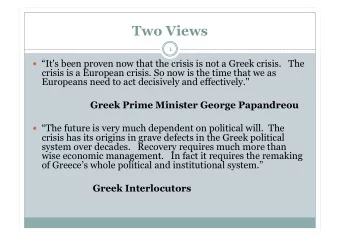

Looking Beyond The Greek Crisis and Lessons for Europe Yannis M. Ioannides Tufts University Confer` encia XREPP, Universitat de Girona, March 18, 2015

Greek Great Recession Competitiveness Expectations Reinventions EU/EZ a crossroads Macro policy tools in view of the Great Greek Great Recession 1 Competitiveness 2 Expectations 3 Reinventions 4 EU/EZ a crossroads 5 Macro policy tools in view of the Great Recession 6 EU vs. US 7 Fiscal Union 8 European Fiscal Compact 9 10 Lessons 11 Conclusions Girona March 18, 2015 Yannis M. Ioannides Tufts University

Greek Great Recession Competitiveness Expectations Reinventions EU/EZ a crossroads Macro policy tools in view of the Great Outline • Crises • Greek Great Recession, vs. Ireland, Portugal • US Great Depression (1929-1938): standard reference • Finnish Great Depression (1990-1997): Finland’s most severe since 1929 • Crises end, with restructuring • Competitiveness • Structural reforms to unleash technological progress, competitiveness • Small improvements grow geometrically in the long run • Investments: human and physical capital, infrastructure • Quality of education, rule of law, and institutions • Aim at world markets, internal linkages will follow • Reinventions Girona March 18, 2015 Yannis M. Ioannides Tufts University

2008 Q1 = 100 2008 Q1 = 100 105 105 Real GDP 100 100 95 95 90 90 85 85 Greece 80 80 Ireland Latvia Portugal 75 75 2008 09 10 11 12 13

2008 Q1 = 100 2008 Q1 = 100 105 105 Real GDP 100 100 95 95 90 90 85 85 Greece 80 80 Ireland Latvia Portugal 75 75 2008 09 10 11 12 13

2008 Q1 = 100 2008 Q1 = 100 105 105 Real GDP 100 100 95 95 90 90 85 85 Greece 80 80 Ireland Latvia Portugal 75 75 2008 09 10 11 12 13

Greek Great Recession Competitiveness Expectations Reinventions EU/EZ a crossroads Macro policy tools in view of the Great Outline • Crises • Greek Great Recession, vs. Ireland, Portugal • US Great Depression (1929-1938): standard reference • Finnish Great Depression (1990-1997): Finland’s most severe since 1929 • Crises end, with restructuring • Competitiveness • Structural reforms to unleash technological progress, competitiveness • Small improvements grow geometrically in the long run • Investments: human and physical capital, infrastructure • Quality of education, rule of law, and institutions • Aim at world markets, internal linkages will follow • Reinventions Girona March 18, 2015 Yannis M. Ioannides Tufts University

Greek Great Recession Competitiveness Expectations Reinventions EU/EZ a crossroads Macro policy tools in view of the Great Understanding the Greek Crisis • Fiscal contraction + cutoff of bank credit + persistent uncertainties related to public debt + one third fall of the real wage + pessimistic expectations + collapse of investment ⇒ Contraction of aggregate demand ⇒ huge rise in unemployment, accentuated by pervasive frictions • Accomplished huge reduction in unit labor costs • Product market rigidities prevented huge commensurate price reductions. KEPE 2015, 1.3.1, 1.3.2 • Huge reduction in living standards. ELSTAT Jan. 23, 2015 • Structural reforms to improve competitiveness, ease price adjustment, reallocate resources to most productive sectors and exports. • Modernization of public services to raise trust, increase tax compliance, strengthen rule of law, encourage foreign investment. Girona March 18, 2015 Yannis M. Ioannides Tufts University

Καθαπή σοπήγηζη(+) / καθαπή λήτη(-) δανείυν Σςνολική οικονομία Εκαη. € Κατά το τρίτο τρίμθνο του 2014, το διακζςιμο ειςόδθμα του τομζα των νοικοκυριϊν και των μθ κερδοςκοπικϊν ιδρυμάτων που εξυπθρετοφν νοικοκυριά (ΜΚΙΕΝ) – αυξικθκε οριακά κατά 3% ςε ςφγκριςθ με το αντίςτοιχο τρίμθνο του προθγοφμενου ζτουσ, από 31,16 δις. ευρϊ ςε 31,17 δις. ευρϊ. Η τελικι καταναλωτικι δαπάνθ των νοικοκυριϊν και των μθ κερδοςκοπικϊν ιδρυμάτων που εξυπθρετοφν νοικοκυριά, αυξικθκε κατά 2,3% ςε ςφγκριςθ με το αντίςτοιχο τρίμθνο του προθγοφμενου ζτουσ, από 32,6 δις. ευρϊ ςε 33,3 δις. ευρϊ. Εξέλιξη ηος ακαθάπιζηος διαθέζιμος ειζοδήμαηορ και ηηρ καηαναλυηικήρ δαπάνηρ ηυν Νοικοκςπιών και ΜΚΙΕΝ (μεηαβολή ζε ζτέζη με ηο ανηίζηοιτο ηρίμηνο ηοσ προηγούμενοσ έηοσς) 15,0% 10,0% 5,0% 0,0% -5,0% -10,0% -15,0% 2007Q1 2007Q2 2007Q3 2007Q4 2008Q1 2008Q2 2008Q3 2008Q4 2009Q1 2009Q2 2009Q3 2009Q4 2010Q1 2010Q2 2010Q3 2010Q4 2011Q1 2011Q2 2011Q3 2011Q4 2012Q1 2012Q2 2012Q3 2012Q4 2013Q1 2013Q2 2013Q3 2013Q4 2014Q1 2014Q2 2014Q3 Ακαθάριζηο διαθέζιμο ειζόδημα Τελική καηαναλωηική δαπάνη Το ποςοςτό αποταμίευςθσ των νοικοκυριϊν και των ΜΚΙΕΝ, που ορίηεται ωσ θ ακακάριςτθ αποταμίευςθ προσ το ακακάριςτο διακζςιμο ειςόδθμα, ιταν –7,0% κατά το τρίτο τρίμθνο του 2014, ςε ςφγκριςθ με το τρίτο τρίμθνο του 2013. 2

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries