Functional and Physical Obsolescence in Property Tax Strategies for - PowerPoint PPT Presentation

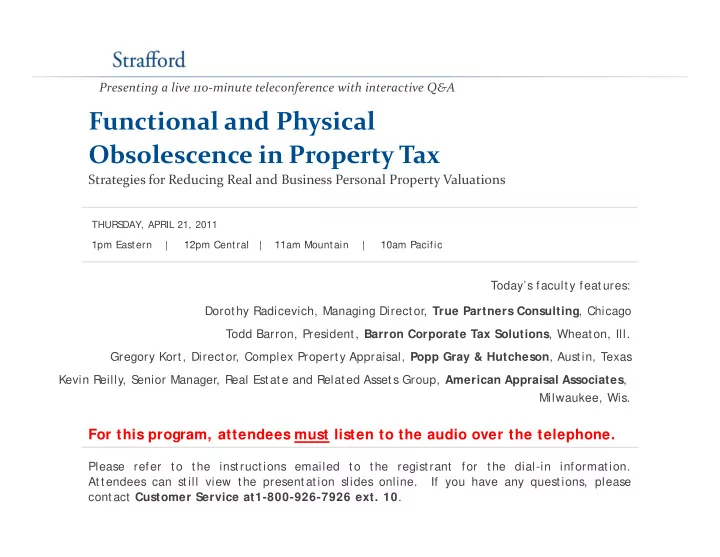

Presenting a live 110 minute teleconference with interactive Q&A Functional and Physical Obsolescence in Property Tax Strategies for Reducing Real and Business Personal Property Valuations THURS DAY, APRIL 21, 2011 1pm Eastern |

Presenting a live 110 ‐ minute teleconference with interactive Q&A Functional and Physical Obsolescence in Property Tax Strategies for Reducing Real and Business Personal Property Valuations THURS DAY, APRIL 21, 2011 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific Today’s faculty features: Dorothy Radicevich Managing Director True Partners Consulting Chicago Dorothy Radicevich, Managing Director, True Partners Consulting , Chicago Todd Barron, President, Barron Corporate Tax Solutions , Wheaton, Ill. Gregory Kort, Director, Complex Property Appraisal, Popp Gray & Hutcheson , Austin, Texas Kevin Reilly, S Kevin Reilly, S enior Manager, Real Estate and Related Assets Group, American Appraisal Associates , enior Manager, Real Estate and Related Assets Group, American Appraisal Associates , Milwaukee, Wis. For this program, attendees must listen to the audio over the telephone. Please refer to the instructions emailed to the registrant for the dial-in information. Attendees can still view the presentation slides online. If you have any questions, please contact Customer Service at1-800-926-7926 ext. 10 .

Conference Materials If you have not printed the conference materials for this program, please complete the following steps: • Click on the + sign next to “ Conference Materials” in the middle of the left- hand column on your screen hand column on your screen. • Click on the tab labeled “ Handouts” that appears, and there you will see a PDF of the slides for today's program. • Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open. • Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY Attendees must listen to the audio over the telephone . Attendees can still view the presentation slides online but there is no online audio for this program. Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10 . at 1 800 926 7926 ext. 10 .

Tips for Optimal Quality S S ound Qualit y d Q lit For this program, you must listen via the telephone by dialing 1-888-450-9970 and entering your PIN when prompted. There will be no sound over the web co connection. ect o . If you dialed in and have any difficulties during the call, press *0 for assistance. Y ou may also send us a chat or e-mail sound@straffordpub.com immediately so we can address the problem. Viewing Qualit y To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again press the F11 key again.

Functional and Physical Obsolescence F ti l d Ph i l Ob l in Property Tax Webinar April 21, 2011 Dorothy Radicevich, True Partners Consulting Todd Barron, Barron Corporate Tax S olutions dorothy.radicevich@ TPCtax.com tbarron@ barrontax.com Kevin Reilly, American Appraisal Gregory Kort, Popp Gray & Hutcheson kreilly@ american-appraisal.com greg@ property-tax.com

Today’s Program Overview Of Valuation Approaches S lide 7 – S lide 18 [Dorot hy Radicevich] Physical Deterioration And Functional Obsolescence S lide 19 – S lide 39 [Todd Barron] Calculating, Accounting For Physical Depreciation and S lide 40 – S lide 51 Functional Obsolescence [Gregory Kort and Kevin Reilly] Case S tudies On Making An Obsolescence-Based Argument S lide 52 – S lide 83 [Gregory Kort , Dorot hy Radicevich, Todd Barron, Kevin Reilly]

Dorothy Radicevich, True Partners Consulting OVERVIEW OF VALUATION OVERVIEW OF VALUATION APPROACHES

Si Significance Of Property Taxes ifi Of P T $215 billion $215 billion $215 billion $215 billion 8

9 Significance Of Property Taxes (Cont.) 35%

10 Significance Of Property Taxes (Cont.)

Wh What Is Fair Market Value? I F i M k V l ? S tates may define value differently Michigan: True cash value Texas: Appraised/ market value Indiana: True tax value Florida: Just value S S tates generally follow appraisal industry’s definition of FMV: tates generally follow appraisal industry s definition of FMV: The most probable price , as of a specified date , in cash, or in t erms of equivalent t o cash, or in ot her precisely revealed t erms, for which t he specified propert y right s should sell aft er reasonable exposure in a compet it ive market under all condit ions requisit e t o a fair sale, wit h t he buyer and seller each act ing prudent ly, knowledgeably, and for self-int erest , and assuming t hat neither is under undue duress . - Appraisal Institute 11

F i M Fair Market Value Concept k V l C Assessor’s principal duty is to determine FMV of property. FMV: What a willing buyer would pay to a willing seller in an open market k t Assessor can utilize three Approaches to value: Income Approach Market Approach Cost Approach FMV 12

I Income Approach To Value A h T V l Value of an investment property reflects the quality and quantity of income it is expected to generate income it is expected to generate over its life. Means of converting future benefits to present value Essential to the approach is the idea that income to be received in the that income to be received in the future is less valuable than income received today. 13

Sales Comparison (Market Value) Approach The sales comparison approach is a correlation of the subj ect property with comparable sales, property with comparable sales, adj usting those comparable sales to the characteristics of the subj ect property. Lack of data is bj t t L k f d t i maj or stumbling block in using this method. Many states do not y require statement of market value in purchase documents. 14

C Cost Approach A h The cost approach assumes value of an asset cannot exceed cost to reconstruct or replace it with another of like utility. Replacement cost new (RCN) establishes the highest amount a prudent investor would pay for an asset. To the extent assets are not new, the RCN is adj usted for losses in value due to physical deterioration and obsolescence. Obsolescence is a loss in value due to factors internal and external to an asset. 15

C Cost Approach (Cont.) A h (C ) Mass appraisal cost approach: Assessor trends taxpayer’s historical data by inflation factors in order to derive a value known as reproduction cost new. Inaccurate assumption is: Reproduction cost new = Replacement cost new Not accounting for excess cost and obsolescence g Assessor’s risk: The trends are not always current, so there is a lag between the assessor’s trends and the current market value. 16

C Cost Approach (Cont.) A h (C ) Reproduction Cost New Excess Capital Cost Replacement Cost New Physical det eriorat ion Physical det eriorat ion is a loss in value Physical Depreciation result ing from wear and t ear from use or exposure t o various t i F Functional Obsolescence ti l Ob l element s. Economic Obsolescence Asset Costs Fair Market Value 17

Ph Physical Deterioration i l D i i Expected on most equipment Not abnormal unless equipment is put to extensive use or misused misused Curable: Cost to correct deficiency is less than resulting economic benefit Incurable: Cost to correct deficiency is greater than resulting economic benefit Capitalized cost Capitalized cost —Depreciation = Book value (accountant) Depreciation = Book value (accountant) vs. Estimate of depreciation that directly relates to the Estimate of depreciation that directly relates to the actual loss in value the property has incurred (appraiser) 18

Todd Barron, Barron Corporate Tax Solutions PHYSICAL DETERIORATION PHYSICAL DETERIORATION AND FUNCTIONAL OBSOLESCENCE

Accrued Depreciation Accrued Depreciation Loss in value from all of the causes of deterioration and obsolescence Loss in value from all of the causes of deterioration and obsolescence (physical, functional and external) = The difference between an asset’s cost new and its fair market value Th diff b ’ d i f i k l 20

Accrued Depreciation (Cont.) Accrued Depreciation (Cont.) Why do we need to consider accrued depreciation in our analysis? Samuel Ichiye Hayakawa Samuel Ichiye Hayakawa Samuel Ichiye Hayakawa Samuel Ichiye Hayakawa 21

Accrued Depreciation (Cont.) Accrued Depreciation (Cont.) Cow one … Cow one … 22

Accrued Depreciation (Cont.) Accrued Depreciation (Cont.) Cow one … Cow one … is not is not Cow two. Cow two. Language in Thought & Action 23

24 Blower Being Assessed Blower Being Assessed

25 New Blower New Blower

Why accrued d depreciation? i i ? The asset being appraised is i d i not new. not new. 26

Accrued Depreciation (Cont.) Accrued Depreciation (Cont.) Question: What is “wrong” with the asset being assessed that would cause a buyer to pay less for it than for a new asset? 27

Physical Deterioration Physical Deterioration Loss in value due to physical wear and tear during usage and/or from the forces of nature 28

Physical Deterioration (Cont.) Physical Deterioration (Cont.) Causes and sources Age of asset A f t Usage over time Maintenance schedule Natural elements Other physical factors 29

Recommend

More recommend

Explore More Topics

Stay informed with curated content and fresh updates.