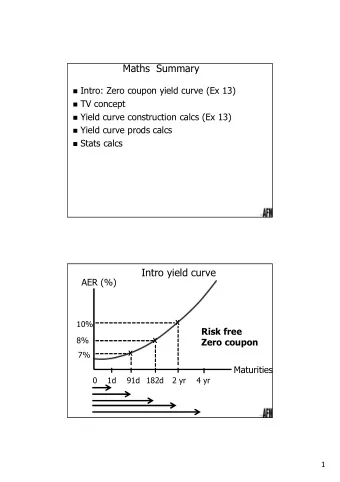

T HE R AMSEY RULE AND YIELD CURVE MODELING : ECONOMIC AND FINANCIAL - PowerPoint PPT Presentation

The economic framework The financial framework and progressive utilities Yield curve dynamics T HE R AMSEY RULE AND YIELD CURVE MODELING : ECONOMIC AND FINANCIAL VIEWPOINTS . Caroline HILLAIRET, Ensae, CREST Joint work with Nicole El Karoui and

The economic framework The financial framework and progressive utilities Yield curve dynamics T HE R AMSEY RULE AND YIELD CURVE MODELING : ECONOMIC AND FINANCIAL VIEWPOINTS . Caroline HILLAIRET, Ensae, CREST Joint work with Nicole El Karoui and Mohamed Mrad (Sorbonne Université, Université Paris XIII) With the support of "Chaire Risques Financiers" and ANR "Lolita" OICA Conference April 28th, 2020 1/ 33 Caroline HILLAIRET, Ensae, CREST Ramsey rule: economic and financial viewpoints

The economic framework The financial framework and progressive utilities Yield curve dynamics M OTIVATION Modeling accurately long term interest rates is a crucial challenge ◮ Embedded long term interest rate risk in longevity-linked securities (maturity up to 30 − 50 years.) ◮ financing of ecological projects ◮ valuation of any other investment with long term impact. ◮ Because of the lack of liquidity for long horizon, the standard financial point of view cannot be easily extended. Economic point of view ◮ Extensive literature on the economic aspects of long-term policy-making (Ekeland, Gollier, Weitzman...), ◮ Often motivated by ecological issues (Gollier, Hourcade & Lecocq) ◮ How to discount the far-distant future? (Gollier) ◮ Based on the equilibrium theory 2/ 33 Caroline HILLAIRET, Ensae, CREST Ramsey rule: economic and financial viewpoints

The economic framework The financial framework and progressive utilities Yield curve dynamics T HE UNDERLYING OPTIMIZATION PROBLEMS The following utility optimization program has to be solved in both financial and economic frames; usually formulated on a given horizon T H . � T H � � u ( T H , X π, c U ( t , x ) = ess sup T H ( t , x )) + v ( s , c s ) ds | X t = x , a . s . E (1) ( π, c ) ∈A t ◮ Link between optimal wealth and consumption process ( X ∗ t , c ∗ t ) and optimal discounted pricing kernel ( Y ∗ t ) of the dual problem, given by the first order relation U x ( t , X ∗ t ) = Y ∗ t = v c ( t , c ∗ − ˜ U y ( t , Y ∗ t ) = X ∗ v y ( t , Y ∗ t ) = c ∗ t , − ˜ t ) , t . ◮ Dual optimization program � T H � � � ˜ ˜ U ( t , y ) = ess inf u ( T H , Y T H ) + v ( s , Y s ) ds | Y t = y , a . s . (2) E Y t � ◮ dual conjugate utility ˜ u ( y ) = sup x > 0 u ( x ) − yx ) 3/ 33 Caroline HILLAIRET, Ensae, CREST Ramsey rule: economic and financial viewpoints

The economic framework The financial framework and progressive utilities Yield curve dynamics T HE UNDERLYING OPTIMIZATION PROBLEMS Financial and economic frameworks both rely on the same optimization problem, that determines the optimal discounted pricing kernel used to evaluate claims (and that is the cornerstone of the Ramsey rule) ◮ The financial point of view, based on No-Arbitrage assumption assets, bank account, time-horizon, and utility functions are given exogenously, the problem is to characterize the optimal (self-financing) wealth-consumption plan. ◮ At the economic equilibrium the optimal investment strategy π e is given (market clearing condition) the problem is to find (if they exist), two utility functions ( U , v ) and a consumption rate c e such that the pair ( π e , c e ) is optimal In general, the dynamics of the technology/risky asset as well as the short rate are endogenously determined 4/ 33 Caroline HILLAIRET, Ensae, CREST Ramsey rule: economic and financial viewpoints

The economic framework The economic equilibrium The financial framework and progressive utilities The Ramsey rule Yield curve dynamics O UTLINE 1 T HE ECONOMIC FRAMEWORK The economic equilibrium The Ramsey rule 2 T HE FINANCIAL FRAMEWORK AND PROGRESSIVE UTILITIES The financial market Pathwise Ramsey rule and financial interpretation 3 Y IELD CURVE DYNAMICS Yield curve dynamics and their volatilities Infinite maturity yield curve 5/ 33 Caroline HILLAIRET, Ensae, CREST Ramsey rule: economic and financial viewpoints

The economic framework The economic equilibrium The financial framework and progressive utilities The Ramsey rule Yield curve dynamics T HE EQUILIBRIUM SPOT RATE ◮ Usual setting of equilibrium Power utility functions Geometric Brownian motion for the risky security/technology � � dS t = S t µ t dt + σ t dW t with deterministic coefficient µ and σ t ( x ) = − ( µ t − r t ( x )) U x ( t , x ) ◮ optimal investment π ∗ together with the σ 2 t x U xx ( t , x ) supply-equals-demand condition for risky security π ∗ = 1 determines endogenously the risk free rate r ∗ t . t x U xx ( t , x ) r ∗ t ( x ) = r ( t , X ∗ with r ( t , x ) = µ t + σ 2 t ( x )) U x ( t , x ) . (3) ◮ link between the risk premium and relative risk aversion of the utility process U t ) = − σ t X ∗ t U xx ( t , X ∗ t ) η ( t , X ∗ = σ t R r A ( U )( t , X ∗ t ) . U x ( t , X ∗ t ) 6/ 33 Caroline HILLAIRET, Ensae, CREST Ramsey rule: economic and financial viewpoints

The economic framework The economic equilibrium The financial framework and progressive utilities The Ramsey rule Yield curve dynamics T HE EQUILIBRIUM : CONS Traditional approaches, based on the theory of general equilibrium, are not always flexible enough to apprehend the long-term and to adapt to the uncertain evolution of the economic or financial environment. ◮ Cons of the usual setting of equilibrium (power utilities, geometric Brownian motion for optimal discounted pricing kernel) the way that preferences of multiple agents aggregate is a difficult task, and it is unlikely that the aggregate utility could be modeled by a simple function : the heterogeneity of economic actors is often downplayed in concrete applications, that use a simplified version of the theory not flexible framework optimal processes/choices are linear w.r.t. their initial conditions : can induce an underestimation of extreme risks equilibrium rate r does not depend on the wealth of the economy 7/ 33 Caroline HILLAIRET, Ensae, CREST Ramsey rule: economic and financial viewpoints

The economic framework The economic equilibrium The financial framework and progressive utilities The Ramsey rule Yield curve dynamics T HE EQUILIBRIUM : P ROS ◮ Pros : of the usual setting of economic equilibrium For a complete Markovian market, it is the only frame compatible with the existence of an equilibrium (see recent work of El Karoui and Mrad): the pricing kernel is a geometric Brownian motion the utility process is a mixture of dynamic power utilities. the market risk premium is deterministic the equilibrium portfolio is a mixture of geometric Brownian motion the dependency of the rate on the time-horizon T H of the optimization problem is in fact artificial, since the utility is part of the processes that should be determined at equilibrium. the expression for the interest rate (3), together with the dynamics of the wealth process dX ∗ t = ( µ t X ∗ t − c ∗ t ) dt + X ∗ t σ t dW t → the equilibrium poses the problem in a natural forward formulation ◮ Our approach: adopt a forward formulation with stochastic utility: can incorporate the possibility of changes in agent preferences over time or the uncertain evolution of the economic or financial environment. generate more complex pricing kernel capture more phenomena, particularly with regard to aggregation of heterogeneous agents and extreme risks. 8/ 33 Caroline HILLAIRET, Ensae, CREST Ramsey rule: economic and financial viewpoints

The economic framework The economic equilibrium The financial framework and progressive utilities The Ramsey rule Yield curve dynamics R AMSEY RULE IN E CONOMICS A link between consumption rate and discount rate at the economic equilibrium ◮ compute today of a long term discount rate R 0 ( T ) . ◮ Based on "representative agent" (Ramsey, Gollier) ◮ Small perturbation around the economic equilibrium Data and parameters ◮ u utility function (concave, increasing) typically u ( t , c ) = e − β t c 1 − θ / ( 1 − θ ) ◮ θ = risk aversion coefficient ◮ β pure time preference parameter ◮ c aggregate consumption rate, typically geometric Brownian motion c T = c 0 exp(( g − 1 2 σ 2 ) T + σ W T ) with g consumption growth rate. � u ′ ( T , c T ) � R 0 ( T ) = − 1 Ramsey rule : T ln E . ( u ′ = marginal utility ) u ′ ( 0 , c 0 ) 9/ 33 Caroline HILLAIRET, Ensae, CREST Ramsey rule: economic and financial viewpoints

The economic framework The economic equilibrium The financial framework and progressive utilities The Ramsey rule Yield curve dynamics ◮ "Historical" Ramsey rule (Ramsey, 1928) : c T = c 0 exp( gT ) R 0 ( T ) = β + θ g , (4) β pure time preference parameter, θ risk aversion, g growth rate. ◮ No consensus among economists about the parameter values that should be considered Example : Stern review on climate change (2006), with θ = 1, g = 1 . 3 % , β = 0 . 1 % → R 0 ( T ) = 1 . 4 % . Or θ = 1 . 2, g = 2 % , β = 0 . 1 % → R 0 ( T ) = 2 . 5 % ◮ Economic rates are very sensitive to the rate of preference for the present β , which can be viewed as the intensity of an independent exponential random horizon ◮ If c T = c 0 exp(( g − 1 2 σ 2 ) T + σ W T ) the Ramsey rule still induces a flat curve R 0 ( T ) = β + θ g − 1 2 θ ( θ + 1 ) σ 2 . (5) 10/ 33 Caroline HILLAIRET, Ensae, CREST Ramsey rule: economic and financial viewpoints

Recommend

![TDR Assumptions for Pulsed Neutron Yield [/keV] Neutron Yield [/keV] 2500 2000 2000 2500](https://c.sambuz.com/892356/tdr-assumptions-for-pulsed-s.webp)

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.