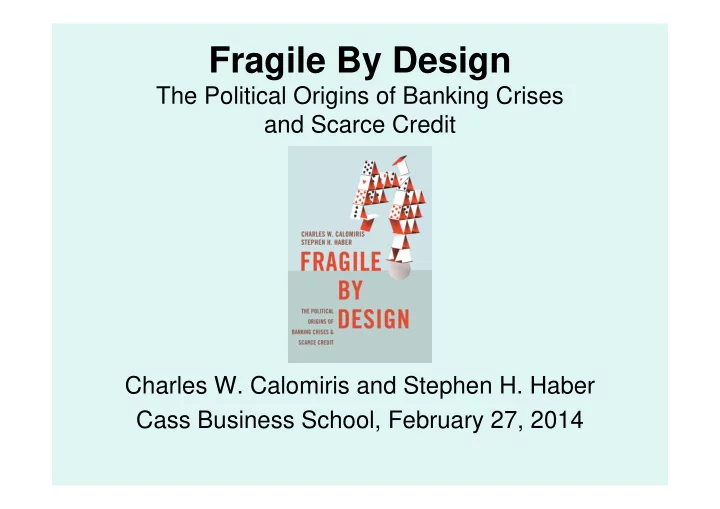

Fragile By Design The Political Origins of Banking Crises and Scarce Credit Charles W. Calomiris and Stephen H. Haber Cass Business School, February 27, 2014

Fact 1: Systemic Banking Crises are Endemic Figure 1 .1 The Frequency of System ic Banking Crises, 1 9 7 0 to 2 0 1 3 Tw o or More Crises Zero Crises 1 8 % 2 9 % One Crisis 5 3 %

Why do banking crises happen? A big shock? (it is true that shocks coincide with crises) Inherent fragility of banks? (bank liquidity transformation is unique; financial firms without opaque assets and short-term liabilities don’t have crises like banks) But these cannot be sufficient answers to the question because, in some times and places, crises are relatively absent despite big shocks and the presence of abundant bank credit.

Variation over Time and Space Some times were remarkably crisis-free worldwide (1874-1913) despite the presence of banks and abundant provision of bank credit. The period 1980-2013 is an unprecedented crisis pandemic. Even the Great Depression doesn’t come close to the current era. Some countries have been crisis-free: Canada, in spite of being a volatile commodity exporting country, has never suffered a severe banking crisis, while the US has suffered 17.

Is It Regulation? There is a lot of evidence in favor of that view, particularly for explaining how the combination of generous public safety nets for banks, without effective prudential regulation, leads to moral hazard and adverse selection problems. This also is corroborated by analysis showing that bank risk taking (e.g., leveraging) has increased dramatically over time. But that just begs the question : where did the wave of protection without adequate prudential regulation come from? Why have some countries avoided it?

Our View: Banks are Fragile By Design In many, but not all, countries, sub-groups form political alliances to use the banking system as a tool to extract public subsidies at the expense of other groups. This is accomplished through a process we call the Game of Bank Bargains , and it happens both in autocracies (where banking is a key part of what is sometimes called “crony networks”) and in democracies that are susceptible to populist capture. Banking systems are especially attractive as tools because it can be hard to identify the subsidies that flow from safety net policies, or favored access to credit (they are often not “on-budget”)

Credit scarcity has a similar explanation Bank credit has been shown to be very helpful for promoting growth and reducing inequality. The basic tools of banking have been known since the mid-18 th century. Yet many countries are credit supply-constrained. Abundant credit is rare because the access to credit is also a politically determined outcome in the Game of Bank Bargains.

Fact 2: Scarce credit is not randomly distributed either (note the relationship between stable democracies and credit provision) Figure 1 .2 Average Private Credit from Deposit Money Banks as a Percent of GDP, 1 9 9 0 to 2 0 1 0 , by W orld Bank I ncom e Classifications 180% 160% U.K. 140% High I ncom e Countries 120% Mean= 8 7 % Canada 100% 80% Upper Middle I ncom e Countries Mean= 3 8 % 60% U.S.A. Low er- Middle I ncom e Countries 40% Brazil Mean= 2 2 % Low I ncom e Countries Mexico Mean= 1 1 % 20% 0% Macao D. R. Congo Chad anzania Gambia Benin ogo Sudan emen Zambia Syria Bhutan Swaziland Cote d'Ivoire Sri Lanka hilippines ape Verde Honduras Morocco Gabon Botswana Suriname eru Iran ica unisia Chile Jordan Thailand q. Guinea Bahrain Greece Barbados S. Korea Belgium Italy Singapore Denmark Malta Iceland Ireland Luxembourg Japan Switz Myanmar ep. Malawi Haiti Mali Nepal Solomon Isl Senegal Fiji gypt ep. Uruguay ob. ortugal U.K. Costa R Cen. Afri. R P Dom. R rin. & T T E Y T P T P E C T Source: W orld Bank Financial Structure Database, Septem ber 2 0 1 2 update. Note: For reasons of readability, all country nam es not show n on X axis.

Our Framework 1. Banking systems are implicit partnerships between governments and private actors. 2. Partnership arise from strategic interactions (the “Game of Bank Bargains”), which operates according to the logic of politics, not the logic of efficiency. 3. It governs entry, competition, who gets credit, the pricing of credit, and the allocation of losses when banks fail. 4. Governments choose “bad” rules of the game because what the winning coalition wants can only be achieved under sub-optimal rules. 5. Who is in the controlling partnership varies across countries and within countries over time--because who is in the partnership and how much they can get from banks depends on each country’s system and rules.

How many crisis-free, abundant-credit countries? What attributes shared? Singapore Malta Hong Kong, China Australia Canada New Zealand Half of these are small island or city states (politically homogeneous). The other half are democracies that have a history of anti- populist constitutions.

How many high crisis, low credit countries are there--and what do they have in common? High crisis, especially low credit : Chad, Democratic Republic of the Congo. High crisis, low credit : Argentina, Bolivia Brazil, Cameroon, the Central African Republic, Colombia, Costa Rica, Ecuador, Kenya, Mexico, Nigeria, the Philippines, Turkey, and Uruguay. How many of these 16 countries have been stable democracies since 1970? Only 2: Colombia, Costa Rica .

What patterns are suggested? Non-democracies are systematically less likely to have stable and efficient banking systems. Being a democracy is not, per se, a solution to endemic banking crises.

Being a democracy is not the solution to endemic banking crises Num ber of System ic Banking Crises Since 1 8 4 0 , Canada and the USA 1 4 12 1 2 1 0 8 6 4 2 0 0 USA Canada

Canadian stability is not a symptom of lower levels of bank credit Figure 8 .1 Ratio of Com m ercial Bank Private Credit to GDP, Canada and the United States, 1 9 1 0 - 2 0 1 0 80% 70% Canada 60% Credit as Percent of GDP 50% 40% 30% USA 20% 10% 0% 1910 1913 1916 1919 1922 1925 1928 1931 1934 1937 1940 1943 1946 1949 1952 1955 1958 1961 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 Source: Historical Statistics of Canada, Bank of Canada Statistical Review, Bank of Canada Review; Federal Reserve, All Bank Statistics, Bureau of Economic Analysis, Banking and Monetary Statistics, FDI C website. Canada series excludes foreign lending.

Issues addressed by our country studies Why are stable, efficient banking systems so rare (why do political bargains need to create fragile banking systems)? Why do democracies generally do better? Why do some democracies do better than others? Through what mechanisms do political institutions affect banking system outcomes?

The key Constraints of the Game: All banking systems must address three property rights problems 1. Majority shareholders, minority shareholders, and depositors must be protected from expropriation by the government, or compensated for it. 2. Depositors and minority shareholders must be protected from expropriation by majority shareholders, or compensated for it. 3. Majority shareholders, depositors and minority shareholders must be protected from expropriation by debtors, or compensated for it.

Solving these problems requires government, but governments have inherent conflicts. 1. They simultaneously borrow from banks and regulate them. 2. They enforce debt contracts but need the political support of debtors. 3. They distribute losses in the event of bank failure, but they need the political support of depositors

Constraints => Fragility There are a finite number of feasible ways to arrange banking in a way that satisfies the property rights constraints and that serves the interests of the winning political coalition. That explains why banking systems often perform badly: they are performing as well as they can under the constraints defined by the allocation of political power, and the logic of property rights.

A basic taxonomy of regimes and banking systems Figure 1 .1 A Taxonom y of Regim es and Banking System s Regime Government Banker-Government Partnership Banking System Outcomes Chaos None None None No State Absolute Power None None Poverty Trap Centralized Rent Creating & Rent Narrow Credit, Strong State Sharing Network Locally Stable Autocracy Weakly Centralized Inflation Tax Sharing between "Float" Banking Mid-Strength State Oligarchy and Autocrat Local Oligarchies Little or No National Chartering Small, Fragmented Weak State Liberalism Competitive Banking with Taxation Broad Credit, Stable Powerful State Democracy Welfare State Moves Banks Limited role for Banks Mid-Strength State Populism out of the Line of Fire Politically Determined Credit Broad Credit, Unstable Powerful State

To show how political institutions and banking systems co-evolve we… Look at what actually happened in five countries from the late 17th century to the present The United Kingdom The United States Canada Mexico Brazil

Recommend

More recommend

Unleash a World of Digital Possibilities—Browse, Share, and Explore Content Without Boundaries