SBA SOP 50-10-5(J) Critical Changes Presented by: Gary Griffin - PowerPoint PPT Presentation

CTAGGL SBA SOP 50-10-5(J) Critical Changes Presented by: Gary Griffin Chief Executive Officer Capital Growth Solutions, LLC Pertinent References/Docs Join NAGGL!!!! SBA Notice Control #: 5000-17008 (10/2017) SBA Notice Control #:

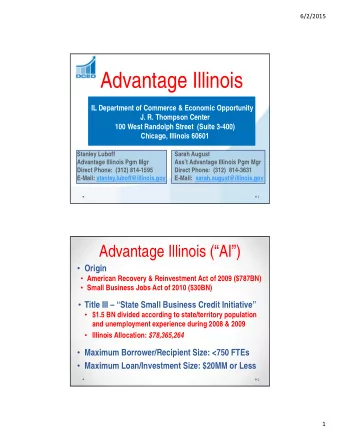

CTAGGL SBA SOP 50-10-5(J) Critical Changes Presented by: Gary Griffin Chief Executive Officer Capital Growth Solutions, LLC

Pertinent References/Docs • Join NAGGL!!!! • SBA Notice Control #: 5000-17008 (10/2017) • SBA Notice Control #: 5000-17009 (10/2017) • SBA Notice Control #: 5000-17029 (12/2017) • Just print the current version on the SBA Website and read it!

Hot Buttons for “Regular” Lenders • SBA is making the PLP designation “almost” essential to effectively process credit in a timely manner. More apparent every SOP. • 3 week minimum turnaround right now. • Stamp Actions MINIMUM of 2 weeks (and there are ALWAYS stamp actions) • Working Capital is a killer! In the initial memo go into DETAIL; no matter how little the request (in loan in excess of $350K). • Do NOT expect SBA to AUTOMATICALLY allow the reallocation of “excess” proceeds to WC. • Credit elsewhere, RMA and chicken farms!

Must do’s (in my opinion) • Dedicated SBA person to follow and interpret the SOP (BOTH SOP’s) • Join NAGGL and PARTICIPATE in training. • Consider SBA guidelines the MINIMUM you must do to protect the guaranty. • Site visits and pictures!!! • External review?

Document!!! Lots of changes, but as always, your best defense (if PLP), and best opportunity to avoid screen-outs (regular processing), is to provide all required documentation. For PLP, it is maintaining docs in file, and for “regular” if is providing all supporting docs the FIRST time!

Regular • PRIOR to submitting the loan, MUST inform Borrower/Principals in writing that they MAY be referred to CAIVRS in the event of default/loss to the government which could impact them negatively upon applying for any future government assisted financial aide. • PRIOR to submission, MUST inform Borrower that they do NOT have to employ Lender/Agent of Lender to assist in the preparation of SBA documentation (packaging fee).

PLP 1) CAIVRS 2) Fee disclosure 3) Docs required to be kept in file 1) Pgs. 215-217 - too long to go over here. I would put together a checklist for each PLP loan application addressing ALL items in BOLD and have that as a cover sheet in each application. 4) RMA

LSP’s A Lender must have a continuing ability to evaluate, process, close, service, liquidate and litigate small business loans (13 CFR § 120.410). A Lender may contract with a third party (Lender Service Provider (LSP)) to assist the Lender with one or more of these functions. However, the Lender itself, not the LSP, must be able to demonstrate that it exercises day-to-day responsibility for evaluating, processing, closing, disbursing, servicing, liquidating and litigating its SBA portfolio. SBA determines whether or not an Agent is an LSP on a loan-by-loan basis. If an Agent meets the definition of an LSP, a formal agreement between the Agent and Lender is required and must be reviewed by SBA. (See Paragraph X.D. for further guidance on LSP agreements.)

Franchise • SIMPLE: MUST be on the franchise directory • Guidance as to where to send them is in the SOP. Jury still out on how long the process takes! I believe it is the attorneys at the Franchisor which delay the process; not SBA. • Assume everyone is a “franchise” unless not even closely related! • Multiple Agreements • All must be eligible.

Drum Roll Please!

“Minimum” Equity • 10% of TOTAL project costs (this INCLUDES purchase price if BizAc, closing costs, guaranty fee, working capital, all PP&E) • Start-up or BizAc. • Owner carryback; FULL standby. • 50% rule/interpretation of “minimum equity”. • Partner buy-out.

Credit Elsewhere • New and Improved! (just kidding; this is nuts!) • Not your Father’s SBA anymore… • Identify non-government sources • Personal Resources (drill down to 10%) • About the only thing I am sure of is call features and balloons as part of policy/market.

Other ideas… ALWAYS have multiple reasons: 1) Balloon and call features. 2) Collateral. 3) DSC (term) necessary to meet cash flow coverage (Lender Policy). 4) Start-ups and projection deals (Lender Policy). 5) LAST is loan size and loan limit to a particular customer (and NEVER alone).

Collateral • Adequacy of collateral has really ALWAYS been there. PLEASE use the “new” discount factors in SBA’s recommendations to determine “fully collateralized”. NOTE: New personal residence rule over short -term assets. • Texas is lucky (for lots of reasons!) • Let’s discuss “Liquid” collateral.

Management Agreements • Basic common sense • Who signs the checks and makes the day-to-day decisions • BEWARE affiliation. If management agreement gives “too much” authority to operator, may bring in affiliation and size standard issues.

912’s • You, the LENDER, are expected to clear 912 issues if they are: 1) minor in nature (misdemeanor) 2) and distant in past. 3) Felonies still must be submitted. • 2 issues: 1) MUST still document the same way as before (Addendum B, court records, letter from principal and letter from Lender) 2) Citrus Heights seems to not have gotten the memo….

Chicken Farms (Ag based loans supposedly) Rumors???? Reality is SBA has taken a dislike to “feed lot” projects and “growers”. 1) Environmental studies as to waste dispersal 2) “Excess” land 3) Term 20/15 period!

Other • Express LOC Maturity: 5/5 rule (loan MUST amortize half way through maturity cycle). • Occupancy: Applicant gets benefit of common area. • 504 “Green” capped at $16.5M. • If you don’t like something go to • SOP50-10modernization@sba.gov • Subject line “7(a) – SOP 50 10 5(J) 7(a) comments.

Thank You!!! Capital Growth Solutions, LLC Gary Griffin, CEO Chuck Evans, President 423-475-5700 (W) 423-593-0976 (C) ggriffin@capgs.com cevans@capgs.com www.capgs.com

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.