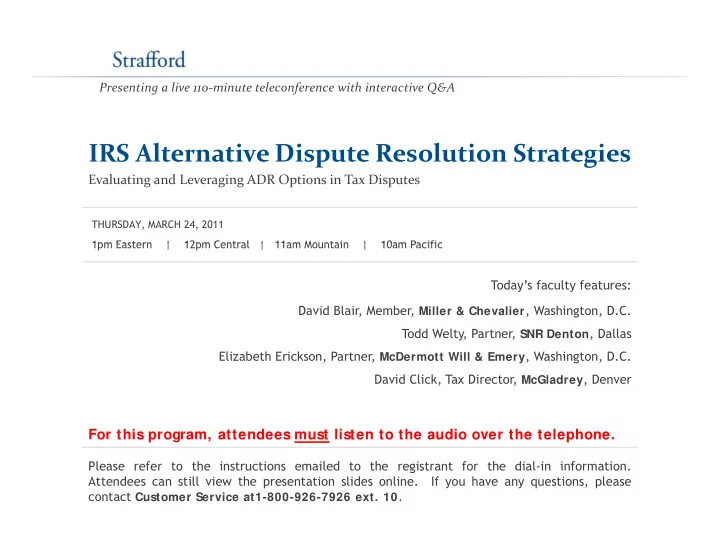

Presenting a live 110 ‐ minute teleconference with interactive Q&A IRS Alternative Dispute Resolution Strategies Evaluating and Leveraging ADR Options in Tax Disputes THURSDAY, MARCH 24, 2011 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific Today’s faculty features: David Blair Member Miller & Chevalier Washington D C David Blair, Member, Miller & Chevalier , Washington, D.C. Todd Welty, Partner, SNR Denton , Dallas Elizabeth Erickson, Partner, McDermott Will & Emery , Washington, D.C. David Click, Tax Director, McGladrey , Denver David Click, Tax Director, McGladrey , Denver For this program, attendees must listen to the audio over the telephone. Please refer to the instructions emailed to the registrant for the dial-in information. Attendees can still view the presentation slides online. If you have any questions, please contact Customer Service at1-800-926-7926 ext. 10 .

Conference Materials If you have not printed the conference materials for this program, please complete the following steps: Click on the + sign next to “Conference Materials” in the middle of the left- • hand column on your screen hand column on your screen. Click on the tab labeled “Handouts” that appears, and there you will see a • PDF of the slides for today's program. Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open. • Print the slides by clicking on the printer icon. •

Continuing Education Credits FOR LIVE EVENT ONLY Attendees must listen to the audio over the telephone . Attendees can still view the presentation slides online but there is no online audio for this program. Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10 . at 1 800 926 7926 ext. 10 .

Tips for Optimal Quality S S ound Qualit y d Q lit For this program, you must listen via the telephone by dialing 1-866-871-8924 and entering your PIN when prompted. There will be no sound over the web co connection. ect o . If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail sound@straffordpub.com immediately so we can address the problem. Viewing Qualit y To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again press the F11 key again.

IRS Alternative Dispute Resolution IRS Alt ti Di t R l ti Strategies Seminar March 24, 2011 David Click, McGladrey David Blair, Miller & Chevalier david.click@mcgladrey.com dblair@milchev.com Elizabeth Erickson, McDermott Will & Emery Todd Welty, SNR Denton eerickson@mwe.com todd.welty@snrdenton.com

Today’s Program Background On IRS And ADR Offerings Slide 7 – Slide 17 [David Click] Pre-Filing ADR Options Slide 18 – Slide 38 [David Blair] ADR Options Before The Audit Closes Slide 39 – Slide 59 [Elizabet h Erickson] ADR Options After The Audit Is Finished Slide 60 – Slide 82 [Todd Welt y]

David Click, McGladrey BACKGROUND ON IRS AND BACKGROUND ON IRS AND ADR OFFERINGS

Evolution Of Alternative Dispute Resolution In Tax IRS Appeals: Traditional dispute resolution P Pre-assessment cases: 30-day letter process t 30 d l tt Appeals has jurisdiction over cases for which the IRS has not made an assessment of tax. Typical cases include: yp Income tax, estate, gift and excise tax before or after a • notice of deficiency Employment tax liabilities • Additions to tax (penalties) • 8

Evolution Of Alternative Dispute Resolution In Tax (Cont.) Limited jurisdiction in docketed cases Appeals has limited jurisdiction in cases that are docketed before the Tax Court. Generally, Appeals will not consider a case if Appeals issued the stat notice. The case is considered by Appeals but is in counsel’s jurisdiction subject to being put on a trial calendar by the Tax Court. Counsel may start trial preparation but allow Appeals to continue negotiating. Pre-trial order of the Tax Court: 60 days – meet to resolve case 30 days – Joint case status report 20 days – Trial memos due to Tax Court y Other dispute resolution approaches Private letter rulings D t Determination letters i ti l tt Technical advice memorandum 9

Genesis Of Alternative Dispute Resolution With The IRS Resolution With The IRS Administrative Issues in the 1980s ― Implementation of IRS large case program ― TEFRA partnership procedures – 1982 TEFRA t hi d 1982 ― Tax Court dockets – Tax shelters 1988: Office of Management and Budget recommends arbitration 1988: Office of Management and Budget recommends arbitration process for Tax Court cases. 1990: Administrative dispute resolution encouraged all federal agencies to use alternative dispute techniques to resolve disputes. 1991: Tax Court Rule 124 on use of arbitration in docketed cases 1991: Tax Court Rule 124 on use of arbitration in docketed cases, supervised by Tax Court 10

IRS: First Steps In Alternative Dispute Resolution i l i Delegation Order 236 (1991): Delegates authority to Exam Delegation Order 236 (1991): Delegates authority to Exam managers to settle issues consistent with an Appeals settlement Advanced pricing agreements and Rev. Proc. 91-22: Allow taxpayers and IRS to agree on transfer pricing methodology and a range of transfer pricing results Competent authority and Appeals: Rev Proc 91-23 and Rev Proc Competent authority and Appeals: Rev. Proc. 91-23 and Rev. Proc. 2002 -52 Accelerated issue resolution and Rev. Proc. 94-67: Allow accelerated resolution of an issue affecting more than one tax year 11

Expanded Appeals Settlements Early referral to appeals and Rev. Proc. 99-28: Allow issues at Exam level to be elevated to Appeals for resolution Mediation and arbitration: Pilot program in IRS Announcement 2000-4; made permanent in Rev. Proc. ; p 2002-44 (mediation) and Rev. Proc. 2006-44 (arbitration) 12

IRS Restructuring And Reform Act Of 1998 g Substantially expanded Appeals jurisdiction over matters handled by the IRS Administrative due process review of a jeopardy assessment d st at ve due p ocess ev ew o a jeopa dy assess e t • Requests for administrative costs • Due process review in collection cases • Administrative review in the rejection of an offer in • compromise Appeals of denial of interest abatement under Sect. 6404(e) pp ( ) • Alternative dispute resolution • 13

Reorganization Of IRS Business Units Large and medium sized business division: Becomes operational June 2000 Pre-filing agreements: Notice 2000-12 – made permanent in Rev. • Proc. 2005-15 Comprehensive case resolution: Notice 2000-43 • Industry issue resolution: Notice 2000-65 • Continuous audit program: 2005 Continuous audit program: 2005 • LMSB appeals: Operational in August 2000 Fast-track dispute resolution: Notice 2001-67. Program was • expended and made permanent in Rev. Proc. 2003-40. 14

Industry Issue Focus (IIF) And Tiered Issues 2007: IRS unveils its industry issue focus (IIF) approach to examination issues. The stated goals of the approach are: Consistency of resolution across industry lines Co s ste cy o esolut o ac oss dust y l es • Improved currency • Increased coverage of non-compliant taxpayers by • maximizing limited resources Greater oversight on and accountability for important • issues D Develops issue management teams between Exam and Appeals l i b E d A l 15

Is Appeals Independent? Tiered issues are managed by a team and require sign-off before the issue is resolved at Exam or Appeals. Both Exam and Appeals are involved in issue management teams and develop settlement guidelines. IRS industry specialists often advise both Exam and Appeals often advise both Exam and Appeals. Treasury Inspector General for Tax Administration report in 2005 raises independence concerns. 16

A ADR S An ADR Strategy: Pros And Cons P A d C Benefits of ADR Benefits of ADR Resolution of uncertain tax positions (UTPs) • Cooperative use of resources • Improved relationship with IRS • Manage tax risk • Risks of using ADR Some issues may not be capable of resolution through • ADR. ADR. Participation of both Exam and Appeals • Waiver of ex part e rules • p Resource allocation for piecemeal ADR process • 17

David Blair, Miller & Chevalier PRE FILING ADR OPTIONS PRE ‐ FILING ADR OPTIONS

Pre-Filing ADR Options • IRS programs provide the opportunity to resolve issues prior to filing return. Pre-filing agreements/CAP Pre filing agreements/CAP Advance pricing agreements 19

Pre-Filing ADR Options (Cont.) • Benefits of resolving issues at pre-filing stage Eliminate tax uncertainty Avoid FIN 48 and Schedule UTP disclosures Avoid “hot interest” under Code § 6621(c) Resolution is non-public p Reduce costs relative to appeals, litigation 20

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries