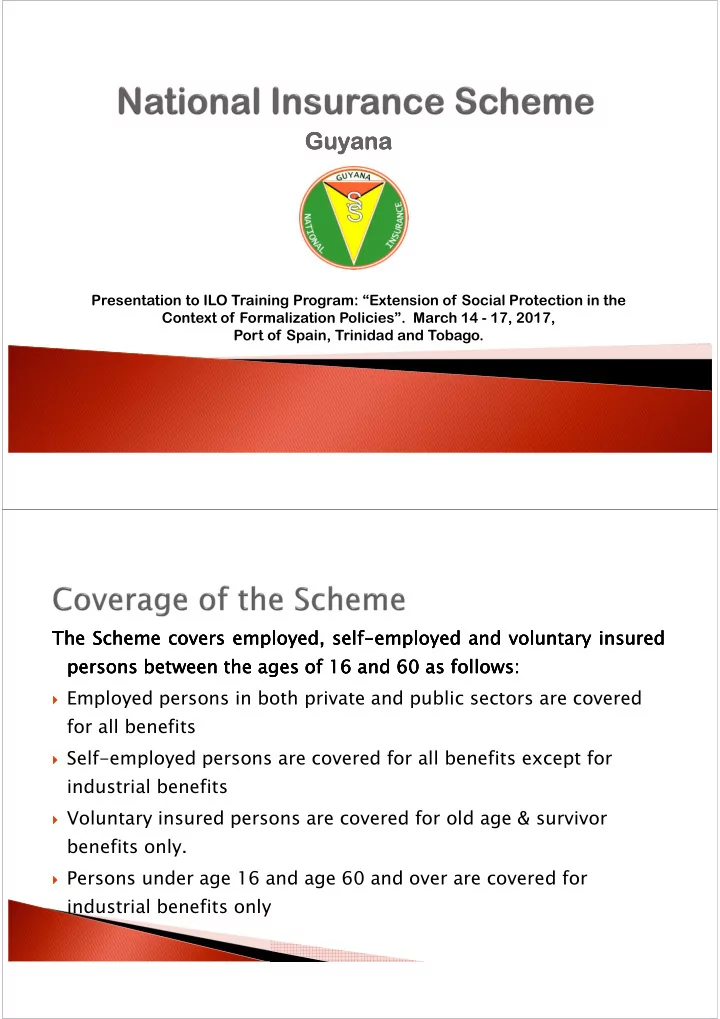

Guyana Guyana Guyana Guyana Presentation to ILO Training Program: “Extension of Social Protection in the Context of Formalization Policies”. March 14 - 17, 2017, Port of Spain, Trinidad and Tobago. The The Scheme Scheme covers covers employed, employed, self self- -employed employed and and voluntary voluntary insured insured The The Scheme Scheme covers covers employed, employed, self self - - employed employed and and voluntary voluntary insured insured persons between persons persons persons between between between the the the the ages ages of ages ages of of 16 of 16 16 16 and and and and 60 60 as 60 60 as as as follows follows follows follows: : : : � Employed persons in both private and public sectors are covered for all benefits � Self-employed persons are covered for all benefits except for industrial benefits � Voluntary insured persons are covered for old age & survivor benefits only. � Persons under age 16 and age 60 and over are covered for industrial benefits only

EMPLOYED PERSONS SELF - EMPLOYED EMPLOYERS New Entrants YEARS Active at Active at Total # Active at the New Total # New Total # the end of the end Registered end of year Registrants Registered Registrants Registered year of year All Ages Ages 16 - 59 2012 11,877 11,763 662,150 117,219 498 29,998 8,791 315 27,717 4,475 2013 10,622 10,545 672,772 118,548 486 30,484 9,017 338 28,055 6,507 2014 11,528 11,455 684,300 124,044 562 31,046 9,656 290 28,345 6,355 2015 12,017 11,951 696,317 128,487 772 31,818 10,002 379 28,724 5,441 2016 12,014 11,959 708,331 131,427 885 32,703 10,721 560 29,284 6,238 Contribution Contribution Rates Contribution Contribution Rates Rates Rates � Persons below 16 or over 60 years - 1.5% � Self-employed persons - 12.5% � Voluntary contributors - 9.3% � Employed Persons - 14% � 5.6% paid by the employee � 8.4% paid by the employer

The insurable earnings ceiling presented below came into effect from January 1 st 2017. Employed: � Weekly insurable earnings ceiling - $50,769 � Monthly insurable earnings ceiling - $220,000 Self-Employed � Minimum insurable earnings ceiling - $68,750 The monthly insurable earnings ceiling is approximately four times the current minimum wage in the public sector. Benefit payments are broken down into the following categories Benefit payments are broken down into the following categories: Benefit payments are broken down into the following categories Benefit payments are broken down into the following categories Long Term Benefits Short Term Benefits Industrial Benefits � Long Term Benefits ◦ Old Age Pension & Grant ◦ Invalidity Pension & Grant ◦ Survivors’ Pension & Grant ◦ Funeral Grant

� Short Term Benefits: ◦ Sickness Benefit ◦ Sickness Benefit Medical Care ◦ Maternity Benefit ◦ Maternity Grant ◦ Constant Attendance Benefit � Industrial Benefits: (Not paid to self-employed persons) ◦ Injury Benefit ◦ Disablement Benefit ◦ Industrial Death Benefit ◦ Injury Benefit Medical Care Benefit Number of Number of Current Type Pensioners Pensioners at Estimated the Minimum Monthly Amount OAP 34,641 22,065 1,127,023,477 INP 573 351 17,511,239 SUP 11,898 9,164 164,445,602 DTP 260 164 4,523,201 47,372 31,744 1,313,503,519

Evasion is significant among: � self-employed workers; � young and low paid workers; � domestic, casual and part-time workers; � small employers, employers in the informal sector; � employers who experience financial difficulties. � Employers evade the payment of contributions by falsely classifying their workers as self-employed persons. � Employers under reporting the earnings subject to contributions and exaggerating their allowances that do not attract contributions. � Employers delay to remit contributions at the statutory specified time. � Employers fail to remit contributions which they have with-held from their employees.

� Employers seek to reduce their labour costs. � Current consumption needs lead workers to evade paying contributions, particularly young workers who place a low value on future retirement consumption needs. � Reluctance to report a defaulting employer for the risk of loosing employment if anonymity is not maintained. � Evasion creates inequities between employers that meet their contribution obligations and those that do not, and similarly between employees who contribute and those who do not. � When evasion is due to an employer failing to remit contributions deducted from the wages of employees, the employees receive credits whether the scheme can recover the contributions from the defaulting employer or not. This causes delay in the award of the pension as investigations have to be conducted. � The scheme ultimately bears the risk.

� Arrangements could be made with the licensing agencies to restrict the issuance of licenses to persons who produce a N.I.S compliance certificate. � Every person doing business with the Revenue Authority must show NIS compliance � Inter-agency collaboration. � Legislative changes

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries