More and more firms just calculate numbers. We help calculate your - PDF document

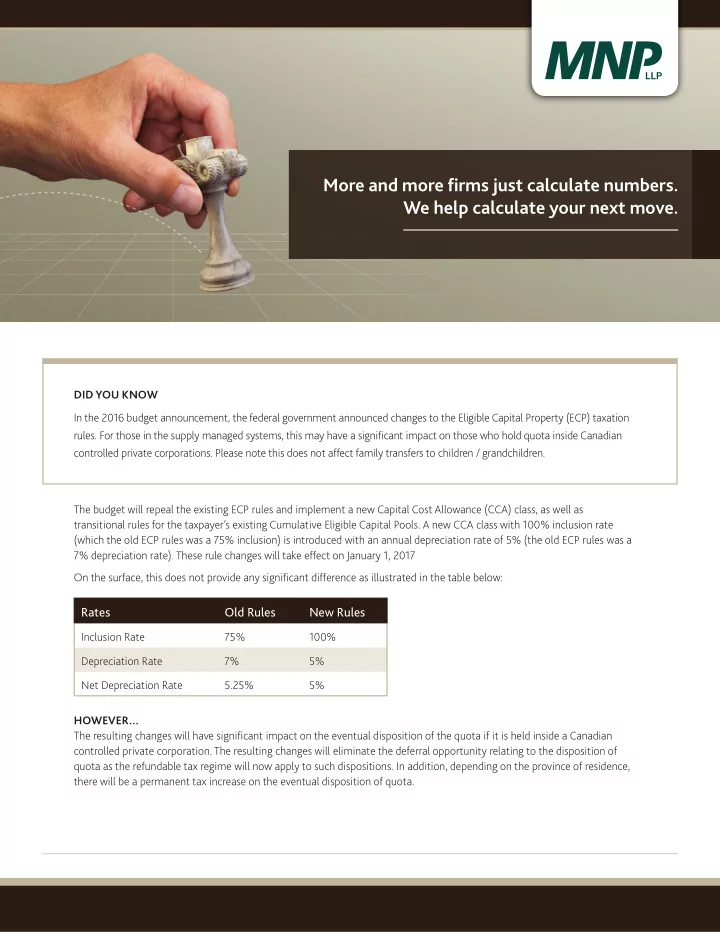

More and more firms just calculate numbers. We help calculate your next move. DID YOU KNOW In the 2016 budget announcement, the federal government announced changes to the Eligible Capital Property (ECP) taxation rules. For those in the supply

More and more firms just calculate numbers. We help calculate your next move. DID YOU KNOW In the 2016 budget announcement, the federal government announced changes to the Eligible Capital Property (ECP) taxation rules. For those in the supply managed systems, this may have a significant impact on those who hold quota inside Canadian controlled private corporations. Please note this does not affect family transfers to children / grandchildren. The budget will repeal the existing ECP rules and implement a new Capital Cost Allowance (CCA) class, as well as transitional rules for the taxpayer’s existing Cumulative Eligible Capital Pools. A new CCA class with 100% inclusion rate (which the old ECP rules was a 75% inclusion) is introduced with an annual depreciation rate of 5% (the old ECP rules was a 7% depreciation rate). These rule changes will take effect on January 1, 2017 On the surface, this does not provide any significant difference as illustrated in the table below: Rates Old Rules New Rules Inclusion Rate 75% 100% Depreciation Rate 7% 5% Net Depreciation Rate 5.25% 5% HOWEVER… The resulting changes will have significant impact on the eventual disposition of the quota if it is held inside a Canadian controlled private corporation. The resulting changes will eliminate the deferral opportunity relating to the disposition of quota as the refundable tax regime will now apply to such dispositions. In addition, depending on the province of residence, there will be a permanent tax increase on the eventual disposition of quota.

For example, let’s say you purchased quota for $100,000 and it is now worth $1,000,000. For simplicity, we will assume no depreciation was taken on the original purchase. We will assume the highest marginal tax rates for British Columbia resident in 2016. The contrast in the rules is outlined in the table below: Corporate Taxes Old Rules New Rules Sale Price 1,000,000 1,000,000 Inclusion Rate 75% 100% Reportable Proceeds 750,000 1,000,000 Less: Original Purchase Price 100,000 100,000 Inclusion Rate 75% 100% Net 75,000 100,000 Net Reportable Income from Sale 675,000 900,000 Taxable Income Inclusion 67% 50% Taxable Income 450,000 450,000 Corporate Tax Rate 13.00% 49.67% Estimated Corporate Taxes 58,500 223,515 Refundable Taxes on payment of Dividend to Shareholders 138,015 Net Corporate Taxes 58,500 85,500 Cash Distributions (Deferral) Proceeds from Sale 1,000,000 1,000,000 Estimated Corporate Taxes -58,500 -85,500 Cash Available before distributions 941,500 914,500 Necessary Dividend to recover Refundable Taxes 360,070 Available Cash for reinvestment or distribution 941,500 554,430 Deferral Advantage Lost $ 387,070 Cash Flow to Shareholders (Immediate) Dividend to Shareholder 360,070 Estimated Personal Taxes on Dividend Above (40%) -146,225 Tax Free Dividend Available 450,000 450,000 Eventual Distribution of remaining cash (deferral advantage) Taxable Dividend (ineligible) 491,500 104,430 Estimated Taxes on Dividend (40.61%) -199,598 -42,409 Total After Tax Cash to Shareholder 741,902 725,867 Combined Taxes (Corporate & Personal) 258,098 274,133

As noted in the table above, the new rules will have the effect of an overall net tax increase on quota held in the corporation, but more importantly the lost deferral opportunity to utilize after tax cash to reinvest back into your farming business, pay down debt or reinvest in another business venture. HAVE YOU CONSIDERED… Given the significant changes in the ECP rules, what effect will this have in your planning? If you plan to continue farming for the foreseeable future (say more than five years out), these rule changes will likely not change any of your planning. However, if there were thoughts of selling some or all of your quota within the next five years, there may be planning opportunities to maximize your results by taking action today. There is a limited time to utilize the more favourable ECP rules to your benefit. This does not mean you necessarily have to go out and sell quota today, there is the ability to utilize favourable rules in our Income Tax Act to your benefit without the need to sell quota today. ABOUT MNP MNP is a leading national accounting, tax and business consulting firm for Canada’s agriculture industry. We have invested more time and resources into understanding agriculture than any other firm. With more than 15,000 agriculture clients and a team of over 600 agriculture specialists, MNP delivers a diverse suite of services to protect farmers and maximize results. Please contact Christopher Tilbury, Regional Tax Leader, Fraser Valley at 604.853.9471 or christopher.tilbury@mnp.ca

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.