Riding the - PDF document

S. Scholtes 30/10/2003 Judge Institute of Management University of Cambridge Riding the waves of change: Simulating Risky Investments S. Scholtes Judge

S. Scholtes 30/10/2003 Judge Institute of Management University of Cambridge ������������������� ��������� Riding the waves of change: Simulating Risky Investments S. Scholtes Judge Institute of Management �������������� ��������������������������� Speaker: Karl Rose (Strategic Intelligence, Shell) Topic: Managing in Darkness Time: Thursday 30 October 4.30 pm Venue: LT2 1

S. Scholtes 30/10/2003 Judge Institute of Management University of Cambridge ��������� Danny and I will prepare a mock exam before the weekend. We will let you know by email ����������������� ���������� �������� 2

S. Scholtes 30/10/2003 Judge Institute of Management University of Cambridge ����������������� ���������� �������� ����������� �������� � ������� � ��������� � ���� ����������������� ���������� �������� ������������ ����������� �������� �������� � �������������������� � ������� � �������������������������� � ��������� � ������ ������ � ���� � ���� 3

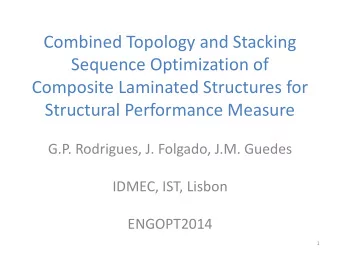

S. Scholtes 30/10/2003 Judge Institute of Management University of Cambridge ����������������� Projection based techniques are ���������� too simplistic in �������� their treatment of risk ������������ ����������� �������� �������� � �������������������� � ������� � �������������������������� � ��������� � ������ ������ � ���� � ���� ������������������������������� Cumulated project value Time 4

S. Scholtes 30/10/2003 Judge Institute of Management University of Cambridge ������������������������������� Cumulated project value Strategic phase: Are we doing the right thing? Time ������������������������������� Cumulated project value Strategic phase: Are we doing the right thing? Time Opportunity gains - ideas matter - period cash flows increase 5

S. Scholtes 30/10/2003 Judge Institute of Management University of Cambridge ������������������������������� Cumulated project value Operational phase: Strategic phase: Are we doing Are we doing things right? the right thing? Time Opportunity gains - ideas matter - period cash flows increase ������������������������������� Cumulated project value Operational phase: Strategic phase: Are we doing Are we doing things right? the right thing? Time Opportunity gains Efficiency gains - fighting the cost battle - ideas matter - period cash flows increase - cash flows positive but decreasing 6

S. Scholtes 30/10/2003 Judge Institute of Management University of Cambridge ������������������������������� Cumulated project value Operational phase: Strategic phase: Are we doing Are we doing things right? the right thing? Uncertainty Time Opportunity gains Efficiency gains - fighting the cost battle - ideas matter - period cash flows increase - cash flows positive but decreasing �������������� • Power plant investment – Fuel price, electricity price, demand, regulation…??? • Bidding for resources (e.g. 3G bandwidth) – Production capacity, market price, market demand, competition, political issues?? • R&D – Technical success, market demand, regulation, … • New product launch – Demand-price curve, competition, production quality, brand,… 7

S. Scholtes 30/10/2003 Judge Institute of Management University of Cambridge �!����"����������������� “Are you sure that we got the forecasts right?” “You can never be 100% sure with forecasts but I am fairly confident that the forecast is right.” #�����������������$����$���� 12 1982 US DEO oil price forecasts 0 Trend predicted 10 1981 0 Dollars per Barrel 80 1984 1983 60 1985 1986 1987 40 Actual 1991 20 1995 0 1975 1980 1985 1990 1995 2000 2005 Year Source: U.S. Department of Energy, 1998 8

S. Scholtes 30/10/2003 Judge Institute of Management University of Cambridge #�����������������$����$���� • In the early 1980's McKinsey were hired by AT&T to forecast the growth in the mobile phone market until the end of the millennium. • They projected a world market of 900,000. • Today, 900,000 handsets are sold every three days �!������������� • Lesson: The forecast is always wrong • But: such projections are part of every NPV analysis • Ergo: NPV analyses are always wrong • Obvious fact that needs to be recognized: – After the fact, the NPV of a project is well defined if the realised cash flows have been recorded – Before the fact, i.e. NOW, the cash flows are uncertain and hence the NPV itself is an uncertain quantity 9

S. Scholtes 30/10/2003 Judge Institute of Management University of Cambridge %�$������ �!������$���������������& • NPV is expected NPV – Beware the flaw of averages • Adjust discount rate for risky projects Discount rate = time value of money + risk premium • BUT: Conceptually difficult to mingle time value of money with risk premium in one figure – If risk premium is applied to costs (negative cash flow) then the expected cost is reduced rather than increased – Global risk adjustment (at cash flow level) versus local risk adjustment (at level of input uncertainties - to account for different risk profiles of different inputs) ������������ '�������������������"��������������� • Traditional NPV analysis Inputs: Projections Output: of uncertain NPV projection values • Risk-enhanced NPV analysis (Monte Carlo simulation) Inputs: Output: Shapes Shape of NPV of uncertain values 10

S. Scholtes 30/10/2003 Judge Institute of Management University of Cambridge (������������������& • Discount rates reflect – Macro-economic trend: Time value of money • “risk-free” rate, e.g. long-term government bonds – Debt risk: Bankruptcy • corporate bond spread - difference between corporate and government bond rate – Equity risk: Uncertain cash flows • risk-adjusted discount rates, CAPM-betas • Avoid double-counting for risk! – Sensible to discount at the corporate debt rate since MCS takes risk of cash flow fluctuation into account – Can estimate the distribution of the equity premium of the project by simulating NPV at debt rate / investment #������$������������ • The flaw of averages: NPV based on average inputs is NOT the average NPV • Flaw of averages lurks everywhere, where numbers are used to replace uncertain quantities! 11

S. Scholtes 30/10/2003 Judge Institute of Management University of Cambridge #������$������������ • Example: Depreciation over an uncertain lifetime (Savage 2002) • If a piece of equipment lasts N years, then the linear depreciation rate is 1/N per year • Suppose a piece of equipment is equally likely to last 2,3,4,…,10 years – Average lifetime: 6 years – Flaw of averages: Average depreciation rate is 1/6=16.7%? #������$������������ Lifetime Depreciation rate 2 50% 3 33% 4 25% 5 20% 6 17% 7 14% 8 13% 9 11% 10 10% Average 6 21% 12

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.