SLIDE 1 Some motivating facts

1 / 31

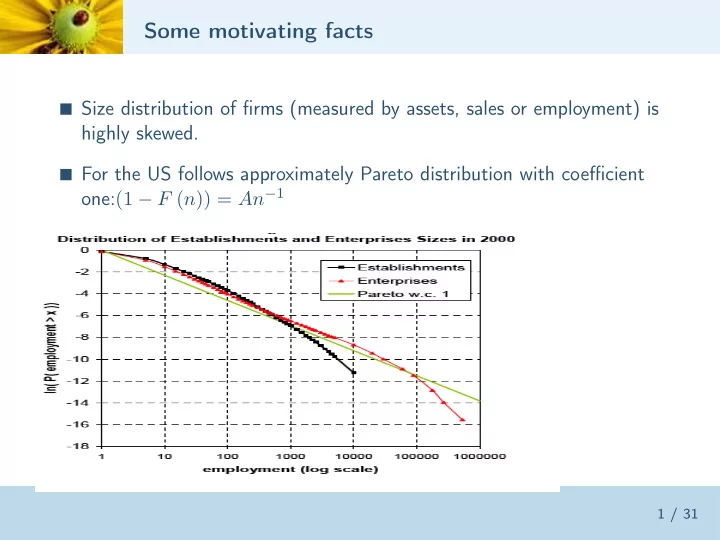

Size distribution of firms (measured by assets, sales or employment) is

highly skewed.

For the US follows approximately Pareto distribution with coefficient

SLIDE 2 more facts

2 / 31

Firm size is persistent but the variance of innovations is quite large. Gross realocation of employment across firms exceeds in several orders of

magnitude net reallocation.

Variance of growth rates declines with size and age. Firm size increases with age. There is considerable degree of entry/exit into narrowly defined

- industries. Small and young firms have higher exit rates.

Most firm level changes in employment correspond to idiosyncratic

shocks, i.e. not explained by aggregate, geographic or industry variables.

SLIDE 3 A simplified Lucas model

3 / 31

Collection of firms i = 1, ..., M Technology yi = einη

i where η < 1

Fixed endowment of labor N Competitive equilibrium {w, ni}maximizing profits and market clearing. n (ei, w) labor demand and n (ei, w) = N Solves planner problem:

maxni

i

SLIDE 4 Equilibrium

4 / 31

Employment:

ni = ae

1 1−η

i

a

1 1−η

i

= N yi = aηeie

η 1−η

i

= aηe

1 1−η

i

Remark yi/ni is the same for all firms! Solving for w and substituting:

y =

yi = aη e

1 1−η

i

=

1 1−η

i

1−η N η

SLIDE 5 The Aggregate Production function

5 / 31

y =

1 1−η

i

1−η N η =

1 1−η

i

1−η M1−ηN η

Cobb Douglass in M, N with TFP equal to geometric average of firm

shocks.

M is like a capital stock, sometimes called "organization capital" Intangible?

SLIDE 6 Multiple inputs

6 / 31

Results generalize to multiple inputs (Lucas 1978) Let f (x) be homogenous of degree one and

yi = ei (f (x))η

aggregate endowment vector X Aggregate production function:

y =

1 1−η

i

1−η M1−ηf (X)η

SLIDE 7 Large number of firms

7 / 31

Let F (e) denote the cdf for shocks. Suppose M is the mass of firms (quantity of organization capital)

y =

1 1−η

1−η M1−ηN η

Special case: F = 1 −

emin

e

α Pareto distribution Ee

1 1−η =

αemin α −

1 1−η

e

1 1−β −α

min

"Tail condition": defined only when α >

1 1−η

SLIDE 8 Endogenizing entry

8 / 31

Technology for creating firms (organization capital) takes ce workers. Entrants draw ei independently from same distribution Planner’s problem:

maxM,L

1 1−η

1−η M1−ηLη subject to : ceM + L ≤ N

solution: L = ηN and M = (1 − η) N/ce

y =

1 1−η

ce 1−η (1 − η)1−η ηη N

Constant returns to scale in aggregate Productivity negatively related to entry cost.

SLIDE 9 Connection to monopolistic competition

9 / 31

Dixit-Stiglitz (1977), Melitz (2003) Continuum of goods: y =

´ yη

i di

1

η

Linear techology yi = eη

i ni

Constant markup pi = 1

η (w/eη i )

yη

i ∝ e

1 1−η

i

and so is ni y =

1 1−η

i

1−η

η

M

1−η η N

yη =

1 1−η

i

1−η M1−ηN η

With endogenous entry get same M.

SLIDE 10

General or partial equilibrium

10 / 31

Partial equilibrium:

Aggregate demand D (p∗) Cost function c (e, q), supply function s (e, p) Entry cost ce Solve for unique p∗that makes expected profits = ce Find MEes (e, p∗) = D (p∗)

Correspondence (w = 1),

c (e, q) = f −1 (q/e) p∗ = 1/w∗

SLIDE 11

Firm dynamics - motivation

11 / 31

Lots of evidence that firms’ size is not constant

Five year AR1 of firm ln employment US manufacturing, persistence

0.92 and large variance of innovation.

Firm size distribution stochastically increases with age.

average entrant 35% size of average incumbent

SLIDE 12 Firm dynamics - simple model

12 / 31

entrants draw independently initial shocks from same distribution firm productivity evolves according to MP F (et+1|et) Repeated application generates probability distributions ˜

µs for firms of age s.

exogenous death/exit rate 1 − δ.

Mt = δtm0 + δt−1m1 + ... + δmt−1 + mt µt = M −1

t

µ0 + δmt−1˜ µ1 + ... + δtm0˜ µt

= ˆ e

1 1−η dµt (e)

1−η M1−η

t

Lη

t

SLIDE 13 Competitive equilibrium

13 / 31

Given sequence of wages w = {wt}∞

t=0

vt (e; w) = maxnenη − wtn + βδEvt+1

t

= E0vt (e; w) − wtce Definition 1. A competitive equilibrium is a sequence {mt, nt (e) , vt} and wages {wt} that satisfy the following conditions:

- 1. Employment decisions are optimal given wages

- 2. value functions are as defined above

- 3. ve

t ≤ 0 and mtve t = 0

´ nt (e) µt (de) = N.

SLIDE 14

Planners problem

14 / 31

Objective:

maxmt,Lt ∞

t=0βt ´

e

1 1−η dµt (e)

1−η M1−η

t

Lη

t

subject to : Mt = δtm0 + δt−1m1 + ... + mt L + cemt = N

Unique solution:

Objective strictly concave Constraints linear

SLIDE 15 Stationary equilibrium

15 / 31

Analogous to steady state (or balanced growth path) Entry flow mt = m for all t. This implies M =

m 1−δ and µ = (1 − δ) ∞ s=0 δs˜

µs

Value function:

v (e) = maxnenη − wn + βδ ˆ v

F

´ n (e, w) dµ (e) + mce = N

Stationary equilibrium is unique. Steady state productivity proportional to:

1 1−η

ce

1−η

SLIDE 16 Costs of entry and TFP

16 / 31

Cross-country regression (Moscoso-Boedo and Mukoyama, 2010) Calculate regulatory costs of creating business measured in units of

annual labor κ

Lowest US κ = 0.3, highest Liberia κ = 616.8, 29 countries with κ < 1

and 31 with κ > 10.

7 6 5 4 3 2 1 1 2 1 1 2 3 4 5 6 Log (GNI p cap relative to US) log() Entry Cost

SLIDE 17 Effects of entry costs in the model

17 / 31

From our previous derivations:

y =

1 1−η

ce + κ 1−η (1 − η)1−η ηη N d ln y/d ln (c + κ) = − (1 − η)

Effects of distortions to entry costs depend on the degree of decreasing

returns

usually take η = 0.85, so d ln y/d ln κ = −0.15 Back of the envelope (Moscoso-Boedo and Mukoyama)

baseline ce = 36. Compare κ = 10 and κ = 100 to κ = 0 κ = 10 → TFP = 0.9, κ = 100 → TFP = 0.6

Sizeable but far from observed differences in TFP.

SLIDE 18

Firm dynamics

18 / 31

Stylized facts:

Small firms grow faster (conditional on survival) Size of firms very persistent (close to random walk) Large firms have lower variance of growth rates Size distribution of firms stochastically increasing in age Exit rates decline with age

Last one cannot be explained in this model that assumes a constant exit

rate

Others depend on assumptions on the distribution F and the initial

distribution of firms shocks, call it G.

SLIDE 19

Age-increasing size distribution

19 / 31

Assumption 1. (FOSD) F (e, e) decreasing in e.

Sequence ˜

µs obtained recursively as ˜ µs+1 ([0, e]) = ´ F ([0, e], e) d˜ µs(e) Assumption 2. F ◦G G (F increases G): ´ F ([0, e], e) dG (e) < G ([0, e])

Persistence and F ◦ G G implies ˜

µs is increasing sequence (in FOSD)

SLIDE 20 Endogenous exit and selection

20 / 31

Firm exit endogenous Need a reason for exiting: fixed costs, opportunity costs Assume fixed cost f denominated in units of labor

v (e; w) = max

ˆ v

- e; w

- F

- de, e

- Decision rules n (e, w) and exit set E (w) .

Proposition 1. (i)v (e; w) strictly decreasing in w if nonzero. (ii)Under (FOSD) v (e; w) strictly increasing in e if nonzero and exit set is threshold e (w) .

Value of entry: ve (w) =

´ v (e; w) dG (e) − ce

SLIDE 21

The invariant measure of firms

21 / 31

Timing: 1) entry; 2) shocks realized, 3) exit; 4) production Entrants: m mass: measure mG Incumbents (before exit): µI (−∞, e) =

´ F (e, e0) µ (de0)

New measure of firms (e ≥ e∗)

Tµ (−∞, e) = m [G (e) − G (e∗)] + µI (e∗, e) = m [G (e) − G (e∗)] + ˆ [F (e, e0) − F (e∗, e0)] µ (de0)

Invariant measure: µ = Tµ

SLIDE 22 Unique invariant measure

22 / 31

Invariant measure as a weighted sum of measure of different cohorts. Let αn be the probability of surviving up to n periods

µ = m

∞

αn˜ µn

Necessary and Sufficient conditoin for existence :

∞

αn < ∞

Integrating by parts: finite expected lifetime

∞

αn =

∞

n (αn+1 − αn) < ∞

SLIDE 23 Stationary equilibrium: definition

23 / 31

{µ, e∗, m, w}

- 1. ve (w) ≤ 0 and ve (w) m = 0

- 2. e∗ is optimal exit rule

- 3. N =

´ (f + n (e, w)) dµ + mce

- 4. µ is an invariant measure

Equilibrium with entry and exit

m > 0 m (1 − G (e∗)) =

´ F (e∗, e) µ (ds)

ve (w∗) = 0 unique

SLIDE 24

Partial equilibrium

24 / 31

Inverse demand p = D (Q) Firms profit and supply function: π (e, p) and q (e, p), strictly increasing

in e and p

Cost of entry ce (fixed costs already included in π (e, p) function) Unique stationary equilibrium {µ, e∗, m, p}

SLIDE 25

Some properties

25 / 31

Size and Age

In the data size distribution stochastically incerases with age In model, depends on properties of F and G Sufficient condtitions:

F (e2, e) 1 − F (e1, e) decreasing in s for all (e, e1) F increases G

Firm growth: depends on properties of F

SLIDE 26

Rate of turnover

26 / 31

Rate of turnover (entry/exit)

m µ (E) = m λ ∞

n=0 αn˜

µn = 1/E (n)

E (n) decreases with e∗ (turnover increases) e∗ increases with w (decreases with p) Higher cost of entry ce, decrease w(increase p), decreases turnover

SLIDE 27 Turnover and Sunk Costs

27 / 31

Indirect measures of sunk costs

Average size of firms Number of firms

Cross industry regression. Dependent: Rate of Entry

Variable Estimate t Intercept

Log Avg Size

Log Num Firms 0.14 12.6

SLIDE 28 Selection and Productivity

28 / 31

Productivity determined by stochastic process (G, F) and exit threshold

Formulas for homogeneous case y =

1 1−η

1−η M1−ηLη L = N − mce − Mf M = m

αn (e∗) Ee

1 1−η =

´

e∗ e

1 1−η dµ

M

Selection effect: Ee

1 1−η increases with threshold e∗so decreases with ce.

Other effects (possibly M decreases), but total productivity must

decrease in ce.

SLIDE 29

Selection and productivity: analysis

29 / 31

No scale effects: Increasing N does not change e∗ and just increases

proportionally m and M.

Aggregate productivity shocks neutral

Changes wage proportionally Does not change employment, exit or entry decisions. Just scales up total output

Aggregate productivity shock that is complementary to e

Increases relative size of larger (higher e) firms Increases exit threshold e∗ (selection effect)

SLIDE 30 Identifying stochastic process

30 / 31

Hopenhayn and Rogerson (JPE 1993) Production function: f (s, n) = snα Let p denote output price (labor as numeraire) ln st+1 = ρ ln st + εt+1, where εt ∼ N

ε, σ2

ε

- First order conditions for employment:ln αp + ln st = (1 − α) ln nt

implies: ln nt+1 = (1 − α)−1 ln st+1 + ln αp = (1 − α)−1 (ρ ln st + εt+1) + ln αp = (1 − α)−1 {(1 − α) ρ ln nt + ρ ln αp + εt+1} + ln αp = A + ρ ln nt + (1 − α)−1 εt+1

ρ and σ identified from AR1 parameters for ln firm size

SLIDE 31

more calibration

31 / 31

The initial distribution determined by distribution of entrants sizes more parameters to determine: cf, ce and the mean ¯

ε.

Data to use: rate of turnover, mean size, age distribution.