Investor Presentation 3Q16 Financial Results April 2017 November - PowerPoint PPT Presentation

Hegh LNG Partners LP The Floating LNG Infrastructure MLP Investor Presentation 3Q16 Financial Results April 2017 November 17, 2016 Forward-Looking Statements This presentation contains certain forward-looking statements concerning future

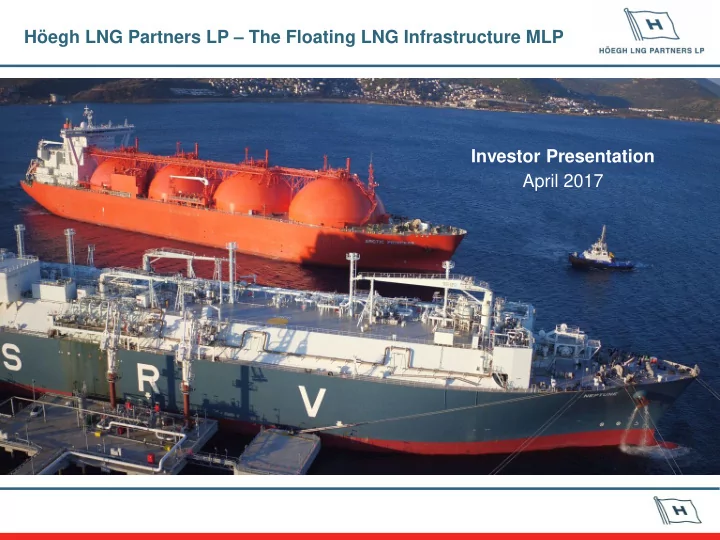

Höegh LNG Partners LP – The Floating LNG Infrastructure MLP Investor Presentation 3Q16 Financial Results April 2017 November 17, 2016

Forward-Looking Statements This presentation contains certain forward-looking statements concerning future events and our operations, performance and financial condition. Forward- looking statements include, without limitation, any statement that may predict, forecast, indicate or imply future results, performance or achievements, and may contain the words “believe,” “anticipate,” “expect,” “estimate,” “project,” “will be,” “will continue,” “will likely resu lt, ” “plan,” “intend” or words or phrases of similar meanings. These statements involve known and unknown risks and are based upon a number of assumptions and estimates that are inherently subject to significant uncertainties and contingencies, many of which are beyond our control. Actual results may differ materially from those expressed or implied by such forward-looking statements. Important factors that could cause actual results to differ materially include, but are not limited to: FSRU and LNG carrier market trends, including hire rates and factors affecting supply and demand; our anticipated growth strategies; our anticipated receipt of dividends and repayment of indebtedness from subsidiaries and joint ventures; the effects of volatility in global prices for crude oil and natural gas; the effect of the worldwide economic environment; turmoil in the global financial markets; fluctuations in currencies and interest rates; general market conditions, including fluctuations in hire rates and vessel values; changes in our operating expenses, including drydocking and insurance costs; our ability to make or increase cash distributions on the units and the amount of any such distributions; our ability to comply with financing agreements and the expected effect of restrictions and covenants in such agreements; the future financial condition of our existing or future customers; our ability to make additional borrowings and to access public equity and debt capital markets; planned capital expenditures and availability of capital resources to fund capital expenditures; the exercise of purchase options by customers; our ability to maintain long-term relationships with our customers; our ability to leverage the relationships of Höegh LNG Holdings (“HLNG”) and its reputation in the shipping industry; our ability to purchase the 49% interest in the Höegh Grace entities or additional vessels from Höegh LNG in the future; our ability to integrate and realize the anticipated benefits from the acquisition of the 51% interest in the Höegh Grace entities ; our continued ability to enter into long-term, fixed-rate charters; the operating performance of our vessels; our ability to maximize the use of our vessels, including the redeployment or disposition of vessels no longer under long-term charters; expected pursuit of strategic opportunities, including the acquisition of vessels; our ability to compete successfully for future chartering and newbuilding opportunities; timely acceptance of our vessels by their charterers; termination dates and extensions of charters; the cost of, and our ability to comply with, governmental regulations and maritime self-regulatory organization standards, as well as standard regulations imposed by our charterers applicable to our business; demand in the FSRU sector or the LNG shipping sector in general and the demand for our vessels in particular; availability of skilled labor, vessel crews and management; our incremental general and administrative expenses as a publicly traded limited partnership and our fees and expenses payable under the ship management agreements, the technical information and services agreement and the administrative services agreements; the anticipated taxation of Höegh LNG Partners LP and distributions to our unitholders; estimated future maintenance and replacement capital expenditures; our ability to retain key employees; customers ’ increasing emphasis on environmental and safety concerns; potential liability from any pending or future litigation; potential disruption of shipping routes due to accidents, political events, piracy or acts by terrorists; future sales of our common units in the public market; our business strategy and other plans and objectives for future operations; our ability to successfully remediate any material weaknesses in our internal control over financial reporting and our disclosure controls and procedures; and other factors listed from time to time in the reports and other documents that we file with the SEC, including our Annual Report on Form 20-F for the year ended December 31, 2016 and subsequently quarterly reports on Form 6-K. All forward-looking statements included in this presentation are made only as of the date hereof. We do not intend to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in our expectations with respect thereto or any change in events, conditions or circumstances on which any such statement is based. 2

Glossary “HMLP” – Höegh LNG Partners LP “HLNG” – Höegh LNG Holdings Ltd. “Höegh LNG Group” – HMLP and HLNG “Grace Holding” – The sole owner of the entities that own and operate the Höegh Grace “FSRU” – Floating Storage and Regasification Unit “ABKN” – AB Klaipedos Nafta “EGAS” – Egyptian Natural Gas Holding Company “PGN” – Perusahaan Gas Negara “GNL Penco” – Import terminal in Chile (JV of Biobiogenera , Cheniere and EDF) “SPEC” – Sociedad Portuaria El Cayao S.A. E.S.P. (JV of Promigas and private equity) “GEI” – Global Energy Infrastructure Ltd. 3

Höegh LNG Partners LP – A Differentiated LNG Infrastructure Provider Höegh LNG Group The only pure play FSRU company Most modern FSRU fleet in the market Höegh LNG 12.2 years average remaining contract length Holdings Ltd. MLP Investors (Oslo Børs: HLNG ) Firm contract backlog of $2.2 billion (1) Operations world-wide: 46.4% (2) 53.6% LNG Infrastructure asset development Green – operational Yellow – development A Growth-Oriented MLP Providing Critical Energy Infrastructure on Stable , Long-term Contracts (1) $6.2 billion of firm contract backlog across Höegh LNG Group; backlog is calculated as the full monthly hire rate multiplied by the number of months remaining on the contract, assuming full utilization. 4 (2) Consists of approximately 10.7% of the total outstanding common units and 100% of the outstanding subordinated units. HLNG also holds all of the incentive distribution rights.

Höegh LNG Partners LP (NYSE:HMLP) – Investment Summary • The only publicly listed FSRU pure play Pure Play Owner and Operator of FSRUs • Current fleet of five FSRUs on long-term, fixed-rate contracts • Average vessel age of 3.8 years (1) Modern Fleet Providing • Meeting critical energy infrastructure needs Critical Energy Infrastructure • Leading player in highly concentrated FSRU market • Average remaining contract term of 12.2 years plus options (2) Full Employment on • Earliest contract expiry in 2025 (3) , with no near-term debt maturities Fixed, Long-term Contracts • No direct commodity exposure and limited Opex exposure (4) • Committed pipeline of high-quality dropdown assets Dropdown Pipeline for • Dropdowns typically evaluated once assets go on long-term contract Built-in Distribution Growth • Accretive acquisitions of FSRUs expected to drive distribution growth • LNG is especially competitive fuel at current prices Attractive FSRU Market • Readily available LNG supply drives FSRU adoption globally Conditions • Oil and coal displacement with environmental benefits over both • Recognized leader in the LNG space for 40+ years Supportive, • Extensive technical and maritime expertise and relationships Industry-Leading Sponsor • Favorable financing terms highlight value of sponsor support (1) As of March 31, 2017 (2) As of March 31, 2017 including the Höegh Grace , 19.2 years including options 5 (3) Includes HMLP option to charter FSRU Höegh Gallant to HLNG after end of EGAS contract (4) Extent of Opex exposure depends on vessel contract

Stable Cash Flows, Fully Covered Distributions and Growth Segment EBITDA (1)(2) ,$m Adj. Net Income (1) , $m 30 30.0 25.8 25.7 24.3 24.9 24.1 25 25.0 20 20.0 16.1 15.2 15.2 15 15.0 9.9 8.8 8.0 7.9 8.1 10 7.6 10.0 6.8 6.8 5 5.0 0 0.0 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 Distribution, $/unit Distributable Cash Flow (1) , $m 30.0 0.6 +4.24% Coverage (1) : +22% 1.18x 1.0x 1.15x 1.14x 0.97x (3) 25.0 0.5 0.43 0.4125 0.4125 0.4125 0.4125 0.4125 1.21x (4) 20.0 0.4 0.3375 0.3375 0.3375 13.3 12.9 12.7 15.0 12.5 0.3 11.0 9.6 9.1 9.2 10.0 0.2 5.0 0.1 0.0 0.0 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 Distribution (1) Adjusted Net Income, Segment EBITDA, Distributable cash flow and Coverage are non-GAAP financial measures. For a definition of each of these non-GAAP financial measures and reconciliations to their most directly comparable US GAAP financial measure, please see the Appendix. (2) Excludes principal payment on direct financing lease, amortization in revenues for above market contracts and equity in earnings of JVs: amortization for deferred revenue. 6 (3) 0.97x based on distribution for 4Q16 (4) Reflects distribution coverage on units existing prior to common unit offering in December 2016.

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.