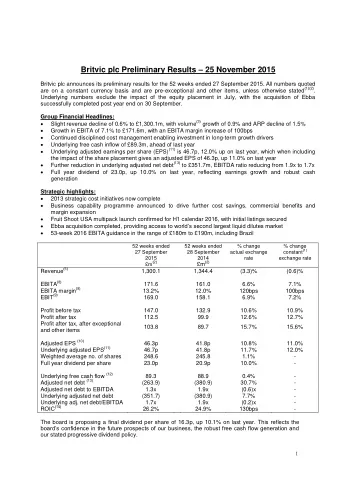

Preliminary Results 2015 Delivering Our Strategy Working together - PowerPoint PPT Presentation

The most important thing we build is trust ADVANCED ELECTRONIC SOLUTIONS AVIATION SERVICES COMMUNICATIONS AND CONNECTIVITY MISSION SYSTEMS Preliminary Results 2015 Delivering Our Strategy Working together to be a leading Global Technology and

The most important thing we build is trust ADVANCED ELECTRONIC SOLUTIONS AVIATION SERVICES COMMUNICATIONS AND CONNECTIVITY MISSION SYSTEMS Preliminary Results 2015 Delivering Our Strategy Working together to be a leading Global Technology and Services innovator, respected for providing solutions to the most challenging problems

Agenda Introduction Bob Murphy • Chief Executive Officer Financial Results Simon Nicholls • Chief Financial Officer Business Review Bob Murphy • Q&A • 1 3 March 2016 Cobham plc Cobham plc

Agenda Introduction Bob Murphy • Chief Executive Officer Financial Results Simon Nicholls • Chief Financial Officer Business Review Bob Murphy • Q&A • 2 3 March 2016 Cobham plc Cobham plc

Financial Highlights Aeroflex Drives Robust Performance Year to Year to Change Constant FX 31/12/15 31/12/14 Change £m £m Order Intake 2,148.0 1,908.3 12.6% 12.5% Revenue 2,072.0 1,851.7 11.9% 11.1% Trading Profit 332.2 286.7 15.9% 15.8% Trading Margin 16.0% 15.5% 0.5pts Underlying Profit before Taxation 280.4 257.0 9.1% 10.7% Underlying Earnings Per Share 19.5p 18.5p 5.4% 6.9% Operating Cash Conversion 70.7% 72.6% (1.9)pts Net Debt (1,206.8) (1,222.7) Dividend per Share 11.18p 10.65p 5.0% See Appendix for definitions, including underlying, used throughout this presentation. 3 3 March 2016 Cobham plc Cobham plc

Communications & Connectivity (CCC) Aeroflex Contribution Partially Offset by Weak Commercial Markets US Defence & Security 2015 2014 Change (2014: 15%) () (constant FX) % 15% Revenue £m 771.8 687.1 12.3% Non-US Defence 19% Trading Profit £m 108.4 113.4 (4.4)% 66% & Security (2014: 20%) Trading Margin 14.0% 16.5% (2.5)pts Commercial (2014: 65%) • Total revenue 12% higher: - Aeroflex test business contributed full year impact of £127m - Overall 4% organic revenue decline - 9% decline in commercial revenue, due to weakness in marine and land markets, partially offset by strong growth in commercial aerospace - Good defence/security organic growth of 5%, driven in particular by Avionics upgrades • Trading profit down £5m and lower trading margin of 14.0% reflects: - Aeroflex contribution including integration benefits - Significant impact of reduction in shorter cycle commercial volumes Note: US$ revenue 37%, EUR & DKK revenue 36% 4 3 March 2016 Cobham plc Cobham plc

Mission Systems (CMS) Strong AAR Execution Drives Results Commercial (2014: 7%) 2015 2014 Change () (constant FX) % 6% Revenue £m 382.4 348.7 9.7% 35% Trading Profit £m 68.0 38.6 76.2% US Defence 59% & Security Trading Margin 17.8% 11.1% 6.7pts (2014: 54%) Non-US Defence & Security (2014: 39%) • Total revenue increased by £34m with 10% organic growth driven by: - Strong production volumes and favourable mix across a variety of AAR programmes - Higher engineering and development revenue on US KC-46 tanker programme - Strong revenue and order flow from actuation products on air-to-ground munitions • Trading profit and margin significantly higher driven by: - Increase in revenue - Non-repeat of 2014 £15m aerial refuelling provision Note: US$ revenue 74% 5 3 March 2016 Cobham plc Cobham plc

Advanced Electronic Solutions (CAES) Aeroflex Drives Improvement Commercial 2015 2014 Change (2014: 11%) () (constant FX) % 17% Revenue £m 538.0 441.9 21.7% Non-US 7% Defence & Security Trading Profit £m 80.5 68.4 17.7% (2014: 4%) 76% Trading Margin 15.0% 15.5% (0.5)pts US Defence & Security (2014: 85%) • Total revenue increase of £96m: - Full year impact of Aeroflex, partially offset by divestments completed in the year - Organic revenue 7% lower with good growth from microelectronics for missiles, EW and radar, offset by mature production programmes ending • Trading profit higher, with margin slightly lower: - Contribution from Aeroflex, partially offset by adverse revenue mix in existing business - Integration efficiencies from site closures and supply chain Note: US$ revenue 99% 6 3 March 2016 Cobham plc Cobham plc

Aviation Services (CAvS) Strong Performance in Difficult Commercial Markets 0% 2015 2014 Change Commercial () (constant FX) % (2014: 46%) Revenue £m 390.1 387.4 0.7% 44% Trading Profit £m 57.3 52.0 10.2% 56% Trading Margin 14.7% 13.4% 1.3pts Non-US Defence & Security (2014: 54%) • Modest organic revenue increase driven by: - Growth in defence/security revenue; Special Mission and Helicopters both contribute - Commercial revenue slightly lower with reduced flying in the natural resources sector • Total trading profit increased £5m due to improved revenue mix and contract execution Note: AU$ revenue 56% 7 3 March 2016 Cobham plc Cobham plc

Revenue and Profit Sector Summary at Constant Exchange 1 Revenue Trading Profit Year to Year to Year to Year to £m Change Change 31/12/15 31/12/14 31/12/15 31/12/14 Cobham Communications and Connectivity 771.8 687.1 12.3% 108.4 113.4 (4.4%) Margin 14.0% 16.5% Cobham Mission Systems 382.4 348.7 9.7% 68.0 38.6 76.2% Margin 17.8% 11.1% Cobham Advanced Electronic Solutions 538.0 441.9 21.7% 80.5 68.4 17.7% Margin 15.0% 15.5% Cobham Aviation Services 390.1 387.4 0.7% 57.3 52.0 10.2% Margin 14.7% 13.4% Head Office and Eliminations (10.3) (0.9) 18.0 14.4 Exchange - (12.5) - (0.1) Cobham Group - as reported 2,072.0 1,851.7 11.9% 332.2 286.7 15.9% Margin 16.0% 15.5% (1) = 2014 data presented at 2015 exchange rates. 8 3 March 2016 Cobham plc Cobham plc

Reconciliation of Trading to Reported Profit Year to Year to 31/12/15 31/12/14 £m £m Trading profit 332.2 286.7 Underlying net finance costs (51.8) (29.7) Underlying profit before taxation 280.4 257.0 Taxation charge on underlying profit (2015: 21.5%; 2014: 20.25%) (60.2) (52.0) Underlying profit after taxation for the period 220.2 205.0 Business restructuring (67.5) (52.2) Movements in non-hedge accounted derivative financial instruments (18.8) (21.8) Amortisation of intangible assets arising on business combinations (176.8) (113.6) Impairment of Goodwill (26.6) - Exceptional legal costs - (0.8) Other business acquisition and divestment related items (30.5) (40.7) Non-underlying finance costs - (3.6) Taxation on non-underlying items 62.3 56.7 (Loss) / profit after taxation for the year (37.7) 29.0 9 3 March 2016 Cobham plc Cobham plc

Free Cash Flow FCF Includes Investment in Development Programmes, CAPEX, Aeroflex Integration £m 450 56.8 400 332.2 350 48.9 300 250 98.7 200 150 80.9 105.5 100 55.0 50 0 Slight Reduction in Net Debt to £1.21B – Net Debt:EBITDA of 2.9x Note: Depreciation and amortisation shown net of profit/loss on sale of property, plant and equipment and excluding amortisation of acquired intangibles. 10 3 March 2016 Cobham plc Cobham plc

Working Capital Bridge £m 500 10.9 41.9 378.3 400 359.3 53.0 36.8 4.0 13.0 300 33.0 Net operating cash outflow of £48.9m 200 100 0 11 3 March 2016 Cobham plc Cobham plc

Balance Sheet 31/12/2015 31/12/2014 restated £m £m Intangible assets 1,729.5 2,040.8 Property, plant and equipment 379.9 390.0 Other non-current assets 102.6 88.8 Non Current Assets 2,212.0 2,519.6 Inventories 410.4 429.5 Trade and other receivables < 1 year 366.0 435.3 Trade and other payables < 1 year (398.1) (505.5) Current Working Capital 378.3 359.3 Net current tax liabilities (116.5) (118.8) Net debt (1,206.8) (1,222.7) Provisions (142.5) (127.0) Retirement benefit obligations (56.7) (102.0) Other assets / liabilities (158.1) (196.1) Net Assets 909.7 1,112.3 12 3 March 2016 Cobham plc Cobham plc

Summary • Robust performance in 2015 in challenging market conditions • Absolute increases driven by the impact of Aeroflex; organic revenue decline of 1% • Group Trading Margin 16% includes: • Benefit of excellent progress with Aeroflex integration • Further traction in continuous improvement activities and cost reduction measures • Cash flow performance includes: • Increase in working capital on development programmes and short cycle demand impact • Business restructuring costs related to Connectivity strategy execution • Recommended increase in final dividend of 5% • Increased Free Cash Flow generation remains a major priority for 2016 • Focus on Net debt reduction • Group remains well funded on a long term basis 13 3 March 2016 Cobham plc Cobham plc

Agenda Introduction Bob Murphy • Chief Executive Officer Financial Results Simon Nicholls • Chief Financial Officer Business Review Bob Murphy • Q&A • 14 3 March 2016 Cobham plc Cobham plc

Today’s Agenda • Our Markets • Delivering Our Strategy • Summary 15 3 March 2016 Cobham plc Cobham plc

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.