Structuring Preferred Partnership Freezes in Estate Planning: - PowerPoint PPT Presentation

Presenting a live 90-minute webinar with interactive Q&A Structuring Preferred Partnership Freezes in Estate Planning: Navigating IRC Chapter 14 Valuation Rules WEDNESDAY, MARCH 30, 2016 1pm Eastern | 12pm Central | 11am Mountain

Presenting a live 90-minute webinar with interactive Q&A Structuring Preferred Partnership Freezes in Estate Planning: Navigating IRC Chapter 14 Valuation Rules WEDNESDAY, MARCH 30, 2016 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific Today’s faculty features: Stephen M. Breitstone, Partner, Meltzer Lippe Goldstein & Breitstone , Mineola, N.Y . David C. Jacobson, Counsel, Meltzer Lippe Goldstein & Breitstone , Mineola, N.Y . Edward Vergara, Partner, Kaye Scholer , New York The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10 . NOTE: If you are seeking CPE credit, you must listen via your computer — phone listening is no longer permitted.

Tips for Optimal Quality FOR LIVE EVENT ONLY Sound Quality If you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory, you may listen via the phone: dial 1-866-961-9091 and enter your PIN when prompted. Otherwise, please send us a chat or e-mail sound@straffordpub.com immediately so we can address the problem. If you dialed in and have any difficulties during the call, press *0 for assistance. NOTE: If you are seeking CPE credit, you must listen via your computer — phone listening is no longer permitted. Viewing Quality To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

Continuing Education Credits FOR LIVE EVENT ONLY In order for us to process your continuing education credit, you must confirm your participation in this webinar by completing and submitting the Attendance Affirmation/Evaluation after the webinar. A link to the Attendance Affirmation/Evaluation will be in the thank you email that you will receive immediately following the program. For CPE credits, attendees must participate until the end of the Q&A session and respond to five prompts during the program plus a single verification code. In addition, you must confirm your participation by completing and submitting an Attendance Affirmation/Evaluation after the webinar and include the final verification code on the Affirmation of Attendance portion of the form. For additional information about continuing education, call us at 1-800-926-7926 ext. 35.

Program Materials FOR LIVE EVENT ONLY If you have not printed the conference materials for this program, please complete the following steps: Click on the ^ symbol next to “Conference Materials” in the middle of the left - • hand column on your screen. • Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program. • Double click on the PDF and a separate page will open. Print the slides by clicking on the printer icon. •

Structuring Preferred Partnership Freezes in Estate Planning – Navigating IRC Chapter 14 Valuation Rules Presented by: Stephen M. Breitstone sbreitstone@meltzerlippe.com David C. Jacobson djacobson@meltzerlippe.com Edward A. Vergara edward.vergara@kayescholer.com

Presentation Overview • Understanding IRC 2701 provisions • Comparison of the freeze partnership to other techniques • Grantor Trust Risks • Use of preferred partnerships with various trusts • Structure of Preferred Partnerships 6

Understanding IRC 2701 Provisions 7

Understanding IRC 2701 Provisions IRC 2701 provides for special valuation rules in the context of family-controlled entities • Provisions intended to discourage the use of entity “design” to enhance wealth transfer between generations. • Failure to account for IRC 2701 provisions can result in unanticipated gift and estate tax consequences. • Can apply even when transaction not intended to achieve wealth transfer or save estate or gift taxes. 8

Understanding IRC 2701 Provisions Perceived Abuse Prior to IRC 2701 • Under general valuation principles, the gift/estate tax value of entity interests are determined under the “subtractive method.” Value of Transferred Interest = (Value of Entity – Value of Retained Interest) • In order to depress the gift/estate tax value of entity interests transferred to a younger generation, the gift/estate tax value of interests retained by senior-generation (typically preferred interests) were enhanced through the addition of certain discretionary rights ( e.g. , rights to non-cumulative dividends, redemption rights, conversion rights, etc.). • Discretionary rights increased gift/estate tax value of parent’s retained interest, and by extension reduced value of common interest transferred to younger generation, even though discretionary rights unlikely to be exercised in context of family-controlled entity. • IRC 2701 ignores such discretionary rights and assigns zero value to them in determining value of senior family interests under Subtraction Method. 9

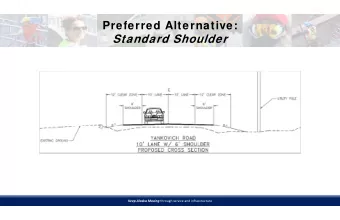

Perceived Abuse • Preferred interests provide for non-cumulative coupon, payable in the discretion of Board G1 Entity G2 Entity controlled by G2 Liquidation Non-cumulative rights Common • Preferred interests provide for Preferred Interest Interest powerful put rights an/or liquidation preference Family Company • Discretionary rights exercised to $10M benefit Common interests Pre-2701 Post-2701 Value of Company $10M Value of Company $10M Less: Value of Preferred $9.5M Less: “Zero valuation $0 (Artificially high) rule” Gift Value of Common $500k Gift Value of Common $10M 10

Understanding IRC 2701 Provisions • Perceived abuse addressed through “zero valuation rule”; Discretionary rights ignored in determining gift/estate tax value of preferred interests retained by senior generation • Narrow Exceptions to Zero Valuation Rule: • When senior generation’s preferred interest structured within certain parameters designed to ensure that retained rights are both mandatory and quantifiable. 11

Understanding IRC 2701 – Technical Provisions Application of § 2701- Overview • Generally, the zero valuation rule of IRC 2701 can cause a deemed gift to occur when there is a “Transfer” to a “Member of Transferor’s Family” of an interest in an entity controlled by “Applicable Family Members” • Transfer. Broadly defined and includes traditional transfer, capital contribution to new or existing entity, redemption, recapitalization or other change in capital structure of entity. • Applicable Family Member . Includes Transferor’s spouse, any ancestor of Transferor or his or her spouse, and spouse of any such ancestor. Attribution rules apply in measuring control. • Member of the Family . Includes Transferor’s spouse, any lineal descendant of Transferor or his or her spouse, and spouse of any such descendant. 12

Understanding IRC 2701 – Technical Provisions • Exception to Distribution Right – “Qualified Payment Right” • Any dividend payable on periodic basis (at least annually) under any cumulative preferred stock, to the extent such dividend is determined at fixed rate; • Any other cumulative distribution payable on periodic basis (at least annually) with respect to equity interest, to the extent determined at fixed rate or as fixed amount; or • Any Distribution Right for which election has been made to be treated as Qualified Payment. • Because Qualified Payments are mandatory, and no discretion of family controlled entity to make or withhold distributions exists, perceived opportunity to manipulate value does not exist; therefore, zero valuation rule will not apply. 13

Understanding IRC 2701 – Technical Provisions • “Lower Of” Rule for Valuing Qualified Payment Right Held in Conjunction with Extraordinary Payment Right • Example : Dad, the 100% stockholder of corporation, transfers common stock to Child and retains preferred stock which provides (1) Qualified Payment Right having value of $1,000,000 and (2) right to put all preferred stock to corporation at any time for $900,000 (Extraordinary Payment Right). • At time of transfer, corporation’s value is $1,500,000. • Under “Lower of” rule, value of Dad’s retained interest is $900,000, even though he retains Qualified Payment Right worth $1,000,000 • Retained interests are valued under assumption that Dad exercises Extraordinary Payment Right (put right) in manner resulting in lowest value being determined for all retained rights. • Result: Dad made gift of $600,000 ($1,500,000 - $900,000) rather than $500,000 (if value of preferred interest was based on the $1,000,000 value of Qualified Payment Right). 14

Understanding IRC 2701 – Technical Provisions • Minimum Value of Junior Equity Interest • If § 2701 applies, in the case of transfer of junior equity interest, such interest shall not be valued at amount less than 10% of sum of (1) total value of all equity interests, plus (2) total indebtedness of entity to Transferor or Applicable Family Member. 15

Understanding IRC 2701 • Rights that Are Not Extraordinary Payment Rights or Distribution Rights (i.e., rights that do not trigger application of § 2701): • Mandatory payment rights. • Liquidation participation rights. • Guaranteed payment rights. • Non-lapsing conversion rights. 16

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.