GASB Update Prepared by: Debbie Harper Brandon Young Ryan Domino - PDF document

GASB Update Prepared by: Debbie Harper Brandon Young Ryan Domino June 30, 2019 Fiscal Year GASB 83: Certain Asset Retirement Obligations GASB 88: Certain Disclosures Related to Debt, including Direct Borrowings and Direct

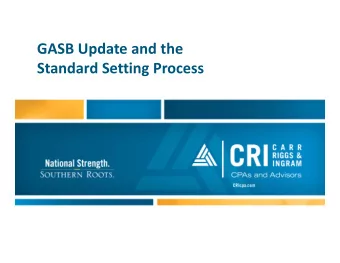

GASB Update Prepared by: Debbie Harper Brandon Young Ryan Domino • June 30, 2019 Fiscal Year – GASB 83: Certain Asset Retirement Obligations – GASB 88: Certain Disclosures Related to Debt, including Direct Borrowings and Direct Placements • June 30, 2020 Fiscal Year – GASB 89: Accounting for interest cost incurred before the end of a construction period – GASB 84: Fiduciary Activities • June 30, 2021 Fiscal Year – GASB 87: Leases www. lslcpas .com 1

On The Horizon Update • Financial Reporting Model – Public Hearings Held in March 2019 – Exposure Draft estimated for June 2020 • Conduit Debt Statement – Exposure Draft Issued April 2019 – Final Expected May 2019 • Deferred Compensation Statement – Added April 2019 www. lslcpas .com FISCAL YEAR ENDING JUNE 30, 2019 2

GASB 83 CERTAIN ASSET RETIREMENT OBLIGATIONS www. lslcpas .com Asset Retirement Obligation (AROs) • Legal obligation to perform future asset retirement activities related to tangible capital assets. • External laws, regulations, contracts, or court judgements together with occurrence of internal event that obligates a government. • Example: Decommissioning nuclear reactors; dismantling and removing sewage treatment plants; • Internal events: contamination, tangible asset that is required to be retired; abandoning a tangible capital asset before in operation. www. lslcpas .com 3

Financial Reporting • Recognize liability and deferred outflows for Asset Retirement Obligation in full accrual statements. • Amortize deferred outflow to expense over the estimated remaining life of the asset. www. lslcpas .com GASB 88 CERTAIN DISCLOSURES RELATED TO DEBT, INCLUDING DIRECT BORROWINGS AND DIRECT PLACEMENTS www. lslcpas .com 4

GASB 88 Certain Disclosures Related to Debt, including Direct Borrowings and Direct Placements • Clarifies which liabilities governments should include when disclosing debt information. • Defines debt and disclosures resulting from a contractual obligation with a set fixed amount and date. • Other disclosure requirements related to debt: – Unused credit lines – Assets pledged as collateral for debt – Terms related to significant events of default – Significant termination events – Significant subjective acceleration clauses www. lslcpas .com Clarifies which liabilities governments should include when disclosing debt information • Direct Borrowings – Loan Agreements with lenders • Direct Placements – Debt Security directly to an investor • Direct Borrowings and Direct Placements – Negotiated directly with the investor or lender – Not offered for public sale www. lslcpas .com 5

Defines debt and disclosures resulting from a contractual obligation with a set fixed amount and date • Fixed Amount – Variable Rate Interest – Capital Appreciation Bonds • Do not preclude the amount to be settled from being considered fixed. www. lslcpas .com Other disclosure requirements related to debt • Amounts of unused lines of credit • Assets pledged as collateral for debt • Terms specified in debt agreements related to significant – Events of default – Termination events – Subjective acceleration clauses • Separate direct borrows and direct placements from other debt www. lslcpas .com 6

GASB 88 Statement Example – Appendix C • Governmental Activities: – General obligation bonds, $12,530,000 – Notes from direct borrowing and direct placements, $941,918 • Business-type Activities: – Notes from direct borrowing, $70,400 – Pledged undeveloped lot for commercial use – Termination event changes timing of repayment to immediate if pledged revenues in the year are less than 120% of debt service due the following year – Acceleration clause; allowing the lender to accelerate payment of the entire principal amount if lender determines that a material adverse change occurs. • All notes contain an event of default = immediately due • Outstanding line of credit of $1,500,000 www. lslcpas .com Disclosure Example • Changes in long-term obligations for the year ended June 30, 20xx, are as follows: Balance at Balance at Due within July 1, 20xx Increases Decreases June 30, 20xx One Year Governmental activities: General obligation bonds $ 21,500,000 $ - $ 8,970,000 $ 12,530,000 $ 7,050,000 Notes from direct borrowings and direct placements 1,412,877 - 470,959 941,918 470,959 Total $ 22,912,877 $ - $ 9,440,959 $ 13,471,918 $ 7,520,959 Business-type activities: Notes from direct borrowings $ 76,800 $ - $ 6,400 $ 70,400 $ 6,400 Note that these debts are separate from other debts They do not have to be grouped together as shown here www. lslcpas .com 7

Consider Segregating on Face of Financial Statements LIABILITIES Current Liabilities: Accounts payable $ 5,864,825 Accrued liabilities 2,543,254 Accrued interest 1,325,465 Compensated absences due within one year 5,132,546 Claims payable due within one year 4,213,585 Long-term obligations due within one year 7,520,959 Total current liabilities $ 26,600,634 Non-current liabilities: Compensated absences due in more than one year $ 2,312,580 Claims payable due in more than one year 18,325,012 Net OPEB liability 10,564,258 Net pension liability 272,586,152 Long-term obligations due in more than one year 5,950,959 Total non-current liabilities $ 309,738,961 www. lslcpas .com Disclosure Example • The Government’s outstanding notes from direct borrowings and direct placements related to government activities of $941,918 contain a provision that in an event of default, outstanding amounts become immediately due if the Government is unable to make payment. www. lslcpas .com 8

Disclosure Example • The Government’s outstanding notes from direct borrowings relate to business-type activities of $70,400 are secured with collateral of an undeveloped lot zoned for commercial use. In addition they contain (1) a provision that in an event of default, the timing of repayment of outstanding amounts become immediately due if pledged revenues during the year are less than 120% of debt service coverage due in the following year and (2) a provision if that Government is unable to make payment, outstanding amounts are due immediately. As well as an acceleration clause that allows the lender to accelerate payment of the entire principal amount outstanding if the lender determines that a material adverse change occurs. www. lslcpas .com Disclosure Example • The Government also has an unused line of credit in the amount of $1,500,000. Debt service requirements on long-term debt at June 30, 20xx, are as follows: Show debt services schedules here as usual Show debt services schedules here as usual www. lslcpas .com 9

FISCAL YEAR ENDING JUNE 30, 2020 GASB 89 ACCOUNTING FOR INTEREST COST INCURRED BEFORE THE END OF A CONSTRUCTION PERIOD www. lslcpas .com 10

GASB 89 Accounting for Interest Cost Incurred before the End of a Construction Period • Changes accounting requirements for interest cost incurred before the end of a construction period. • Including such interest cost that previously was accounted for in accordance with GASB 62. • Resulting in interest cost incurred before the end of a construction period to be recognized as an expense and NOT to be included in the historical cost of a capital asset. www. lslcpas .com Accounting for Interest Cost • This is a prospective application. • Earlier application is encouraged. • CIP, interest cost incurred in the fiscal year of implementation should NOT be capitalized. www. lslcpas .com 11

Key take away • Include Prepaid Insurance when calculating gains/losses • Review Current Debt Disclosures for: – Unused credit lines – Assets pledged as collateral – Terms related to significant events if default – Significant termination events – Significant subjective acceleration clauses • Talk with all departments that currently capitalize interest costs – Prepare to stop capitalizing by 20/21 or stop now if project won’t be completed by then. www. lslcpas .com GASB 84 FIDUCIARY ACTIVITIES www. lslcpas .com 12

Fiduciary Activities Needed clarification • Large variances in the use of fiduciary funds in practice – Some reported as governmental funds – Some a fiduciary funds – Some not reported at all www. lslcpas .com Identifying Fiduciary Activities • Fiduciary Component Units – Meets Statement 14 as amended as a component unit AND is one of the following arrangements: An irrevocable trust of a pension plan An irrevocable trust of an OPEB plan Non employer assets accumulated for a pension plan Non employer assets accumulated for an OPEB plan www. lslcpas .com 13

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.