H.-W. Sinn Th The E e European pean Balanc ance-of of-Paymen - PowerPoint PPT Presentation

H.-W. Sinn Th The E e European pean Balanc ance-of of-Paymen ments Cris isis is Hans-Werner Sinn May 2012 H.-W. Sinn 1. The bubble 2. The balance-of-payments crisis 3. The loss of competitiveness 4. The cost of the rescue operations

H.-W. Sinn

Th The E e European pean Balanc ance-of of-Paymen ments Cris isis is Hans-Werner Sinn May 2012 H.-W. Sinn

1. The bubble 2. The balance-of-payments crisis 3. The loss of competitiveness 4. The cost of the rescue operations 5. Two options for Europe H.-W. Sinn

1. The bubble H.-W. Sinn

Net yields for 10-year government bonds % 40 Irrevocably fixed conversion rates 35 Introduction of virtual euro EU Summit in Madrid 30 Greece 25 Introduction of 20 euro cash 15 Portugal 10 Ireland Spain Italy 5 Belgium France Germany 0 1985 1990 1995 2000 2005 2010 Source: Thomson Reuters Datastream. H.-W. Sinn

Net yields for 10-year government bonds % 40 Irrevocably fixed conversion rates 35 Introduction of virtual euro Conference of 30 EU governments Greece in Madrid 25 Introduction of 20 euro cash 15 Portugal 10 Ireland Spain Italy 5 Belgium France Germany 0 1985 1990 1995 2000 2005 2010 Source: Thomson Reuters Datastream. H.-W. Sinn

2. The loss of competitiveness H.-W. Sinn

Price development 1995-2008 % Slovenia 108 Slovakia 82 Greece 67 Spain 56 Trade-weighted appreciation Ireland 53 Cyprus vis-à-vis other 51 Portugal 47 euro countries: Luxembourg 44 Italy 40 GIIPS: + 30% Netherlands 37 Eurozone 26 Germany: - 22% Belgium 25 France 25 Finland 22 Austria 17 Germany 9 0 20 40 60 80 100 Source: Eurostat, calculations by the Ifo Institute. March 2012 H.-W. Sinn

Necessary real write-down in the Eurozone (Goldman Sachs) Portugal 35% Greece 30% Spain 20% France 20% Italy 10% to 15% Ireland 0% to 5% Source: Goldman Sachs. H.-W. Sinn

Real exchange rate (GDP deflator relative to rest of Eurozone) Index Q3 - 2008=100 108 Ireland 104 Greece Italy Portugal 100 France Spain 96 92 88 2005 2006 2007 2008 2009 2010 2011 Source: European Commission. H.-W. Sinn

H.-W. Sinn

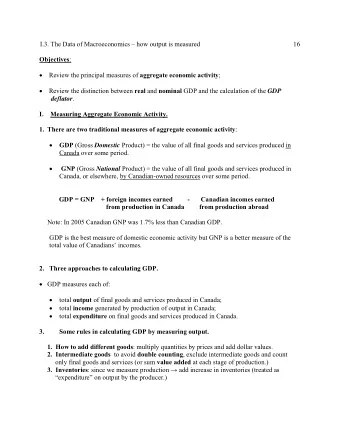

3. The balance-of-payments crisis (Sinn & Wollmershäuser, CESifo WP 3500, NBER WP 17626, 2011) H.-W. Sinn

Target balances: German claim and GIPS debt Billion euros Billion euros 700 -700 April 2012 644 bn 600 -600 Bundesbank (left-hand scale) 500 -500 Feb. 2012 -671 bn 400 -400 GIPS 300 -300 (right-hand scale) 200 -200 March 2012 157 bn 100 -100 0 0 Netherlands (left-hand scale) -100 100 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 H.-W. Sinn

Target balances in the Eurozone (End of February 2012) Billion euros 600 547 300 GIIPS: -671 146 100 45 0 0 0 - 4 - 10 - 10 - 35 - 51 - 63 - 85 - 96 - 106 - 194 - 211 -300 Source: IMF, IFS; Deutsche Bundesbank; De Nederlandsche Bank; Banco de España; Banca d‘Italia. H.-W. Sinn

Balance-of-payments imbalances Credit and goods H.-W. Sinn

Balance-of-payments imbalances Credit flow stops H.-W. Sinn

Balance-of-payments imbalances Capital flight H.-W. Sinn

Balance-of-payments imbalances Capital flight H.-W. Sinn

Balance-of-payments imbalances Capital flight H.-W. Sinn

Balance-of-payments imbalances Reprinting the money H.-W. Sinn

What happened to the money flowing into the core? H.-W. Sinn

Why was it so easy to reprint the money? H.-W. Sinn

ECB collateral requirements Date Standard Until 24 October 2008 A- From 25 Oktober 2008 BBB- 3 May 2010 – 7 July 2011 Rating requirement waved for government bonds of Greece, Irleland and Portugal ELA credit Non-traded ABS created by commercial banks Company credit, national liability H.-W. Sinn

Germany and the Netherlands received for their current account surpluses in 2008-2012 only Target claims. H.-W. Sinn

Target claim and current account surplus % of GDP 35 Germany 30 25 Accumulated 20 current account 15 surplus 10 5 0 -5 Target claims -10 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 H.-W. Sinn

Target claim and current account surplus % of GDP 35 Germany 30 Netherlands 25 Accumulated 20 current account 15 surplus 10 5 0 -5 Target claims -10 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 H.-W. Sinn

4. The cost of the rescue operations H.-W. Sinn

The European bail-out funds (billion euros) Potential 250 IMF with preliminary promised by 188 EFSF ESM Until now 49 EFSM awarded 1270 (without German ESM 620 ECB) guarantees 2. rescue plan Greece (IMF) 18 exposure**** 2. rescue plan Greece (EU) 386 120 Portugal (IMF, EFSM, EFSF) 78 (without Capital Ireland (IMF, EFSM, EFSF) 63 15 80 contribution ECB) 1. rescue plan Greece (IMF) 30 80 30 77 10 1. rescue plan Greece (EU) 53*** 168 ECB purchases 212 22 212 2 of government bonds* 15*** 57 286 883 883 671 Target liabilities** 671 656 (GIPS and Italy) 1269 2153 * Data update: 17.5.2012 **** if GIPS countries and Italy default ** Data End of February 2012 H.-W. Sinn *** Credits disbursed by the end of 2011, unused resources to be released by the EFSF.

The European bail-out funds (billion euros) Netherland´s exposure**** German 5 exposure**** 17 2 35 5 15 1 80 3*** 12 10 168 60 22 2 15*** 57 141 286 in % of GDP (2011) 26 23 656 * Data update: 17.5.2012 **** if GIPS countries and Italy default ** Data End of February 2012 H.-W. Sinn *** Credits disbursed by the end of 2011, unused resources to be released by the EFSF.

Why is the Target credit a problem? • Fiscal rescue operation circumventing parliaments (Europe is no nation) • High risks for the core central banks • Eurobonds follow with necessity • Uniform interest despite differences in credit risk imply interest subsidies • Allocation of capital through a central planning agency rather than the capital market H.-W. Sinn

Really rescue? 1. Wrong asset prices are supported artificially, capital stays away. 2. ECB chases away the interbank credit. 3. Wrong goods prices and wages are supported artificially: Current account deficits are maintained. H.-W. Sinn

5. Two options for Europe H.-W. Sinn

Two options for Europe 1. Eurobonds and Target credit like today, political debt constraints H.-W. Sinn

Two options for Europe 1. Eurobonds and Target credit like today, political debt constraints 2. Liability, interest spreads, and settlement of Target balances with marketable assets H.-W. Sinn

Target and ISA balances % of GDP (of the previous year) 12 10 8 6 April 2012 4 21 bn dollars 2 USA 0.1% 0 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 H.-W. Sinn

Target and ISA balances % of GDP (of the previous year) 12 April 2012 10.1% 947 bn euros 10 8 Eurozone 6 April 2012 4 21 bn dollars 2 USA 0.1% 0 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 H.-W. Sinn

A crisis procedure: insurance with deductibles H.-W. Sinn

H.-W. Sinn

Liquidity crisis I • Tempory help (two years) Impending insolvency II • Piecemeal approach maturity by maturity • Other maturities cannot be called due (CAC) • Haircut up to 50% • Replacement bonds, secured up to 80% • Upper bound for guarantees and liquidity help: 30% of GDP III Full insolvency Exit from the Eurozone (my proposal) H.-W. Sinn

6. Conclusions • Balance-of-payment crisis caused by loss of competitiveness • The eurozone needs an internal realignment. • Target: 947 billion euro bailout program not sanctioned by any parliaments • ECB causes capital flight and maintains current-account imbalances. • US model is better, because it has harder budget constraints. • EEAG bankruptcy procedure for help and orderly default H.-W. Sinn

H.-W. Sinn

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.