Alpha – measure of Alpha: Baseline = 0 (a %) performance compared to the <0 - underperforms. • Higher Beta [ ] [ Y] =0 - perform the same as market market. >0 – outperforms the market

What would sway you make a riskier Where would you invest? investment? • Idea: You want to be compensated for the Safely deposit in bank Risky Company added risk. • Fixed • Fixed – Want higher average percentage return. – 5% Interest – 5% Interest. • Question : What Average Percentage Return would compensates for the added risk? – What expected return of the investment is worth the added risk? Capital Asset Pricing Formula. Capital Asset Pricing Model - CAPM Capital Asset Pricing Model - CAPM Time Value of Money : Risk Free Rate - r f over a period of • Expected return of an a sset r a 1) time • General Idea: Compensation comes in 2: 2) Risk Incurred : Amount of compensation for taking additional risk. 1) Time Value of Money : Investment over time, and is typically represented by the Risk Free Rate - r f r a = r f + Risk Incurred over a period of time 2) Risk Incurred : Amount of compensation for Risk Incurred = β a * ( Risk Premium) taking additional risk. Risk Premium = r m - r f r a = Time Value + Risk Incurred r m = Expected Market Return r a = r f + Risk Incurred r f = risk free rate. r a = r f + β a ( r m - r f )

Going Back to Regression How does it relate? • r a (t) = β a r m (t) + α a (t) • Imagine many different stocks, many different α a (t), IS the residual - CAPM says betas, they may move in different directions. this is random with an expected value of 0 r a (t) = β a r m (t) + α a (t) • Lets assume the risk free rate is 0 (for now), in CAPM formula – Strategies: » Passive: Buy Index and HOLD r a (t) = β a r m (t) + α a (t) » Active: Pick Stocks (believe in alpha – note α a is market relative). • CAPM – significant return of an individual stock is due to the market. • Overweigh • Now also imagine that we have a portfolio – with many • Underweigh different betas. Possibly moving in different directions.. Active Portfolio Construction Q: Implications of CAPM • r p (t) = β p r m (t) + α p (t) larger β p smaller β p • r a (t) = β p r m (t) + Σ w a α a (t) • Upward market ������� • Downward market �������� • Similarly β p is weighted sum of the individual betas for each of the stocks. • If you have an upward market do you want a larger, or smaller β p? • If you have an downward market do you want a larger, or smaller β p

Implication of CAPM • r p (t) = β p r m (t) + α p (t) • Upward market want a larger beta because then we go up even further than the market. • Expected value of α p = 0 So greater good to have greater than 1. • Only way to beat market is to choose β p • Downward market – want smaller beta . • Choose high β p in upward market • Choose low β p in downward market – Example: if market goes down 1% and beta is less than 1, then our portfolio goes down less than the • Efficient Market Hypothesis (EMH) says you market, less than 1%. cannot predict the market • Can you? What do you think? Arbitrage Pricing Theory (ABT) CAPM and Hedge Funds. • Two Stock Scenario • 1976 Stephen Ross. – over 10 days. • Don’t use a single Beta. Use different Beta per – Assume Market is flat, did not move over time period sectors e.g., different betas for Finance, Tech. • A. Long $50.00 – Predict stock is going up 1% over market – Beta = 1.0 r a (t) = β a r m (t) + α a (t) • B. Short $50.00 – Predict stock is going down -1% below market. In flat market first term is 0: • Negative BET – Beta = 2.0

CAPM and Hedge Funds. CAPM and Hedge Funds. • Two Stock Scenario • Two Stock Scenario – over 10 days. – over 10 days. – Assume Market is flat, did – Assume Market goes up by not move over time period 10%. • A. Long $50.00 • A. Long $50.00 – Predict stock is going up 1% – Predict stock is going up 1% over market over market – Beta = 1.0 – Beta = 1.0 r a (t) = β a r m (t) + α a (t) r a (t) = β a r m (t) + α a (t) • B. Short $50.00 • B. Short $50.00 – Predict stock is going down – Predict stock is going down -1% below market. -1% below market. In flat market first term is 0: Answer % increase $ increase • Negative BET • Negative BET Ra – Beta = 2.0 – Beta = 2.0 For A our return is 0.01 *50 = .50 Rb For B our return is – 1* -1* 0.01 = .50 Total Total is 1.00 CAPM and Hedge Funds. CAPM and Hedge Funds. • Two Stock Scenario • Two Stock Scenario – over 10 days. – over 10 days. – Assume Market goes down by – Assume Market is flat, did 10% did not move over time not move over time period period • A. Long $50.00 • A. Long $50.00 – Predict stock is going up 1% – Predict stock is going up 1% over market over market – Beta = 1.0 – Beta = 1.0 r a (t) = β a r m (t) + α a (t) r a (t) = β a r m (t) + α a (t) • B. Short $50.00 • B. Short $50.00 – Predict stock is going down -1% – Predict stock is going down below market. -1% below market. In flat market first term is 0: In flat market first term is 0: • Negative BET • Negative BET – Beta = 2.0 – Beta = 2.0 For A our return is 0.01 *50 = .50 For A our return is 0.01 *50 = .50 For B our return is – 1* -1* 0.01 = .50 For B our return is – 1* -1* 0.01 = .50 Total is 1.00 Total is 1.00

• Board Examples

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.