Implementation of Basel Core Principles for Effective Banking - PowerPoint PPT Presentation

Implementation of Basel Core Principles for Effective Banking Supervision in the context of Bangladesh Presented by: Sarder Azizur Rahman Student ID-112286 Student ID-112286 Examination Committee: Mr.Weerakoon Wijewardena (Chairperson) Dr.

Implementation of Basel Core Principles for Effective Banking Supervision in the context of Bangladesh Presented by: Sarder Azizur Rahman Student ID-112286 Student ID-112286 Examination Committee: Mr.Weerakoon Wijewardena (Chairperson) Dr. Winai Wongsurawat (Co-chair) Dr. Sundar Venkatesh (Member)

Agenda of the Presentation: 1. Objective of the study 2. Research Methodology 3. Brief introduction about Bangladesh Bank 4. Basel Principles 4. Basel Principles 5. Why Basel Accord is needed 6. Findings in Bangladesh Perspective 7. Recommendation and Conclusion

Objective of the research � To explore an overview of the BASEL Accords and Basel core principles for effective Banking supervision � To assess the compliance status of the BASEL core principles of banking supervision in Bangladesh. principles of banking supervision in Bangladesh. � To review the need of Basel II in place of Basel I Accord and make a comparison between them. � To study the implications and impact of Basel Core principles in Banking Supervision in Bangladesh.

Research Methodology � Exhaustive study � Analysis Analysis � Inference

Brief introduction about Bangladesh Bank � Central Bank of Bangladesh � Formed under presidential order 1972 ,127(A) � Follows The Bank Company Act 1991 � Follows The Bank Company Act 1991 � Started to implement Basel Core Principles since 2002 under the FSAP carried out by IMF and World Bank � Basel Core Principles for Effective Banking Supervision is conducted by ‘Basel II implementation cell of BRPD. Officially kicked off from 2010.

What is Basel The Basel Accords refer to the banking supervision Accords Basel I, Basel II and Basel III issued by the Basel Committee on Banking Supervision (BCBS). They are called the Basel Accords as the BCBS maintains its secretariat at the Bank for International Settlements in Basel, Switzerland.

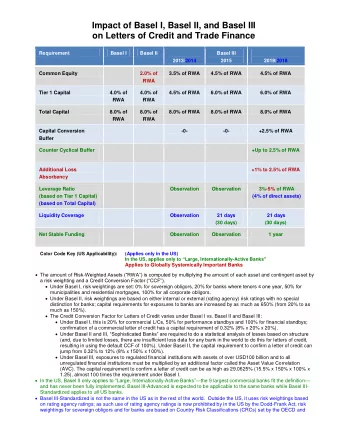

Basel I � 1988 with a set of minimum capital requirements for banks. or � Basel I credit risk. Assets of banks were classified and � Basel I credit risk. Assets of banks were classified and grouped in five categories according to credit risk. Risk weights of zero (for example home country sovereign, debt), ten, twenty, fifty, and up to one hundred percent. Banks with international presence are required to hold capital equal to 8 % of the risk-weighted assets.

Few shortcomings of Basel I � Basel I framework does not make adequate differentiation of credit risk, although the risk is different as the recovery of the two instruments would be different. � There is no recognition of the term structure of credit risk. � The current rules do not recognize the portfolio diversification effects for credit risk while at the same time recognizing it for market risk for credit risk while at the same time recognizing it for market risk under the internal VAR models of banks. As a result the current rules under the internal VAR models of banks. As a result the current rules can represent a false picture of the riskiness of an institution. � The current Accord does not give due recognition to the credit risk mitigation techniques and does not recognize the role collateral can play in reducing the losses on account of credit risk. � The 1988 accord does not levy any capital charge for operational risk although that is a very important source of risk and can be more devastating than credit risk.

Basel II � Basel II, initially published in June 2004. � For creating international standard for banking regulators to control how much capital banks need to put aside to guard against the types of financial and operational risks banks face. � To maintain sufficient consistency of regulations so that this does not become a source of competitive inequality amongst does not become a source of competitive inequality amongst internationally active banks. � In theory, Basel II attempted to accomplish this by setting up risk and capital management requirements designed to ensure that a bank has adequate capital for the risk the bank exposes itself to through its lending and investment practices. In general the greater risk to which the bank is exposed, the greater the amount of capital the bank needs to hold to safeguard its solvency and overall economic stability

Basel II (Cont..) Basel II consists of three pillars: Basel II consists of three pillars: � Minimum capital requirements for credit risk, market risk and operational risk—expanding the 1988 Accord (Pillar I) � Supervisory review of an institution’s capital adequacy and internal assessment process (Pillar II) � Effective use of market discipline as a lever to strengthen disclosure and encourage safe and sound banking practices (Pillar III)

Principles � Principle 1 Preconditions for effective banking supervision � Principles 2 – 5 Licensing and structure � Principles 6 -15 � Principles 6 -15 Prudential regulations and requirements Prudential regulations and requirements � Principles 16-20 Methods of ongoing banking supervision � Principles 21 Information requirements � Principles 22 Formal powers of supervisors � Principles 23- 25 Cross-border banking Basel Implementation in Bangladesh.docx

Analysis

Preconditions for effective banking supervision and Licensing � Assessment : � Section 44 of the Bank Companies Act, 1991 vests powers in Bangladesh Bank for inspection of books of any banking company at any time. � A suitable legal framework is in place for the BB to take action as needed against banks, and the BB take action as needed against banks, and the BB appears to use these powers as needed. In the light of qualitative judgment and BB by law has access to bank records. Compliance Level: Largely Compliant.

Capital Adequacy Assessments According to BB circular No. 01, 08-01-1996, Capital adequacy takes account of different degrees of credit risk and covers both on balance sheet and off balance sheet transactions. transactions. Minimum Capital Standard: Each bank will maintain a ratio of capital to risk weighted assets of 400 Crore or 10% of risk weighted assets which one is higher. Compliance Level: Largely Compliant.

Assessment of the risk factors Country and Transfer Risk 1. Bangladeshi banks in overseas operations need to follow the internal guidelines on country risk management and fix based on risk rating of the country. Limits should also be fixed for a group of countries in a particular risk category subject to a maximum ceiling fixed by Bangladesh Bank. 2. For investment in abroad by banks, permission of Bangladesh Bank is necessary according to BRPD circular no. 1/96. necessary according to BRPD circular no. 1/96. Market risk 1. Under section 49 of the Banking Company Act, 1991 to impose specific limit and/or specific charge on market risk exposures. 2. The capital charge for some of the market risks already exists. Market risks in the investment Portfolio are controlled through quantitative restrictions, (BRPD circular no. 2/95 ). Compliance Level: Compliant

Other risk management (e.g. Liquidity risk, Interest Rate risk, Currency risk) Already issued guidelines for banks to set up effective Asset- Liability management (ALM) System. � Liquidity risk management: All banks are required to maintain Cash Reserve Ratio (CRR) and statutory Liquidity Ratio (SLR) as per section 36(1) of Bangladesh Bank order, 1972 and section 24(2a) of the Banking Company Act, 1991 respectively. � Interest Rate Risk Management: The banks are expected to measure interest rate risk through traditional gap analysis supplemented by sophisticated techniques wherever possible. � Currency Risk Management: The banks are to assign 100% risk weight to their open position limit in foreign exchange. Besides, they are required to fix aggregate and individual limits for each currency with the approval of Bangladesh Bank. They are required to adopt value at risk associated with forward exposures. The Bangladesh Bank monitors currency risk through a monthly return on maturity and positions for both on and of balance sheet items in foreign exchange. Compliance Level: Largely Compliant crd_risk01.pdf

Internal control and know your Customer � Examination and evaluation of the adequacy and effectiveness of the internal Control System in the banks form one of the important aspects during on-site inspection by the Bangladesh Bank periodically. � In Bangladesh, ‘ Know your Customer’ Rules are in place right form the beginning. There are specific directions for obtaining proper introduction introduction while while opening opening Deposit “Accounts. Deposit “Accounts. Requirement of Requirement of obtaining photographs of account holders before opening accounts has been prescribed. Numbered accounts are not permitted in Bangladesh. � Anti-Money Laundering Act 2002 has been enacted in 2003 in this regard. Compliance Level: Largely Compliant

Methods of Ongoing Banking Supervision (a) The main instrument of supervision in Bangladesh is the periodical on-site inspection of banks that is supplemented by off-site monitoring and supervision. Since 1995, on-site inspections are based on CAMEL Rating. The domestic banks were rated on CAMEL model. (b)Two separate departments were established in Bangladesh Bank for the supervision and examination purposes: � Department of Off-site Supervision (DOS); and � Department of Banking Inspection (DBI). � Compliance Level: Largely Compliant

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.