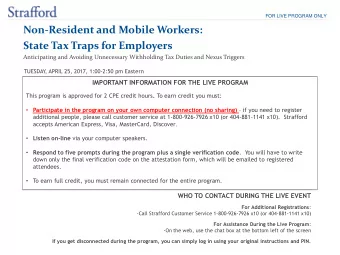

Presenting a live 110 ‐ minute teleconference with interactive Q&A Tax Traps Arising From Non ‐ Resident and Mobile Workers Anticipate and Avoid Unwarranted Withholding Tax Duties and Nexus Triggers THURSDAY, JUNE 2, 2011 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific Today’s faculty features: Mindy Harada Director Employment Tax Practice PricewaterhouseCoopers San Jose Calif Mindy Harada, Director, Employment Tax Practice, PricewaterhouseCoopers , San Jose, Calif. Chaim Kofinas, Senior Manager, WithumSmith+Brown , Red Bank, N.J. Hollis Hyans, Partner, Morrison & Foerster , New York For this program, attendees must listen to the audio over the telephone. Please refer to the instructions emailed to the registrant for the dial-in information. Attendees can still view the presentation slides online. If you have any questions, please contact Customer Service at1-800-926-7926 ext. 10 .

Conference Materials If you have not printed the conference materials for this program, please complete the following steps: Click on the + sign next to “Conference Materials” in the middle of the left- • hand column on your screen hand column on your screen. Click on the tab labeled “Handouts” that appears, and there you will see a • PDF of the slides for today's program. Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open. • Print the slides by clicking on the printer icon. •

Continuing Education Credits FOR LIVE EVENT ONLY Attendees must listen to the audio over the telephone . Attendees can still view the presentation slides online but there is no online audio for this program. Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10 . at 1 800 926 7926 ext. 10 .

Tips for Optimal Quality S S ound Qualit y d Q lit For this program, you must listen via the telephone by dialing 1-866-869-6667 and entering your PIN when prompted. There will be no sound over the web co connection. ect o . If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail sound@ straffordpub.com immediately so we can address the problem. Viewing Qualit y To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again press the F11 key again.

Tax Traps Arising From Non ‐ Resident T T A i i F N R id t and Mobile Workers Seminar June 2, 2011 Holly Hyans, Morrison & Foerster Chaim Kofinas, WithumSmith+Brown hhyans@ mofo.com ckofinas@ withum.com Mindy Harada, PricewaterhouseCoopers mindy.harada@ us.pwc.com

Today’s Program How Mobile Workers Can Trigger Tax Obligations Slide 3 – Slide 24 [Holly Hyans] Difficulties With Current State Laws, Regulations Slide 25 – Slide 43 [Chaim Kofinas] Administrative Challenges For Taxpayers Slide 44 – Slide 52 [Mindy Harada] Options To Consider In Addressing These Tax Issues Slide 53 – Slide 57 [Holly Hyans, Chaim Kofinas and Mindy Harada]

Holly Hyans, Morrison & Foerster HOW MOBILE WORKERS CAN HOW MOBILE WORKERS CAN TRIGGER TAX OBLIGATIONS

Introduction To This Section Introduction To This Section Legal Withholding (by employer for employee) Nexus (for the employer and the employee) Practical Filing obligations (for the employer and employee) Penalty issues (for the employer and employee) Need for a reliable tracking system g y Theoretical goals Nexus and withholding thresholds should be clear and uniform. Nexus thresholds should not be based on de minimis in-state visits or modest telecommuting by employees. The same employee-based nexus thresholds should apply to employers and employees. 8 This is MoFo.

Nexus And Telecommu ting Nexus And Telecommu ting Under basic nexus rules, telecommuting employees can create nexus for their employers. p y Under basis nexus rules, telecommuting employees can create nexus for themselves and be subject to personal income tax filing nexus for themselves and be subject to personal income tax filing requirements and liability. 9 This is MoFo.

Employee Withholding: Nexus Basics Nexus Basics Nexus basics - Individuals Nexus basics - Individuals A state has nexus over a resident and can subject all of a resident’s income to tax, regardless of where the income is earned earned. A state has nexus over a non-resident to the extent that such individual derives income from in-state activities. 10 This is MoFo.

Employee Withholding: Employer Nexus Employer Nexus Employer nexus Employer statutory nexus is generally statutorily triggered by “doing business” or “transacting business” in-state, maintaining an office, owning or leasing property, or having employees performing services for the employer in-state. The U.S. Constitution may limit the breadth of statutory nexus. The Commerce Clause of the U.S. Constitution may require y q that an in-state physical presence exist, although the applicability of the rule to corporate income tax has not been resolved. Quill Corp. v. North Dakota , 504 U.S. 298 (1992) KFC Corp. v. Iowa Dep’t of Revenue, 792 N.W.2d 308 (Iowa 2010), petition for cert. filed (U.S. Apr. 28, 2011) (No. ( ), p ( p , ) ( 10-1340) 11 This is MoFo.

Employee Withholding: Employer Nexus (Cont ) Employer Nexus (Cont.) Employer nexus Under basic nexus rules telecommuting employees can create Under basic nexus rules, telecommuting employees can create nexus for their employers. Employers will have an in-state physical presence (the employee at a minimum and perhaps also property and an employee, at a minimum, and perhaps also property and an office). 12 This is MoFo.

Employee Withholding: N Nexus Triggers T i Examples Hiring an employee to perform back office or software support services from his or her home, in a state other than that in which , the employer has offices Sending an employee into a state to meet with clients Allowing senior personnel to work from their homes and providing Allowing senior personnel to work from their homes and providing them with or reimbursing them for expenses related to work Allowing a long-term employee who needs to relocate for personal reasons to telecommute personal reasons to telecommute 13 This is MoFo.

Employee Withholding: Telecommuting Issues And Challenges Telecommuting Issues And Challenges Employers may not be aware that there are tax ramifications from Employers may not be aware that there are tax ramifications from telecommuting and may not have tracking systems in place. Even if an employer adopts a tracking system employees may not Even if an employer adopts a tracking system, employees may not report telecommuting completely or accurately. 14 This is MoFo.

Practical Impacts Of Withholding On Corporate Exposure g p p Tax costs of telecommuters to employers can be substantial and may include, in addition to “employer” taxes (withholding, unemployment insurance, workers’ compensation), corporate income and franchise taxes; and may impose on employers a sales tax collection responsibility. Implementation of tracking system may be costly. Employees may not comply with the tracking system to avoid Employees may not comply with the tracking system, to avoid potential personal income tax obligations. 15 This is MoFo.

Corporate Withholding Issue s Corporate Withholding Issue s Withholding thresholds vary from state to state. Visit thresholds E.g. , Connecticut and New York (14 days) Day count methodology may vary Income thresholds Fixed dollar Idaho ($1,000) Tied to personal exemption New Jersey, West Virginia Withholding for employees can lead to taxability inquiries. Some statutes explicitly provide that withholding standing alone is not a nexus-generating event. Withholding “does not in itself” create nexus for the withholding agent. N.C. Gen. Stat. § 105-163.4 16 This is MoFo.

Corporate Withholding Provisions g Sample withholding provisions Georgia: Georgia defines an employer as “any person for whom an individual who is a resident or domiciliary of this state performs or performed any service of whatever nature ... ” Ga. Code Ann. § 48 7 100(5) § 48-7-100(5) New Jersey: Every “employer maintaining an office or transacting business within this State and making payment of any wages subject to New Jersey personal income tax or making payment of subject to New Jersey personal income tax or making payment of any remuneration for employment subject to contribution under the New Jersey ‘unemployment compensation law’ ... to a resident or nonresident individual shall deduct and withhold from such wages ... ” N.J. Stat. Ann. § 54A:7-1(a) ” N J St t A § 54A 7 1( ) North Carolina: North Carolina requires an employer to withhold income tax from wages of all residents regardless of where earned N C Gen Stat § 105-163 1(4) earned. N.C. Gen. Stat. § 105 163.1(4) 17 This is MoFo.

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries