Corrections to Report Regarding Consolidated Capital Adequacy Ratio - PDF document

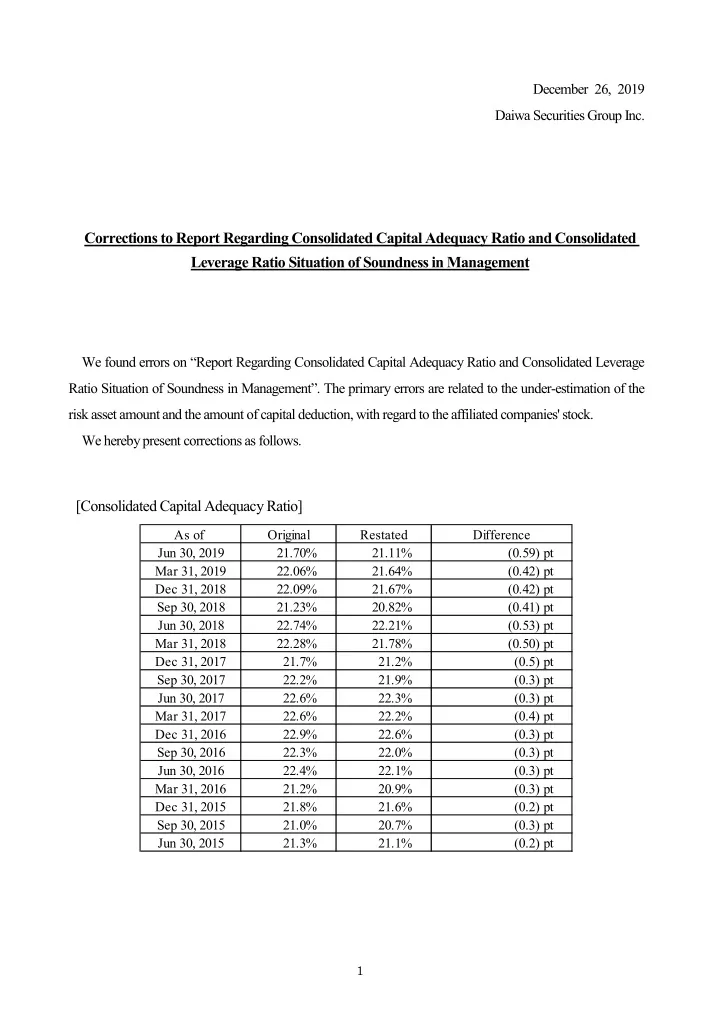

December 26, 2019 Daiwa Securities Group Inc. Corrections to Report Regarding Consolidated Capital Adequacy Ratio and Consolidated Leverage Ratio Situation of Soundness in Management We found errors on Report Regarding Consolidated Capital

[Restated] (Millions of yen , %) Basel III Group Consolidated Cross-referenced to template Items Quarter-End CC2 number Common Equity Tier 1 capital: regulatory adjustments (2) 133,513 8+9 Intangible assets other than mortgage-servicing rights (net of related tax liability) 8 Goodwill (net of related tax liability) 26,966 (e), (g) Investments in the capital of banking, financial and insurance entities that are outside the scope of 18 13,691 (a),(b),(c),(g) regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued share capital (amount above 10% threshold) Regulatory adjustments applied to Common Equity Tier 1 due to insufficient Additional Tier 1 and Tier 2 20,159 27 to cover deductions 28 167,880 Total regulatory adjustments to Common equity Tier 1 (b) Common Equity Tier 1 capital 29 1,074,541 Common Equity Tier 1 capital (CET1) ((a) - (b)) (c) Additional Tier 1 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 3,397 (a),(b),(c),(g) 39 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above 10% threshold) 42 16,762 Regulatory adjustments applied to Additional Tier 1 due to insufficient Tier 2 to cover deductions 43 20,159 Total regulatory adjustments to Additional Tier 1 capital (e) Tier 1 capital 1,074,541 45 Tier 1 capital ((c) + (f)) (g) Tier 2 capital: regulatory adjustments Investments in the capital and other TLAC liabilities of banking, financial and insurance entities that are 54 16,762 (a),(b),(c),(g) outside the scope of regulatory consolidation, where the bank does not own more than 10% of the issued common share capital of the entity (amount above 10% threshold) 16,762 57 Total regulatory adjustments to Tier 2 capital (i) Total capital 59 1,074,541 Total capital ((g) + (j)) (k) Risk weighted assets (5) 60 (l) 5,089,921 Total risk weighted assets Consolidated capital adequacy ratio 61 Common Equity Tier 1 (as a percentage of risk weighted assets) ((c) / (l)) 21.11% 62 21.11% Tier 1 (as a percentage of risk weighted assets) ((g) / (l)) 63 21.11% Total capital (as a percentage of risk weighted assets) ((k) / (l)) 64 3.02% CET1 specific buffer requirement 0.02% 66 of which: countercyclical buffer requirement 13.11% 68 CET1 available after meeting the minimum capital requirements Amounts below the thresholds for deduction (before risk weighting) (6) 72 110,839 (a),(b),(c),(g) Non-significant investments in the capital of other financials 73 Significant investments in the common stock of financials 69,807 (a),(b),(c),(g) 6

Qualitative Disclosure (Consolidated) 1. Reconciliation of regulatory capital to balance sheet CC2 : Reconciliation of regulatory capital to balance sheet [Original] (Millions of yen) Balance sheets as in Under regulatory scope of Cross-referenced to CC1 published statements consolidation Investment securities (g) 420,958 420,958 18, 39, 54, 72, 73 [Restated] (Millions of yen) Balance sheets as in Under regulatory scope of Cross-referenced to CC1 published statements consolidation Investment securities (g) 420,958 420,958 8, 18, 39, 54, 72, 73 Quantitative Disclosure (Consolidated) 1. Other quantitative disclosures OV1 : Overview of RWA [Original] (Millions of yen) Minimum capital Basel III RWA requirements template June March June March number 2019 2019 2019 2019 1 Credit risk (excluding counterparty credit risk) (CCR) 795,932 779,968 63,674 62,397 2 Of which standardized approach (SA) 576,658 581,678 46,132 46,534 16 Market risk 1,522,590 1,536,044 121,807 122,883 17 Of which standardized approach (SA) 898,308 838,957 71,864 67,116 18 Of which internal model approaches (IMM) 624,282 697,087 49,942 55,766 Amounts below the thresholds for deduction (subject to 250% 23 124,640 126,235 9,971 10,098 risk weight) 25 5,025,318 4,953,208 402,025 396,256 Total 7

[Restated] (Millions of yen) Minimum capital Basel III RWA requirements template June March June March number 2019 2019 2019 2019 1 803,669 816,153 64,293 65,291 Credit risk (excluding counterparty credit risk) (CCR) 2 584,394 617,863 46,751 49,428 Of which standardized approach (SA) 16 1,514,782 1,530,739 121,182 122,459 Market risk 17 890,462 838,622 71,237 67,089 Of which standardized approach (SA) 18 624,320 692,117 49,945 55,369 Of which internal model approaches (IMM) Amounts below the thresholds for deduction (subject to 250% 23 189,314 162,995 15,145 13,039 risk weight) 25 Total 5,089,921 5,020,849 407,193 401,667 MR2 : RWA flow statements of market risk exposures under an IMA [Original] (Millions of yen) VaR Stressed VaR IRC CRM Other Total RWA 1a RWA at previous quarter end 173,111 523,975 - - 697,087 1c Amounts of IMA at previous quarter end 44,992 142,079 - - 187,072 Change in 2 reporting Movement in risk levels 11,068 ▲ 5,256 - - 5,812 period 8a Amounts of IMA at end of reporting period 56,061 136,823 - - 192,884 8c RWA at end of reporting period 168,183 456,098 - - 624,282 [Restated] (Millions of yen) VaR Stressed VaR IRC CRM Other Total RWA 1a RWA at previous quarter end 174,078 518,038 - - 692,117 1c Amounts of IMA at previous quarter end 49,951 149,111 - - 199,062 Change in 2 reporting Movement in risk levels (299) (12,266) - - (12,566) period 8a Amounts of IMA at end of reporting period 49,651 136,844 - - 186,496 8c RWA at end of reporting period 168,261 456,058 - - 624,320 8

Consolidated Leverage Ratio 1. Composition of consolidated leverage ratio [Original] (Millions of yen , %) Basel III Basel III template template Items June 2019 March 2019 number (2) number (1) On-balance sheet exposures (1) 2 7 Common Equity Tier 1 capital: regulatory adjustments 151,577 146,287 3 Total on-balance sheet exposures (excluding derivatives and SFTs) (A) 13,128,327 11,894,900 Securities financing transaction exposures (3) 13 Netted amounts of cash payables and cash receivables of gross SFT assets 879,870 668,826 16 5 Total securities financing transaction exposures (C) 5,968,696 6,035,605 Capital and total exposures (5) 20 Tier 1 capital (E) 1,090,844 1,092,835 21 8 Total exposures (A)+(B)+(C)+(D) (F) 20,274,116 19,067,611 22 Leverage ratio on a consolidated basis (E) / (F) 5.38% 5.73% [Restated] (Millions of yen , %) Basel III Basel III template template Items June 2019 March 2019 number (2) number (1) On-balance sheet exposures (1) 2 7 Common Equity Tier 1 capital: regulatory adjustments 151,118 137,328 3 Total on-balance sheet exposures (excluding derivatives and SFTs) (A) 13,128,786 11,903,859 Securities financing transaction exposures (3) 13 Netted amounts of cash payables and cash receivables of gross SFT assets 1,338,135 1,070,592 16 5 Total securities financing transaction exposures (C) 5,510,431 5,633,839 Capital and total exposures (5) 20 Tier 1 capital (E) 1,074,541 1,086,889 21 8 Total exposures (A)+(B)+(C)+(D) (F) 19,816,310 18,674,804 22 Leverage ratio on a consolidated basis (E) / (F) 5.42% 5.82% 9

[As of March 31, 2019] Key Metrics (at consolidated group level) [Original] (Millions of yen , %) Basel III template March 2019 December 2018 September 2018 June 2018 March 2018 number Available capital (amounts) Common Equity Tier 1 1 1,092,835 1,085,262 1,111,476 1,134,950 1,142,340 (CET1) 2 1,092,835 1,085,262 1,111,476 1,134,950 1,142,340 Tier 1 3 1,092,835 1,085,262 1,111,476 1,134,950 1,142,340 Total capital Risk-weighted assets (amounts) Total risk-weighted assets 4 4,953,208 4,911,966 5,234,732 4,989,109 5,125,879 (RWA) Capital ratio 5 CET1 ratio (%) 22.06% 22.09% 21.23% 22.74% 22.28% 6 Tier 1 ratio (%) 22.06% 22.09% 21.23% 22.74% 22.28% 7 Total capital ratio (%) 22.06% 22.09% 21.23% 22.74% 22.28% Additional CET1 buffer requirements as a percentage of RWA CET1 available after 12 meeting the bank’s minimum 14.06% 14.09% 13.23% 14.74% 14.28% capital requirements (%) Leverage ratio Total leverage ratio 13 19,067,611 20,199,002 19,458,472 19,902,398 20,358,038 exposure measure Leverage ratio (%) including the impact of any 14 applicable temporary 5.73% 5.37% 5.71% 5.70% 5.61% exemption of central bank reserves 10

[Restated] (Millions of yen , %) Basel III template March 2019 December 2018 September 2018 June 2018 March 2018 number Available capital (amounts) Common Equity Tier 1 1 1,086,889 1,081,295 1,105,298 1,123,271 1,133,926 (CET1) 2 1,086,889 1,081,295 1,105,298 1,123,271 1,133,926 Tier 1 3 1,086,889 1,081,295 1,105,298 1,123,271 1,133,926 Total capital Risk-weighted assets (amounts) Total risk-weighted assets 4 5,020,849 4,988,639 5,307,882 5,055,974 5,205,812 (RWA) Capital ratio 5 CET1 ratio (%) 21.64% 21.67% 20.82% 22.21% 21.78% 6 Tier 1 ratio (%) 21.64% 21.67% 20.82% 22.21% 21.78% 7 Total capital ratio (%) 21.64% 21.67% 20.82% 22.21% 21.78% Additional CET1 buffer requirements as a percentage of RWA CET1 available after 12 meeting the bank’s minimum 13.64% 13.67% 12.82% 14.21% 13.78% capital requirements (%) Leverage ratio Total leverage ratio 13 18,674,804 20,092,466 19,916,960 19,884,503 20,356,302 exposure measure Leverage ratio (%) including the impact of any 14 applicable temporary 5.82% 5.38% 5.54% 5.64% 5.57% exemption of central bank reserves 11

Composition of Capital Disclosure CC1: Composition of Capital Disclosure [Original] (Millions of yen , %) Basel III Group Consolidated Cross-referenced to template Items Quarter-End CC2 number Common Equity Tier 1 capital: regulatory adjustments (2) 8+9 Intangible assets other than mortgage-servicing rights (net of related tax liability) 115,937 8 10,605 (e) Goodwill (net of related tax liability) Investments in the capital of banking, financial and insurance entities that are outside the scope of 18 11,653 (a),(b),(c),(g) regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued share capital (amount above 10% threshold) Regulatory adjustments applied to Common Equity Tier 1 due to insufficient Additional Tier 1 and Tier 2 18,258 27 to cover deductions 28 146,287 Total regulatory adjustments to Common equity Tier 1 (b) Common Equity Tier 1 capital 29 1,092,835 Common Equity Tier 1 capital (CET1) ((a) - (b)) (c) Additional Tier 1 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 39 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of 4,233 (a),(b),(c),(g) the issued common share capital of the entity (amount above 10% threshold) 42 14,025 Regulatory adjustments applied to Additional Tier 1 due to insufficient Tier 2 to cover deductions 43 18,258 Total regulatory adjustments to Additional Tier 1 capital (e) Tier 1 capital 1,092,835 45 Tier 1 capital ((c) + (f)) (g) Tier 2 capital: regulatory adjustments Investments in the capital and other TLAC liabilities of banking, financial and insurance entities that are 54 14,025 (a),(b),(c),(g) outside the scope of regulatory consolidation, where the bank does not own more than 10% of the issued common share capital of the entity (amount above 10% threshold) 14,025 57 Total regulatory adjustments to Tier 2 capital (i) Total capital 59 Total capital ((g) + (j)) (k) 1,092,835 Risk weighted assets (5) 4,953,208 60 Total risk weighted assets (l) Consolidated capital adequacy ratio 22.06% 61 Common Equity Tier 1 (as a percentage of risk weighted assets) ((c) / (l)) 62 Tier 1 (as a percentage of risk weighted assets) ((g) / (l)) 22.06% 63 22.06% Total capital (as a percentage of risk weighted assets) ((k) / (l)) 68 14.06% CET1 available after meeting the minimum capital requirements Amounts below the thresholds for deduction (before risk weighting) (6) 112,274 (a),(b),(c),(g) 72 Non-significant investments in the capital of other financials 73 43,961 (a),(b),(c),(g) Significant investments in the common stock of financials 12

[Restated] (Millions of yen , %) Basel III Group Consolidated Cross-referenced to template Items Quarter-End CC2 number Common Equity Tier 1 capital: regulatory adjustments (2) 120,913 8+9 Intangible assets other than mortgage-servicing rights (net of related tax liability) 8 Goodwill (net of related tax liability) 15,582 (e),(g) Investments in the capital of banking, financial and insurance entities that are outside the scope of 18 11,290 (a),(b),(c),(g) regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued share capital (amount above 10% threshold) Regulatory adjustments applied to Common Equity Tier 1 due to insufficient Additional Tier 1 and Tier 2 19,590 27 to cover deductions 152,232 28 Total regulatory adjustments to Common equity Tier 1 (b) Common Equity Tier 1 capital 29 1,086,889 Common Equity Tier 1 capital (CET1) ((a) - (b)) (c) Additional Tier 1 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 4,686 (a),(b),(c),(g) 39 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above 10% threshold) 42 14,904 Regulatory adjustments applied to Additional Tier 1 due to insufficient Tier 2 to cover deductions 43 19,590 Total regulatory adjustments to Additional Tier 1 capital (e) Tier 1 capital 45 1,086,889 Tier 1 capital ((c) + (f)) (g) Tier 2 capital: regulatory adjustments Investments in the capital and other TLAC liabilities of banking, financial and insurance entities that are 54 14,904 (a),(b),(c),(g) outside the scope of regulatory consolidation, where the bank does not own more than 10% of the issued common share capital of the entity (amount above 10% threshold) 14,904 57 Total regulatory adjustments to Tier 2 capital (i) Total capital 1,086,889 59 Total capital ((g) + (j)) (k) Risk weighted assets (5) 5,020,849 60 Total risk weighted assets (l) Consolidated capital adequacy ratio 21.64% 61 Common Equity Tier 1 (as a percentage of risk weighted assets) ((c) / (l)) 21.64% 62 Tier 1 (as a percentage of risk weighted assets) ((g) / (l)) 63 Total capital (as a percentage of risk weighted assets) ((k) / (l)) 21.64% 68 13.64% CET1 available after meeting the minimum capital requirements Amounts below the thresholds for deduction (before risk weighting) (6) 72 111,777 (a),(b),(c),(g) Non-significant investments in the capital of other financials 73 58,664 (a),(b),(c),(g) Significant investments in the common stock of financials 13

Qualitative Disclosure (Consolidated) 12. Reconciliation of regulatory capital to balance sheet CC2 – Reconciliation of regulatory capital to balance sheet [Original] (Millions of yen) Balance sheets as in Under regulatory scope of Cross-referenced to CC1 published statements consolidation Investment securities (g) 374,484 374,484 18, 39, 54, 72, 73 [Restated] (Millions of yen) Balance sheets as in Under regulatory scope of Cross-referenced to CC1 published statements consolidation Investment securities (g) 374,484 374,484 8, 18, 39, 54, 72, 73 Quantitative Disclosure (Consolidated) 2. Credit risk (excluding counterparty credit risk and securitization) A). Breakdown of exposures by geographical areas, industry and residual maturity [Original] 【 March 2019 】 (Millions of yen) Credit risk exposures Loans Securities Others Japan 6,088,175 837,642 820,760 4,429,773 Overseas 337,185 61,902 27,545 247,738 Total (by area) 6,425,360 899,544 848,305 4,677,511 Corporate 331,065 200,097 26,570 104,397 Others 595,997 11,590 263,137 321,269 Total (by industry) 6,425,360 899,544 848,305 4,677,511 Indeterminate 5,690,183 772,702 264,187 4,653,294 4,677,511 Total (by maturity) 6,425,360 899,544 848,305 14

[Restated] 【 March 2019 】 (Millions of yen) Credit risk exposures Loans Securities Others Japan 6,148,201 837,642 881,159 4,429,398 Overseas 335,514 61,902 25,874 247,738 Total (by area) 6,483,715 899,544 907,034 4,677,137 Corporate 330,691 200,097 26,570 104,023 Others 654,726 11,590 321,866 321,269 Total (by industry) 6,483,715 899,544 907,034 4,677,137 Indeterminate 5,748,538 772,702 322,916 4,652,919 4,677,137 Total (by maturity) 6,483,715 899,544 907,034 4. Other quantitative disclosures OV1 : Overview of RWA [Original] (Millions of yen) Minimum capital Basel III RWA requirements template March March March March number 2019 2018 2019 2018 1 Credit risk (excluding counterparty credit risk) (CCR) 779,968 903,175 62,397 72,254 2 Of which standardized approach (SA) 581,678 747,448 46,534 59,795 16 Market risk 1,536,044 1,461,548 122,883 116,923 17 838,957 860,281 67,116 68,822 Of which standardized approach (SA) 18 697,087 601,266 55,766 48,101 Of which internal model approaches (IMM) Amounts below the thresholds for deduction (subject to 250% 23 126,235 30,709 10,098 2,456 risk weight) 25 4,953,208 5,125,879 396,256 410,070 Total 15

[Restated] (Millions of yen) Minimum capital RWA Basel III requirements template March March March March number 2019 2018 2019 2018 1 Credit risk (excluding counterparty credit risk) (CCR) 816,153 903,084 65,292 72,246 2 Of which standardized approach (SA) 617,863 747,357 49,429 59,788 16 Market risk 1,530,739 1,457,444 122,459 116,595 17 Of which standardized approach (SA) 838,622 856,504 67,089 68,520 18 Of which internal model approaches (IMM) 692,117 600,940 55,369 48,075 Amounts below the thresholds for deduction (subject to 250% 23 162,995 114,837 13,040 9,187 risk weight) 25 5,020,849 5,205,812 401,667 416,465 Total [Original] (Millions of yen) Minimum capital Basel III RWA requirements template March December March December number 2019 2018 2019 2018 1 779,968 853,398 62,397 68,271 Credit risk (excluding counterparty credit risk) (CCR) 2 581,678 675,740 46,534 54,059 Of which standardized approach (SA) 16 1,536,044 1,334,804 122,883 106,784 Market risk 17 Of which standardized approach (SA) 838,957 847,602 67,116 67,808 18 Of which internal model approaches (IMM) 697,087 487,201 55,766 38,976 Amounts below the thresholds for deduction (subject to 250% 23 126,235 13,023 10,098 1,041 risk weight) 25 4,953,208 4,911,966 396,256 392,957 Total [Restated] (Millions of yen) Minimum capital Basel III RWA requirements template March December March December number 2019 2018 2019 2018 1 816,153 784,209 65,292 62,736 Credit risk (excluding counterparty credit risk) (CCR) 2 617,863 606,550 49,429 48,524 Of which standardized approach (SA) 16 1,530,739 1,336,484 122,459 106,918 Market risk 17 838,622 849,132 67,089 67,930 Of which standardized approach (SA) 18 692,117 487,352 55,369 38,988 Of which internal model approaches (IMM) Amounts below the thresholds for deduction (subject to 250% 23 162,995 157,205 13,040 12,576 risk weight) 25 5,020,849 4,988,639 401,667 399,091 Total 16

LI1: Differences between accounting and regulatory scopes of consolidation and mapping of financial statement categories with regulatory risk categories [Original] (Millions of yen) Carrying Carrying values as values Carrying values of items: reported in under scope published of regulatory Subject to Subject to Subject to the Subject to the Not subject to financial consolidation credit risk counterparty securitization market risk capital statements 1 credit risk 2 framework requirements framework framework framework or subject to deduction from capital Assets 39,229 39,048 - - 19,699 - 15 Accrued income 20,405,580 6,649,486 9,496,030 695,901 11,784,724 26,442 19 Total current assets Investments and other assets 437,100 436,999 - - 60,358 - 24 25 Investment securities 374,484 374,383 - - 22,374 - 721,126 605,088 - - 73,562 115,937 28 Total noncurrent assets 30 Total assets 21,126,706 7,254,576 9,496,030 695,901 11,858,286 142,379 [Restated] (Millions of yen) Carrying Carrying values as values Carrying values of items: reported in under scope published of regulatory Subject to Subject to Subject to the Subject to the Not subject to financial consolidation credit risk counterparty securitization market risk capital statements 1 credit risk 2 framework requirements framework framework framework or subject to deduction from capital Assets 39,229 39,018 - - 19,699 - 15 Accrued income 19 Total current assets 20,405,580 6,649,457 9,496,030 695,901 11,784,724 26,442 Investments and other assets 437,100 436,999 - - 60,682 4,976 24 25 Investment securities 374,484 374,383 - - 22,698 4,976 721,126 605,088 - - 73,886 120,913 28 Total noncurrent assets 30 Total assets 21,126,706 7,254,546 9,496,030 695,901 11,858,611 147,355 17

LI2: Main sources of differences between regulatory exposure amounts and carrying values in financial statements [Original] (Millions of yen) Items subject to: Credit risk Counterparty Securitization Market risk 1 credit risk framework framework framework Total 2 framework Asset carrying value amount under scope of regulatory 1 20,984,327 7,254,576 9,496,030 695,901 11,858,286 consolidation (as per template LI1) 3 Total net amount under regulatory scope of consolidation 9,501,678 7,254,303 418,343 695,901 1,452,715 1,452,715 10,709,038 7,132,430 1,417,085 706,807 12 Exposure amounts considered for regulatory purposes [Restated] (Millions of yen) Items subject to: Credit risk Counterparty Securitization Market risk 1 credit risk framework framework framework Total 2 framework Asset carrying value amount under scope of regulatory 1 20,979,351 7,254,546 9,496,030 695,901 11,858,611 consolidation (as per template LI1) 3 Total net amount under regulatory scope of consolidation 9,496,702 7,254,274 418,343 695,901 1,453,040 10,768,629 7,132,400 1,417,085 706,807 1,453,040 12 Exposure amounts considered for regulatory purposes 18

CR4: Standardized approach – credit risk exposure and Credit Risk Mitigation (CRM) effects [Original] (Millions of yen , %) Exposures before CCF and Exposures post-CCF and CRM CRM RWA RWA density On-balance Off-balance On-balance Off-balance Asset classes sheet amount sheet amount sheet amount sheet amount Non-Japanese public sector entities 2,760 - 2,760 - 624 22.61% 6 (excluding sovereign) Japan Finance Organization for 8 1,367 - 1,367 - 271 19.82% Municipalities (JFM) 9 Japanese government-sponsored entities 240,998 - 240,998 - 26,167 10.86% Three major local public corporations of 10 - - - - - - Japan 313,020 1,819 206,520 1,819 191,234 91.79% 12 Corporates 219,713 - 219,713 - 219,713 100.00% 21 Equities (excluding significant investments) 6,037,764 24,518 5,931,264 9,289 581,679 9.79% 22 Total [Restated] (Millions of yen , %) Exposures before CCF and Exposures post-CCF and CRM CRM RWA RWA density On-balance Off-balance On-balance Off-balance Asset classes sheet amount sheet amount sheet amount sheet amount Non-Japanese public sector entities 2,760 - 2,760 - 624 22.62% 6 (excluding sovereign) Japan Finance Organization for 1,367 - 1,367 - 271 19.86% 8 Municipalities (JFM) 240,998 - 240,998 - 26,167 10.85% 9 Japanese government-sponsored entities Three major local public corporations of 0 - 0 - 0 20.00% 10 Japan 12 Corporates 312,646 1,819 206,145 1,819 190,860 91.77% 21 Equities (excluding significant investments) 256,271 - 256,271 - 256,271 100.00% 22 Total 6,073,948 24,518 5,967,447 9,289 617,863 10.33% 19

CR5: Standardized approach – exposures by asset classes and risk weights [Original] (Millions of yen) Credit risk exposures (post-CCF and post-CRM) Risk weight Asset classes 100% 150% 250% 1250% Total 12 Corporates 184,857 - - - 208,339 219,713 - - - 219,713 21 Equities (excluding significant investments) 22 Total 423,848 624 - - 5,940,554 [Restated] (Millions of yen) Credit risk exposures (post-CCF and post-CRM) Risk weight Asset classes 100% 150% 250% 1250% Total 12 Corporates 184,483 - - - 207,965 256,271 - - - 256,271 21 Equities (excluding significant investments) 460,033 624 - - 5,976,738 22 Total 20

MR1 : Market risk under standardized approach [Original] (Millions of yen) RWA 1 Interest rate risk (general and specific) 621,669 120,708 2 Equity risk (general and specific) 3 Foreign exchange risk 74,858 838,957 9 Total [Restated] (Millions of yen) RWA 620,360 1 Interest rate risk (general and specific) 121,356 2 Equity risk (general and specific) 75,183 3 Foreign exchange risk 838,622 9 Total MR2 : RWA flow statements of market risk exposures under an IMA [Original] (Millions of yen) VaR Stressed VaR IRC CRM Other Total RWA 1a RWA at end of previous year 189,559 411,707 - - 601,266 1c Amounts of IMA at end of previous year 32,178 106,780 - - 138,959 Change in 2 reporting Movement in risk levels 8,479 48,791 - - 57,270 period 8a Amounts of IMA at end of reporting period 44,992 142,079 - - 187,072 8c RWA at end of reporting period 173,111 523,975 - - 697,087 21

[Restated] (Millions of yen) VaR Stressed VaR IRC CRM Other Total RWA 1a RWA at end of previous year 189,672 411,268 - - 600,940 1c Amounts of IMA at end of previous year 34,661 114,056 - - 148,717 Change in 2 reporting Movement in risk levels 10,954 48,546 - - 59,501 period 8a Amounts of IMA at end of reporting period 49,951 149,111 - - 199,062 8c RWA at end of reporting period 174,078 518,038 - - 692,117 [Original] (Millions of yen) VaR Stressed VaR IRC CRM Other Total RWA 1a RWA at previous quarter end 176,487 310,714 - - 487,201 1c Amounts of IMA at previous quarter end 64,703 196,079 - - 260,782 Change in 2 reporting Movement in risk levels ▲ 19,710 ▲ 53,999 - - ▲ 73,710 period 8a Amounts of IMA at end of reporting period 44,992 142,079 - - 187,072 8c RWA at end of reporting period 173,111 523,975 - - 697,087 [Restated] (Millions of yen) VaR Stressed VaR IRC CRM Other Total RWA 1a RWA at previous quarter end 176,519 310,833 - - 487,352 1c Amounts of IMA at previous quarter end 70,101 209,624 - - 279,726 Change in 2 reporting Movement in risk levels (20,150) (60,513) - - (80,664) period 8a Amounts of IMA at end of reporting period 49,951 149,111 - - 199,062 8c RWA at end of reporting period 174,078 518,038 - - 692,117 22

MR3 : IMA values for trading portfolios [Original] (Millions of yen) VaR (10 day 99%) – 15,076 1 Maximum value 5,850 2 Average value 3,969 4 Period end Stressed VaR (10 day 99%) 18,297 5 Maximum value 10,498 6 Average value 4,635 7 Minimum value 12,092 8 Period end [Restated] (Millions of yen) VaR (10 day 99%) – 9,110 1 Maximum value 4,947 2 Average value 3,996 4 Period end Stressed VaR (10 day 99%) 18,296 5 Maximum value 10,462 6 Average value 4,638 7 Minimum value 11,928 8 Period end IRRBB1 : Quantitative information on IRRBB [Original] (Millions of yen) ΔEVE March 2019 March 2018 1,092,835 1,142,340 8 Tier 1 capital 23

[Restated] (Millions of yen) ΔEVE March 2019 March 2018 1,086,889 1,133,926 8 Tier 1 capital CCyB1: Geographical distribution of credit exposures used in the countercyclical buffer [Original] (Millions of yen) Risk-weighted assets Bank-specific Geographical Countercyclical capital Countercyclical used in the computation countercyclical breakdown buffer rate buffer amount of the countercyclical capital buffer rate capital buffer 355 Total 1,778,639 0.02% [Restated] (Millions of yen) Risk-weighted assets Bank-specific Geographical Countercyclical capital Countercyclical used in the computation countercyclical breakdown buffer rate buffer amount of the countercyclical capital buffer rate capital buffer Total 1,855,761 0.02% 371 Consolidated Leverage Ratio 1. Composition of consolidated leverage ratio [Original] (Millions of yen , %) Basel III Basel III template template Items March 2019 March 2018 number (2) number (1) On-balance sheet exposures (1) 2 7 Common Equity Tier 1 capital: regulatory adjustments 146,287 115,303 3 Total on-balance sheet exposures (excluding derivatives and SFTs) (A) 11,894,900 11,544,374 Securities financing transaction exposures (3) 13 Netted amounts of cash payables and cash receivables of gross SFT assets 668,826 1,156,495 16 5 Total securities financing transaction exposures (C) 6,035,605 6,572,576 Capital and total exposures (5) 20 Tier 1 capital (E) 1,092,835 1,142,340 21 8 Total exposures (A)+(B)+(C)+(D) (F) 19,067,611 20,358,038 22 Leverage ratio on a consolidated basis (E) / (F) 5.73% 5.61% 24

[Restated] (Millions of yen , %) Basel III Basel III template template Items March 2019 March 2018 number (2) number (1) On-balance sheet exposures (1) 2 7 Common Equity Tier 1 capital: regulatory adjustments 137,328 117,039 3 Total on-balance sheet exposures (excluding derivatives and SFTs) (A) 11,903,859 11,542,638 Securities financing transaction exposures (3) 13 Netted amounts of cash payables and cash receivables of gross SFT assets 1,070,592 1,156,495 16 5 Total securities financing transaction exposures (C) 5,633,839 6,572,576 Capital and total exposures (5) 20 Tier 1 capital (E) 1,086,889 1,133,926 21 8 Total exposures (A)+(B)+(C)+(D) (F) 18,674,804 20,356,302 22 Leverage ratio on a consolidated basis (E) / (F) 5.82% 5.57% 25

[As of December 31, 2018] Key Metrics (at consolidated group level) [Original] (Millions of yen , %) Basel III template December 2018 September 2018 June 2018 March 2018 December 2017 number Available capital (amounts) Common Equity Tier 1 1 1,085,262 1,111,476 1,134,950 1,142,340 1,142,707 (CET1) 2 1,085,262 1,111,476 1,134,950 1,142,340 1,142,707 Tier 1 3 1,085,262 1,111,476 1,134,950 1,142,340 1,142,707 Total capital Risk-weighted assets (amounts) Total risk-weighted assets 4 4,911,966 5,234,732 4,989,109 5,125,879 5,257,936 (RWA) Capital ratio 5 CET1 ratio (%) 22.09% 21.23% 22.74% 22.28% 21.73% 6 Tier 1 ratio (%) 22.09% 21.23% 22.74% 22.28% 21.73% 7 Total capital ratio (%) 22.09% 21.23% 22.74% 22.28% 21.73% Additional CET1 buffer requirements as a percentage of RWA CET1 available after 12 meeting the bank’s minimum 14.09% 13.23% 14.74% 14.28% 13.73% capital requirements (%) Leverage ratio Total leverage ratio 13 20,199,002 19,458,472 19,902,398 20,358,038 20,987,142 exposure measure Leverage ratio (%) including the impact of any 14 applicable temporary 5.37% 5.71% 5.70% 5.61% 5.44% exemption of central bank reserves 26

[Restated] (Millions of yen , %) Basel III template December 2018 September 2018 June 2018 March 2018 December 2017 number Available capital (amounts) Common Equity Tier 1 1 1,081,295 1,105,298 1,123,271 1,133,926 1,131,024 (CET1) 2 1,081,295 1,105,298 1,123,271 1,133,926 1,131,024 Tier 1 3 1,081,295 1,105,298 1,123,271 1,133,926 1,131,024 Total capital Risk-weighted assets (amounts) Total risk-weighted assets 4 4,988,639 5,307,882 5,055,974 5,205,812 5,325,897 (RWA) Capital ratio 5 CET1 ratio (%) 21.67% 20.82% 22.21% 21.78% 21.23% 6 Tier 1 ratio (%) 21.67% 20.82% 22.21% 21.78% 21.23% 7 Total capital ratio (%) 21.67% 20.82% 22.21% 21.78% 21.23% Additional CET1 buffer requirements as a percentage of RWA CET1 available after 12 meeting the bank’s minimum 13.67% 12.82% 14.21% 13.78% 13.23% capital requirements (%) Leverage ratio Total leverage ratio 13 20,092,466 19,916,960 19,884,503 20,356,302 21,007,559 exposure measure Leverage ratio (%) including the impact of any 14 applicable temporary 5.38% 5.54% 5.64% 5.57% 5.38% exemption of central bank reserves 27

Composition of Capital Disclosure [Original] (Millions of yen , %) Basel III Group Consolidated template Items Quarter-End number Common Equity Tier 1 capital: regulatory adjustments (2) 113,894 8+9 Intangible assets other than mortgage-servicing rights (net of related tax liability) 8 11,017 Goodwill (net of related tax liability) Investments in the capital of banking, financial and insurance entities that are outside the scope of 15,972 18 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued share capital (amount above 10% threshold) Regulatory adjustments applied to Common Equity Tier 1 due to insufficient Additional Tier 1 and Tier 2 28,746 27 to cover deductions 28 159,044 Total regulatory adjustments to Common equity Tier 1 (b) Common Equity Tier 1 capital 1,085,262 29 Common Equity Tier 1 capital (CET1) ((a) - (b)) (c) Additional Tier 1 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 39 7,093 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above 10% threshold) 21,653 42 Regulatory adjustments applied to Additional Tier 1 due to insufficient Tier 2 to cover deductions 43 28,746 Total regulatory adjustments to Additional Tier 1 capital (e) Tier 1 capital 1,085,262 45 Tier 1 capital ((c) + (f)) (g) Tier 2 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 54 21,653 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above the 10% threshold) 57 21,653 Total regulatory adjustments to Tier 2 capital (i) Total capital 59 1,085,262 Total capital ((g) + (j)) (k) Risk weighted assets (5) 4,911,966 60 Total risk weighted assets (l) Consolidated capital adequacy ratio 22.09% 61 Common Equity Tier 1 (as a percentage of risk weighted assets) ((c) / (l)) 62 22.09% Tier 1 (as a percentage of risk weighted assets) ((g) / (l)) 22.09% 63 Total capital (as a percentage of risk weighted assets) ((k) / (l)) Amounts below the thresholds for deduction (before risk weighting) (6) 112,998 72 Non-significant investments in the capital of other financials 42,767 73 Significant investments in the common stock of financials 28

[Restated] (Millions of yen , %) Basel III Group Consolidated template Items Quarter-End number Common Equity Tier 1 capital: regulatory adjustments (2) 8+9 118,971 Intangible assets other than mortgage-servicing rights (net of related tax liability) 8 16,095 Goodwill (net of related tax liability) Investments in the capital of banking, financial and insurance entities that are outside the scope of 14,854 18 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued share capital (amount above 10% threshold) Regulatory adjustments applied to Common Equity Tier 1 due to insufficient Additional Tier 1 and Tier 2 27 28,755 to cover deductions 163,011 28 Total regulatory adjustments to Common equity Tier 1 (b) Common Equity Tier 1 capital 1,081,295 29 Common Equity Tier 1 capital (CET1) ((a) - (b)) (c) Additional Tier 1 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 7,332 39 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above 10% threshold) 42 21,422 Regulatory adjustments applied to Additional Tier 1 due to insufficient Tier 2 to cover deductions 43 28,755 Total regulatory adjustments to Additional Tier 1 capital (e) Tier 1 capital 1,081,295 45 Tier 1 capital ((c) + (f)) (g) Tier 2 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 21,422 54 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above the 10% threshold) 21,422 57 Total regulatory adjustments to Tier 2 capital (i) Total capital 59 1,081,295 Total capital ((g) + (j)) (k) Risk weighted assets (5) 60 4,988,639 Total risk weighted assets (l) Consolidated capital adequacy ratio 21.67% 61 Common Equity Tier 1 (as a percentage of risk weighted assets) ((c) / (l)) 62 21.67% Tier 1 (as a percentage of risk weighted assets) ((g) / (l)) 21.67% 63 Total capital (as a percentage of risk weighted assets) ((k) / (l)) Amounts below the thresholds for deduction (before risk weighting) (6) 112,490 72 Non-significant investments in the capital of other financials 73 57,672 Significant investments in the common stock of financials 29

Qualitative Disclosure (Consolidated) 1. The amount of each account in the balance sheets as in published statements and the reference number in composition of capital disclosure [Original] (Millions of yen) Reference number Balance sheets as in Under regulatory scope of in composition of published statements consolidation capital disclosure 378,567 18, 39, 54, 72, 73 Investment securities 378,567 [Restated] (Millions of yen) Reference number Balance sheets as in Under regulatory scope of in composition of published statements consolidation capital disclosure 378,567 8, 18, 39, 54, 72, 73 Investment securities 378,567 Quantitative Disclosure (Consolidated) 1. Other quantitative disclosures OV1 : Overview of RWA [Original] (Millions of yen) Minimum capital RWA Basel III requirements template number December September December September 2018 2018 2018 2018 1 853,398 884,040 68,271 70,723 Credit risk (excluding counterparty credit risk) (CCR) 2 675,740 703,163 54,059 56,253 Of which standardized approach (SA) 16 1,334,804 1,555,923 106,784 124,473 Market risk 17 847,602 940,241 67,808 75,219 Of which standardized approach (SA) 18 487,201 615,682 38,976 49,254 Of which internal model approaches (IMM) Amounts below the thresholds for deduction (subject to 250% 23 13,023 14,670 1,041 1,173 risk weight) 25 4,911,966 5,234,732 392,957 418,778 Total 30

[Restated] (Millions of yen) Minimum capital RWA Basel III requirements template number December September December September 2018 2018 2018 2018 1 Credit risk (excluding counterparty credit risk) (CCR) 784,209 813,622 62,736 65,089 2 Of which standardized approach (SA) 606,550 632,744 48,524 50,619 16 Market risk 1,336,484 1,556,021 106,918 124,481 17 Of which standardized approach (SA) 849,132 940,387 67,930 75,230 18 Of which internal model approaches (IMM) 487,352 615,634 38,988 49,250 Amounts below the thresholds for deduction (subject to 250% 23 157,205 158,140 12,576 12,651 risk weight) 25 4,988,639 5,307,882 399,091 424,630 Total MR2 : RWA flow statements of market risk exposures under an IMA [Original] (Millions of yen) VaR Stressed VaR IRC CRM Other Total RWA 1a RWA at previous quarter end 213,860 401,821 - - 615,682 Adjustments to RWA based on the regulatory consolidated capital at previous 5 3 - - 3 1b quarter end 1c Amounts of IMA at previous quarter end 46,196 159,363 - - 205,560 Change in 2 reporting Movement in risk levels ▲ 12,119 ▲ 59,962 - - ▲ 72,081 period 8a Amounts of IMA at end of reporting period 64,703 196,079 - - 260,782 Adjustments to RWA based on the regulatory consolidated capital at end of 3 2 - - 2 8b reporting period 8c RWA at end of reporting period 176,487 310,714 - - 487,201 31

[Restated] (Millions of yen) VaR Stressed VaR IRC CRM Other Total RWA 1a RWA at previous quarter end 213,852 401,781 - - 615,634 Adjustments to RWA based on the 1b regulatory consolidated capital at previous 4 2 - - 3 quarter end 1c Amounts of IMA at previous quarter end 48,048 164,694 - - 212,742 Change in 2 reporting Movement in risk levels (8,571) (51,748) - - (60,320) period 8a Amounts of IMA at end of reporting period 70,101 209,624 - - 279,726 Adjustments to RWA based on the 8b regulatory consolidated capital at end of 3 1 - - 2 reporting period 8c RWA at end of reporting period 176,519 310,833 - - 487,352 Consolidated Leverage Ratio 1. Composition of consolidated leverage ratio [Original] (Millions of yen) Basel Ⅲ Basel Ⅲ template template Items December 2018 September 2018 number (2) number (1) On-balance sheet exposures (1) 2 7 Common Equity Tier 1 capital: regulatory adjustments 159,044 167,029 3 Total on-balance sheet exposures (excluding derivatives and SFTs) (A) 12,351,286 11,391,951 Securities financing transaction exposures (3) Gross SFT assets (with no recognition of netting), after adjusting for sale 12 7,467,690 7,295,941 accounting transactions 13 Netted amounts of cash payables and cash receivables of gross SFT assets 2,093,412 1,718,286 16 5 Total securities financing transaction exposures (sum of lines 12 to 15) (C) 5,535,703 5,761,118 Capital and total exposures (5) 20 Tier 1 capital (E) 1,085,262 1,111,476 21 8 Total exposures (A)+(B)+(C)+(D) (F) 20,199,002 19,458,472 22 Basel III consolidated leverage ratio(E)/ (F) 5.37% 5.71% 32

[Restated] (Millions of yen) Basel Ⅲ Basel Ⅲ template template Items December 2018 September 2018 number (2) number (1) On-balance sheet exposures (1) 2 7 Common Equity Tier 1 capital: regulatory adjustments 141,588 149,142 3 Total on-balance sheet exposures (excluding derivatives and SFTs) (A) 12,368,742 11,409,838 Securities financing transaction exposures (3) Gross SFT assets (with no recognition of netting), after adjusting for sale 12 7,627,690 7,635,941 accounting transactions 13 Netted amounts of cash payables and cash receivables of gross SFT assets 2,377,404 1,617,685 16 5 Total securities financing transaction exposures (sum of lines 12 to 15) (C) 5,411,711 6,201,719 Capital and total exposures (5) 20 Tier 1 capital (E) 1,081,295 1,105,298 21 8 Total exposures (A)+(B)+(C)+(D) (F) 20,092,466 19,916,960 22 Basel III consolidated leverage ratio(E)/ (F) 5.38% 5.54% 33

[As of September 30, 2018] Key Metrics (at consolidated group level) [Original] (Millions of yen , %) Basel III template September 2018 June 2018 March 2018 December 2017 September 2017 number Available capital (amounts) Common Equity Tier 1 1 1,111,476 1,134,950 1,142,340 1,142,707 1,134,487 (CET1) 2 1,111,476 1,134,950 1,142,340 1,142,707 1,134,487 Tier 1 3 Total capital 1,111,476 1,134,950 1,142,340 1,142,707 1,134,487 Risk-weighted assets (amounts) Total risk-weighted assets 4 5,234,732 4,989,109 5,125,879 5,257,936 5,106,753 (RWA) Capital ratio 5 CET1 ratio (%) 21.23% 22.74% 22.28% 21.73% 22.21% 6 21.23% 22.74% 22.28% 21.73% 22.21% Tier 1 ratio (%) 7 Total capital ratio (%) 21.23% 22.74% 22.28% 21.73% 22.21% Additional CET1 buffer requirements as a percentage of RWA CET1 available after 12 meeting the bank’s minimum 13.23% 14.74% 14.28% 13.73% 14.21% capital requirements (%) Leverage ratio Total leverage ratio 13 19,458,472 19,902,398 20,358,038 20,987,142 19,524,574 exposure measure Leverage ratio (%) including the impact of any 14 applicable temporary 5.71% 5.70% 5.61% 5.44% 5.81% exemption of central bank reserves 34

[Restated] (Millions of yen , %) Basel III template September 2018 June 2018 March 2018 December 2017 September 2017 number Available capital (amounts) Common Equity Tier 1 1 1,105,298 1,123,271 1,133,926 1,131,024 1,140,647 (CET1) 2 1,105,298 1,123,271 1,133,926 1,131,024 1,140,647 Tier 1 3 Total capital 1,105,298 1,123,271 1,133,926 1,131,024 1,140,647 Risk-weighted assets (amounts) Total risk-weighted assets 4 5,307,882 5,055,974 5,205,812 5,325,897 5,188,403 (RWA) Capital ratio 5 CET1 ratio (%) 20.82% 22.21% 21.78% 21.23% 21.98% 6 20.82% 22.21% 21.78% 21.23% 21.98% Tier 1 ratio (%) 7 Total capital ratio (%) 20.82% 22.21% 21.78% 21.23% 21.98% Additional CET1 buffer requirements as a percentage of RWA CET1 available after 12 meeting the bank’s minimum 12.82% 14.21% 13.78% 13.23% 13.98% capital requirements (%) Leverage ratio Total leverage ratio 13 19,916,960 19,884,503 20,356,302 21,007,559 19,562,959 exposure measure Leverage ratio (%) including the impact of any 14 applicable temporary 5.54% 5.64% 5.57% 5.38% 5.83% exemption of central bank reserves 35

Composition of Capital Disclosure [Original] (Millions of yen , %) Basel III Group Consolidated template Items Quarter-End number Common Equity Tier 1 capital: regulatory adjustments (2) 110,803 8+9 Intangible assets other than mortgage-servicing rights (net of related tax liability) 8 10,740 Goodwill (net of related tax liability) Investments in the capital of banking, financial and insurance entities that are outside the scope of 24,703 18 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued share capital (amount above 10% threshold) Regulatory adjustments applied to Common Equity Tier 1 due to insufficient Additional Tier 1 and Tier 2 30,850 27 to cover deductions 28 167,029 Total regulatory adjustments to Common equity Tier 1 (b) Common Equity Tier 1 capital 1,111,476 29 Common Equity Tier 1 capital (CET1) ((a) - (b)) (c) Additional Tier 1 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 39 7,637 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above 10% threshold) 23,213 42 Regulatory adjustments applied to Additional Tier 1 due to insufficient Tier 2 to cover deductions 43 30,850 Total regulatory adjustments to Additional Tier 1 capital (e) Tier 1 capital 1,111,476 45 Tier 1 capital ((c) + (f)) (g) Tier 2 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 54 23,213 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above the 10% threshold) 57 23,213 Total regulatory adjustments to Tier 2 capital (i) Total capital 59 1,111,476 Total capital ((g) + (j)) (k) Risk weighted assets (5) 5,234,732 60 Total risk weighted assets (l) Consolidated capital adequacy ratio 21.23% 61 Common Equity Tier 1 (as a percentage of risk weighted assets) ((c) / (l)) 62 21.23% Tier 1 (as a percentage of risk weighted assets) ((g) / (l)) 21.23% 63 Total capital (as a percentage of risk weighted assets) ((k) / (l)) Amounts below the thresholds for deduction (before risk weighting) (6) 116,702 72 Non-significant investments in the capital of other financials 42,609 73 Significant investments in the common stock of financials 36

[Restated] (Millions of yen , %) Basel III Group Consolidated template Items Quarter-End number Common Equity Tier 1 capital: regulatory adjustments (2) 8+9 115,905 Intangible assets other than mortgage-servicing rights (net of related tax liability) 8 15,842 Goodwill (net of related tax liability) Investments in the capital of banking, financial and insurance entities that are outside the scope of 24,281 18 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued share capital (amount above 10% threshold) Regulatory adjustments applied to Common Equity Tier 1 due to insufficient Additional Tier 1 and Tier 2 27 32,348 to cover deductions 173,207 28 Total regulatory adjustments to Common equity Tier 1 (b) Common Equity Tier 1 capital 29 1,105,298 Common Equity Tier 1 capital (CET1) ((a) - (b)) (c) Additional Tier 1 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 8,284 39 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above 10% threshold) 42 24,064 Regulatory adjustments applied to Additional Tier 1 due to insufficient Tier 2 to cover deductions 32,348 43 Total regulatory adjustments to Additional Tier 1 capital (e) Tier 1 capital 1,105,298 45 Tier 1 capital ((c) + (f)) (g) Tier 2 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 24,064 54 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above the 10% threshold) 24,064 57 Total regulatory adjustments to Tier 2 capital (i) Total capital 1,105,298 59 Total capital ((g) + (j)) (k) Risk weighted assets (5) 5,307,882 60 Total risk weighted assets (l) Consolidated capital adequacy ratio 61 20.82% Common Equity Tier 1 (as a percentage of risk weighted assets) ((c) / (l)) 20.82% 62 Tier 1 (as a percentage of risk weighted assets) ((g) / (l)) 63 20.82% Total capital (as a percentage of risk weighted assets) ((k) / (l)) Amounts below the thresholds for deduction (before risk weighting) (6) 116,192 72 Non-significant investments in the capital of other financials 57,388 73 Significant investments in the common stock of financials 37

Qualitative Disclosure (Consolidated) 2. The amount of each account in the balance sheets as in published statements and the reference number in composition of capital disclosure [Original] (Millions of yen) Reference number Balance sheets as in Under regulatory scope of in composition of published statements consolidation capital disclosure 384,689 18, 39, 54, 72, 73 Investment securities 384,689 [Restated] (Millions of yen) Reference number Balance sheets as in Under regulatory scope of in composition of published statements consolidation capital disclosure 384,689 8, 18, 39, 54, 72, 73 Investment securities 384,689 Quantitative Disclosure (Consolidated) 3. Other quantitative disclosures OV1 : Overview of RWA [Original] (Millions of yen) Minimum capital RWA Basel III requirements template number September September September September 2018 2017 2018 2017 1 Credit risk (excluding counterparty credit risk) (CCR) 884,040 70,723 2 Of which standardized approach (SA) 703,163 56,253 16 Market risk 1,555,923 124,473 17 Of which standardized approach (SA) 940,241 75,219 18 Of which internal model approaches (IMM) 615,682 49,254 Amounts below the thresholds for deduction (subject to 250% 23 14,670 1,173 risk weight) 25 5,234,732 418,778 Total 38

[Restated] (Millions of yen) Minimum capital RWA Basel III requirements template number September September September September 2018 2017 2018 2017 1 Credit risk (excluding counterparty credit risk) (CCR) 813,622 65,089 2 Of which standardized approach (SA) 632,744 50,619 16 Market risk 1,556,021 124,481 17 Of which standardized approach (SA) 940,387 75,230 18 Of which internal model approaches (IMM) 615,634 49,250 Amounts below the thresholds for deduction (subject to 250% 23 158,140 12,651 risk weight) 25 5,307,882 424,630 Total [Original] (Millions of yen) Minimum capital RWA Basel III requirements template number September June September June 2018 2018 2018 2018 1 884,040 903,494 70,723 72,279 Credit risk (excluding counterparty credit risk) (CCR) 2 703,163 722,141 56,253 57,771 Of which standardized approach (SA) 16 1,555,923 1,418,973 124,473 113,517 Market risk 17 940,241 903,919 75,219 72,313 Of which standardized approach (SA) 18 615,682 515,053 49,254 41,204 Of which internal model approaches (IMM) Amounts below the thresholds for deduction (subject to 250% 23 14,670 11,397 1,173 911 risk weight) 25 5,234,732 4,989,109 418,778 399,128 Total [Restated] (Millions of yen) Minimum capital RWA Basel III requirements template number September June September June 2018 2018 2018 2018 1 813,622 850,303 65,089 68,024 Credit risk (excluding counterparty credit risk) (CCR) 2 632,744 668,950 50,619 53,516 Of which standardized approach (SA) 16 1,556,021 1,412,401 124,481 112,992 Market risk 17 940,387 897,386 75,230 71,790 Of which standardized approach (SA) 18 615,634 515,015 49,250 41,201 Of which internal model approaches (IMM) Amounts below the thresholds for deduction (subject to 250% 23 158,140 138,025 12,651 11,042 risk weight) 25 5,307,882 5,055,974 424,630 404,477 Total 39

CR4: Standardized approach – credit risk exposure and Credit Risk Mitigation (CRM) effects [Original] (Millions of yen , %) Exposures before CCF and Exposures post-CCF and CRM CRM RWA RWA density On-balance Off-balance On-balance Off-balance Asset classes sheet amount sheet amount sheet amount sheet amount 385,294 - 385,294 - 7,894 2.05% 3 Non-Japanese sovereign and central bank Non-Japanese public sector entities 2,480 - 2,480 - 557 22.46% 6 (excluding sovereign) Three major local public corporations of - - - - - - 10 Japan Financial institutions and securities firms 545,428 19,010 545,428 3,802 120,716 21.98% 11 268,240 1,861 210,122 1,861 187,088 88.26% 12 Corporates Past due exposures for three months or 559 - 559 - 838 149.91% 16 more(excluding residential mortgage loans) 21 Equities (excluding significant investments) 269,948 - 269,948 - 338,526 125.40% 22 Total 5,652,785 20,871 5,594,667 5,663 703,163 12.56% 40

[Restated] (Millions of yen , %) Exposures before CCF and Exposures post-CCF and CRM CRM RWA RWA density On-balance Off-balance On-balance Off-balance Asset classes sheet amount sheet amount sheet amount sheet amount 3 Non-Japanese sovereign and central bank 385,294 - 385,294 - 7,894 2.04% Non-Japanese public sector entities 2,480 - 2,480 - 557 22.48% 6 (excluding sovereign) Three major local public corporations of 0 - 0 - 0 20.00% 10 Japan Financial institutions and securities firms 545,428 19,010 545,428 3,802 120,716 21.97% 11 268,236 1,861 210,118 1,861 187,083 88.25% 12 Corporates Past due exposures for three months or 559 - 559 - 838 150.00% 16 more(excluding residential mortgage loans) 21 Equities (excluding significant investments) 268,111 - 268,111 - 268,111 100.00% 22 Total 5,650,943 20,871 5,592,825 5,663 632,744 11.30% CR5: Standardized approach – exposures by asset classes and risk weights [Original] (Millions of yen) Credit risk exposures (post-CCF and post-CRM) Risk weight Asset classes 100% 150% 250% 1250% Total 176,640 - - - 211,984 12 Corporates 21 Equities (excluding significant investments) 224,229 - 45,718 - 269,948 421,534 559 45,718 - 5,600,330 22 Total 41

[Restated] (Millions of yen) Credit risk exposures (post-CCF and post-CRM) Risk weight Asset classes 100% 150% 250% 1250% Total 176,636 - - - 211,980 12 Corporates 268,111 - - - 268,111 21 Equities (excluding significant investments) 22 Total 465,411 559 - - 5,598,489 MR1 : Market risk under standardized approach [Original] (Millions of yen) RWA 638,388 1 Interest rate risk (general and specific) 209,630 2 Equity risk (general and specific) 70,103 3 Foreign exchange risk 940,241 9 Total [Restated] (Millions of yen) RWA 636,913 1 Interest rate risk (general and specific) 2 Equity risk (general and specific) 202,212 79,142 3 Foreign exchange risk 9 Total 940,387 42

MR2 : RWA flow statements of market risk exposures under an IMA [Original] (Millions of yen) VaR Stressed VaR IRC CRM Other Total RWA 1a RWA at previous quarter end 176,889 338,164 - - 515,053 Adjustments to RWA based on the regulatory consolidated capital at previous 7 6 - - 6 1b quarter end 1c Amounts of IMA at previous quarter end 24,703 60,454 - - 85,158 Change in 2 reporting Movement in risk levels 21,493 98,908 - - 120,402 period 8a Amounts of IMA at end of reporting period 46,196 159,363 - - 205,560 Adjustments to RWA based on the 8b regulatory consolidated capital at end of 5 3 - - 3 reporting period 8c RWA at end of reporting period 213,860 401,821 - - 615,682 [Restated] (Millions of yen) VaR Stressed VaR IRC CRM Other Total RWA 1a RWA at previous quarter end 176,552 338,463 - - 515,015 Adjustments to RWA based on the 1b regulatory consolidated capital at previous 6 5 - - 5 quarter end 1c Amounts of IMA at previous quarter end 27,206 67,506 - - 94,712 Change in 2 reporting Movement in risk levels 20,841 97,188 - - 118,030 period 8a Amounts of IMA at end of reporting period 48,048 164,694 - - 212,742 Adjustments to RWA based on the regulatory consolidated capital at end of 4 2 - - 3 8b reporting period 8c RWA at end of reporting period 213,852 401,781 - - 615,634 43

MR3 : IMA values for trading portfolios [Original] (Millions of yen) VaR (10 day 99%) – 8,495 1 Maximum value 4,700 2 Average value 1,743 3 Minimum value 3,695 4 Period end Stressed VaR (10 day 99%) 17,812 5 Maximum value 9,532 6 Average value 4,346 7 Minimum value 12,749 8 Period end [Restated] (Millions of yen) VaR (10 day 99%) – 8,668 1 Maximum value 4,845 2 Average value 1,834 3 Minimum value 3,843 4 Period end Stressed VaR (10 day 99%) 18,296 5 Maximum value 9,953 6 Average value 4,653 7 Minimum value 13,175 8 Period end IRRBB1 : Quantitative information on IRRBB [Original] (Millions of yen) ΔEVE September September 2018 2017 1,111,476 1,134,487 8 Tier 1 capital 44

[Restated] (Millions of yen) ΔEVE September September 2018 2017 1,105,298 1,140,647 8 Tier 1 capital Consolidated Leverage Ratio 1. Composition of consolidated leverage ratio [Original] (Millions of yen) Basel Ⅲ Basel Ⅲ template template Items September 2018 September 2017 number (2) number (1) On-balance sheet exposures (1) 2 7 Common Equity Tier 1 capital: regulatory adjustments 167,029 147,784 3 Total on-balance sheet exposures (excluding derivatives and SFTs) (A) 11,391,951 11,718,430 Securities financing transaction exposures (3) Gross SFT assets (with no recognition of netting), after adjusting for sale 12 7,295,941 6,753,882 accounting transactions 13 Netted amounts of cash payables and cash receivables of gross SFT assets 1,718,286 1,423,824 16 5 Total securities financing transaction exposures (sum of lines 12 to 15) (C) 5,761,118 5,489,913 Capital and total exposures (5) 20 Tier 1 capital (E) 1,111,476 1,134,487 21 8 Total exposures (A)+(B)+(C)+(D) (F) 19,458,472 19,524,574 22 Basel III consolidated leverage ratio(E)/ (F) 5.71% 5.81% [Restated] (Millions of yen) Basel Ⅲ Basel Ⅲ template template Items September 2018 September 2017 number (2) number (1) On-balance sheet exposures (1) 2 7 Common Equity Tier 1 capital: regulatory adjustments 149,142 109,399 3 Total on-balance sheet exposures (excluding derivatives and SFTs) (A) 11,409,838 11,756,815 Securities financing transaction exposures (3) Gross SFT assets (with no recognition of netting), after adjusting for sale 12 7,635,941 6,753,882 accounting transactions 13 Netted amounts of cash payables and cash receivables of gross SFT assets 1,617,685 1,423,824 16 5 Total securities financing transaction exposures (sum of lines 12 to 15) (C) 6,201,719 5,489,913 Capital and total exposures (5) 20 Tier 1 capital (E) 1,105,298 1,140,647 21 8 Total exposures (A)+(B)+(C)+(D) (F) 19,916,960 19,562,959 22 Basel III consolidated leverage ratio(E)/ (F) 5.54% 5.83% 45

[As of June 30, 2018] Key Metrics (at consolidated group level) [Original] (Millions of yen , %) Basel III template June 2018 March 2018 December 2017 September 2017 June 2017 number Available capital (amounts) Common Equity Tier 1 1 1,134,950 1,142,340 1,142,707 1,134,487 1,140,227 (CET1) 2 1,134,950 1,142,340 1,142,707 1,134,487 1,140,227 Tier 1 3 1,134,950 1,142,340 1,142,707 1,134,487 1,140,227 Total capital Risk-weighted assets (amounts) Total risk-weighted assets 4 4,989,109 5,125,879 5,257,936 5,106,753 5,043,690 (RWA) Capital ratio 5 CET1 ratio (%) 22.74% 22.28% 21.73% 22.21% 22.60% 6 Tier 1 ratio (%) 22.74% 22.28% 21.73% 22.21% 22.60% 7 Total capital ratio (%) 22.74% 22.28% 21.73% 22.21% 22.60% Additional CET1 buffer requirements as a percentage of RWA CET1 available after 12 meeting the bank’s minimum 14.74% 14.28% 13.73% 14.21% 14.60% capital requirements (%) Leverage ratio Total leverage ratio 13 19,902,398 20,358,038 20,987,142 19,524,574 18,979,308 exposure measure Leverage ratio (%) including the impact of any 14 applicable temporary 5.70% 5.61% 5.44% 5.81% 6.00% exemption of central bank reserves 46

[Restated] (Millions of yen , %) Basel III template June 2018 March 2018 December 2017 September 2017 June 2017 number Available capital (amounts) Common Equity Tier 1 1 1,123,271 1,133,926 1,131,024 1,140,647 1,143,722 (CET1) 2 1,123,271 1,133,926 1,131,024 1,140,647 1,143,722 Tier 1 3 1,123,271 1,133,926 1,131,024 1,140,647 1,143,722 Total capital Risk-weighted assets (amounts) Total risk-weighted assets 4 5,055,974 5,205,812 5,325,897 5,188,403 5,110,915 (RWA) Capital ratio 5 CET1 ratio (%) 22.21% 21.78% 21.23% 21.98% 22.37% 6 Tier 1 ratio (%) 22.21% 21.78% 21.23% 21.98% 22.37% 7 Total capital ratio (%) 22.21% 21.78% 21.23% 21.98% 22.37% Additional CET1 buffer requirements as a percentage of RWA CET1 available after 12 meeting the bank’s minimum 14.21% 13.78% 13.23% 13.98% 14.37% capital requirements (%) Leverage ratio Total leverage ratio 13 19,884,503 20,356,302 21,007,559 19,562,959 18,998,109 exposure measure Leverage ratio (%) including the impact of any 14 applicable temporary 5.64% 5.57% 5.38% 5.83% 6.02% exemption of central bank reserves 47

Composition of Capital Disclosure [Original] (Millions of yen , %) Basel III Group Consolidated template Items Quarter-End number Common Equity Tier 1 capital: regulatory adjustments (2) 107,752 8+9 Intangible assets other than mortgage-servicing rights (net of related tax liability) 8 10,977 Goodwill (net of related tax liability) Investments in the capital of banking, financial and insurance entities that are outside the scope of 16,913 18 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued share capital (amount above 10% threshold) Regulatory adjustments applied to Common Equity Tier 1 due to insufficient Additional Tier 1 and Tier 2 27 22,543 to cover deductions 28 147,794 Total regulatory adjustments to Common equity Tier 1 (b) Common Equity Tier 1 capital 1,134,950 29 Common Equity Tier 1 capital (CET1) ((a) - (b)) (c) Additional Tier 1 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 3,653 39 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above 10% threshold) 42 18,889 Regulatory adjustments applied to Additional Tier 1 due to insufficient Tier 2 to cover deductions 43 22,543 Total regulatory adjustments to Additional Tier 1 capital (e) Tier 1 capital 1,134,950 45 Tier 1 capital ((c) + (f)) (g) Tier 2 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 18,889 54 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above the 10% threshold) 18,889 57 Total regulatory adjustments to Tier 2 capital (i) Total capital 1,134,950 59 Total capital ((g) + (j)) (k) Risk weighted assets (5) 60 4,989,109 Total risk weighted assets (l) Consolidated capital adequacy ratio 61 22.74% Common Equity Tier 1 (as a percentage of risk weighted assets) ((c) / (l)) 22.74% 62 Tier 1 (as a percentage of risk weighted assets) ((g) / (l)) 63 22.74% Total capital (as a percentage of risk weighted assets) ((k) / (l)) Amounts below the thresholds for deduction (before risk weighting) (6) 72 117,440 Non-significant investments in the capital of other financials 36,826 73 Significant investments in the common stock of financials 48

[Restated] (Millions of yen , %) Basel III Group Consolidated template Items Quarter-End number Common Equity Tier 1 capital: regulatory adjustments (2) 8+9 109,874 Intangible assets other than mortgage-servicing rights (net of related tax liability) 8 13,099 Goodwill (net of related tax liability) Investments in the capital of banking, financial and insurance entities that are outside the scope of 18,889 18 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued share capital (amount above 10% threshold) Regulatory adjustments applied to Common Equity Tier 1 due to insufficient Additional Tier 1 and Tier 2 27 30,123 to cover deductions 159,473 28 Total regulatory adjustments to Common equity Tier 1 (b) Common Equity Tier 1 capital 29 1,123,271 Common Equity Tier 1 capital (CET1) ((a) - (b)) (c) Additional Tier 1 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 6,858 39 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above 10% threshold) 42 23,264 Regulatory adjustments applied to Additional Tier 1 due to insufficient Tier 2 to cover deductions 30,123 43 Total regulatory adjustments to Additional Tier 1 capital (e) Tier 1 capital 1,123,271 45 Tier 1 capital ((c) + (f)) (g) Tier 2 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 23,264 54 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above the 10% threshold) 23,264 57 Total regulatory adjustments to Tier 2 capital (i) Total capital 1,123,271 59 Total capital ((g) + (j)) (k) Risk weighted assets (5) 5,055,974 60 Total risk weighted assets (l) Consolidated capital adequacy ratio 61 22.21% Common Equity Tier 1 (as a percentage of risk weighted assets) ((c) / (l)) 22.21% 62 Tier 1 (as a percentage of risk weighted assets) ((g) / (l)) 63 22.21% Total capital (as a percentage of risk weighted assets) ((k) / (l)) Amounts below the thresholds for deduction (before risk weighting) (6) 117,228 72 Non-significant investments in the capital of other financials 50,650 73 Significant investments in the common stock of financials 49

Qualitative Disclosure (Consolidated) 1. The amount of each account in the balance sheets as in published statements and the reference number in composition of capital disclosure [Original] (Millions of yen) Reference number Balance sheets as in Under regulatory scope of in composition of published statements consolidation capital disclosure 380,724 18, 39, 54, 72, 73 Investment securities 380,724 [Restated] (Millions of yen) Reference number Balance sheets as in Under regulatory scope of in composition of published statements consolidation capital disclosure 380,724 8, 18, 39, 54, 72, 73 Investment securities 380,724 Quantitative Disclosure (Consolidated) 1. Other quantitative disclosures OV1 : Overview of RWA [Original] (Millions of yen) Minimum capital RWA Basel III requirements template number June March June March 2018 2018 2018 2018 1 903,494 903,175 72,279 72,254 Credit risk (excluding counterparty credit risk) (CCR) 2 722,141 747,448 57,771 59,795 Of which standardized approach (SA) 16 1,418,973 1,461,548 113,517 116,923 Market risk 17 903,919 860,281 72,313 68,822 Of which standardized approach (SA) 18 515,053 601,266 41,204 48,101 Of which internal model approaches (IMM) Amounts below the thresholds for deduction (subject to 250% 23 11,397 30,709 911 2,456 risk weight) 410,070 25 Total 4,989,109 5,125,879 399,128 50

[Restated] (Millions of yen) Minimum capital RWA Basel III requirements template number June March June March 2018 2018 2018 2018 1 Credit risk (excluding counterparty credit risk) (CCR) 850,303 903,084 68,024 72,246 2 Of which standardized approach (SA) 668,950 747,357 53,516 59,788 16 Market risk 1,412,401 1,457,444 112,992 116,595 17 Of which standardized approach (SA) 897,386 856,504 71,790 68,520 18 Of which internal model approaches (IMM) 515,015 600,940 41,201 48,075 Amounts below the thresholds for deduction (subject to 250% 23 138,025 114,837 11,042 9,187 risk weight) 25 5,055,974 5,205,812 404,477 416,465 Total MR2 : RWA flow statements of market risk exposures under an IMA [Original] (Millions of yen) VaR Stressed VaR IRC CRM Other Total RWA 1a RWA at previous quarter end 189,559 411,707 - - 601,266 Adjustments to RWA based on the 1b regulatory consolidated capital at previous 6 4 - - 4 quarter end 1c Amounts of IMA at previous quarter end 32,178 106,780 - - 138,959 Change in 2 reporting Movement in risk levels ▲ 7,474 ▲ 46,326 - - ▲ 53,801 period 8a Amounts of IMA at end of reporting period 24,703 60,454 - - 85,158 Adjustments to RWA based on the regulatory consolidated capital at end of 7 6 - - 6 8b reporting period RWA at end of reporting period 176,889 338,164 - - 515,053 8c 51

[Restated] (Millions of yen) VaR Stressed VaR IRC CRM Other Total RWA 1a RWA at previous quarter end 189,672 411,268 - - 600,940 Adjustments to RWA based on the 1b regulatory consolidated capital at previous 5 4 - - 4 quarter end 1c Amounts of IMA at previous quarter end 34,661 114,056 - - 148,717 Change in 2 reporting Movement in risk levels (7,455) (46,550) - - (54,005) period 8a Amounts of IMA at end of reporting period 27,206 67,506 - - 94,712 Adjustments to RWA based on the 8b regulatory consolidated capital at end of 6 5 - - 5 reporting period 8c RWA at end of reporting period 176,552 338,463 - - 515,015 Consolidated Leverage Ratio 1. Composition of consolidated leverage ratio [Original] (Millions of yen) Basel Ⅲ Basel Ⅲ template template Items June 2018 March 2018 number (2) number (1) On-balance sheet exposures (1) 2 7 Common Equity Tier 1 capital: regulatory adjustments 147,794 115,303 3 Total on-balance sheet exposures (excluding derivatives and SFTs) (A) 12,852,826 11,544,374 Securities financing transaction exposures (3) 13 Netted amounts of cash payables and cash receivables of gross SFT assets 1,323,443 1,156,495 16 5 Total securities financing transaction exposures (sum of lines 12 to 15) (C) 4,842,764 6,572,576 Capital and total exposures (5) 20 Tier 1 capital (E) 1,134,950 1,142,340 21 8 Total exposures (A)+(B)+(C)+(D) (F) 19,902,398 20,358,038 22 Basel III consolidated leverage ratio(E)/ (F) 5.70% 5.61% [Restated] (Millions of yen) Basel Ⅲ Basel Ⅲ template template Items June 2018 March 2018 number (2) number (1) On-balance sheet exposures (1) 2 7 Common Equity Tier 1 capital: regulatory adjustments 136,208 117,039 3 Total on-balance sheet exposures (excluding derivatives and SFTs) (A) 12,864,412 11,542,638 Securities financing transaction exposures (3) 13 Netted amounts of cash payables and cash receivables of gross SFT assets 1,352,924 1,156,495 16 5 Total securities financing transaction exposures (sum of lines 12 to 15) (C) 4,813,283 6,572,576 Capital and total exposures (5) 20 Tier 1 capital (E) 1,123,271 1,133,926 21 8 Total exposures (A)+(B)+(C)+(D) (F) 19,884,503 20,356,302 22 Basel III consolidated leverage ratio(E)/ (F) 5.64% 5.57% 52

[As of March 31, 2018] Key metrics (at consolidated group level) [Original] (Millions of yen , %) Basel III template March 2018 December 2017 September 2017 June 2017 March 2017 number Available capital (amounts) Common Equity Tier 1 1 1,142,340 1,142,707 1,134,487 1,140,227 1,131,194 (CET1) 2 1,142,340 1,142,707 1,134,487 1,140,227 1,131,194 Tier 1 3 1,142,340 1,142,707 1,134,487 1,140,227 1,131,194 Total capital Risk-weighted assets (amounts) Total risk-weighted assets 4 5,125,879 5,257,936 5,106,753 5,043,690 4,996,323 (RWA) Capital ratio 5 CET1 ratio (%) 22.28% 21.73% 22.21% 22.60% 22.64% 6 22.28% 21.73% 22.21% 22.60% 22.64% Tier 1 ratio (%) 7 Total capital ratio (%) 22.28% 21.73% 22.21% 22.60% 22.64% Additional CET1 buffer requirements as a percentage of RWA CET1 available after meeting 12 the bank’s minimum capital 14.28% 13.73% 14.21% 14.60% 14.64% requirements (%) Leverage ratio Total leverage ratio exposure 13 20,358,038 20,987,142 19,524,574 18,979,308 19,090,638 measure Leverage ratio (%) including the impact of any 14 applicable temporary 5.61% 5.44% 5.81% 6.00% 5.92% exemption of central bank reserves 53

[Restated] (Millions of yen , %) Basel III template March 2018 December 2017 September 2017 June 2017 March 2017 number Available capital (amounts) Common Equity Tier 1 1 1,133,926 1,131,024 1,140,647 1,143,722 1,125,825 (CET1) 2 1,133,926 1,131,024 1,140,647 1,143,722 1,125,825 Tier 1 3 1,133,926 1,131,024 1,140,647 1,143,722 1,125,825 Total capital Risk-weighted assets (amounts) Total risk-weighted assets 4 5,205,812 5,325,897 5,188,403 5,110,915 5,061,423 (RWA) Capital ratio 5 CET1 ratio (%) 21.78% 21.23% 21.98% 22.37% 22.24% 6 21.78% 21.23% 21.98% 22.37% 22.24% Tier 1 ratio (%) 7 Total capital ratio (%) 21.78% 21.23% 21.98% 22.37% 22.24% Additional CET1 buffer requirements as a percentage of RWA CET1 available after meeting 12 the bank’s minimum capital 13.78% 13.23% 13.98% 14.37% 14.24% requirements (%) Leverage ratio Total leverage ratio exposure 13 20,356,302 21,007,559 19,562,959 18,998,109 19,097,795 measure Leverage ratio (%) including the impact of any 14 applicable temporary 5.57% 5.38% 5.83% 6.02% 5.89% exemption of central bank reserves 54

Composition of Capital Disclosure [Original] (Millions of yen , %) Basel III Exclusion under Group Consolidated template Items transitional Quarter-End number arrangements Common Equity Tier 1 capital: regulatory adjustments (2) 8+9 105,776 - Intangible assets other than mortgage-servicing rights (net of related tax liability) 11,170 - 8 Goodwill (net of related tax liability) Investments in the capital of banking, financial and insurance entities that are outside the scope of 4,629 - 18 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued share capital (amount above 10% threshold) Regulatory adjustments applied to Common Equity Tier 1 due to insufficient Additional Tier 1 and Tier 2 4,016 27 to cover deductions 115,303 28 Total regulatory adjustments to Common equity Tier 1 (b) Common Equity Tier 1 capital 29 1,142,340 Common Equity Tier 1 capital (CET1) ((a) - (b)) (c) Additional Tier 1 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 769 - 39 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above 10% threshold) 42 3,246 Regulatory adjustments applied to Additional Tier 1 due to insufficient Tier 2 to cover deductions 43 4,016 Total regulatory adjustments to Additional Tier 1 capital (e) Tier 1 capital 1,142,340 45 Tier 1 capital ((c) + (f)) (g) Tier 2 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 54 3,246 - regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above the 10% threshold) 57 3,246 Total regulatory adjustments to Tier 2 capital (i) Total capital 1,142,340 59 Total capital ((g) + (j)) (k) Risk weighted assets (5) 60 Total risk weighted assets 5,125,879 (l) Consolidated capital adequacy ratio 22.28% 61 Common Equity Tier 1 (as a percentage of risk weighted assets) ((c) / (l)) 22.28% 62 Tier 1 (as a percentage of risk weighted assets) ((g) / (l)) 22.28% 63 Total capital (as a percentage of risk weighted assets) ((k) / (l)) Amounts below the thresholds for deduction (before risk weighting) (6) 115,098 72 Non-significant investments in the capital of other financials 73 Significant investments in the common stock of financials 33,651 55

[Restated] (Millions of yen , %) Basel III Exclusion under Group Consolidated template Items transitional Quarter-End number arrangements Common Equity Tier 1 capital: regulatory adjustments (2) 106,427 - 8+9 Intangible assets other than mortgage-servicing rights (net of related tax liability) 11,821 - 8 Goodwill (net of related tax liability) Investments in the capital of banking, financial and insurance entities that are outside the scope of 18 7,810 - regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued share capital (amount above 10% threshold) Regulatory adjustments applied to Common Equity Tier 1 due to insufficient Additional Tier 1 and Tier 2 8,599 27 to cover deductions 123,718 28 Total regulatory adjustments to Common equity Tier 1 (b) Common Equity Tier 1 capital 29 1,133,926 Common Equity Tier 1 capital (CET1) ((a) - (b)) (c) Additional Tier 1 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 1,920 - 39 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above 10% threshold) 42 6,678 Regulatory adjustments applied to Additional Tier 1 due to insufficient Tier 2 to cover deductions 8,599 43 Total regulatory adjustments to Additional Tier 1 capital (e) Tier 1 capital 1,133,926 45 Tier 1 capital ((c) + (f)) (g) Tier 2 capital: regulatory adjustments Investments in the capital of banking, financial and insurance entities that are outside the scope of 6,678 - 54 regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above the 10% threshold) 57 6,678 Total regulatory adjustments to Tier 2 capital (i) Total capital 1,133,926 59 Total capital ((g) + (j)) (k) (5) Risk weighted assets 60 5,205,812 Total risk weighted assets (l) Consolidated capital adequacy ratio 21.78% 61 Common Equity Tier 1 (as a percentage of risk weighted assets) ((c) / (l)) 21.78% 62 Tier 1 (as a percentage of risk weighted assets) ((g) / (l)) 63 21.78% Total capital (as a percentage of risk weighted assets) ((k) / (l)) Amounts below the thresholds for deduction (before risk weighting) (6) 72 Non-significant investments in the capital of other financials 115,033 73 48,423 Significant investments in the common stock of financials 56

Qualitative Disclosure (Consolidated) 12. The amount of each account in the balance sheets as in published statements and the reference number in composition of capital disclosure [Original] (Millions of yen) Reference number Balance sheets as in Under regulatory scope of in composition of published statements consolidation capital disclosure 367,196 18, 39, 54, 72, 73 Investment securities 367,196 [Restated] (Millions of yen) Reference number Balance sheets as in Under regulatory scope of in composition of published statements consolidation capital disclosure 367,196 8, 18, 39, 54, 72, 73 Investment securities 367,196 Quantitative Disclosure (Consolidated) 2. Credit risk (exclude counterparty credit risk and securitization) A). Breakdown of exposures by geographical areas, industry and residual maturity [Original] 【 March 2018 】 (Millions of yen) Credit risk exposures Loans Securities Others Japan 5,604,819 751,323 973,771 3,879,725 Overseas 320,531 34,892 29,153 256,484 Total (by area) 5,925,350 786,216 1,002,924 4,136,210 Corporate 294,251 130,733 63,517 100,000 Others 582,178 9,107 297,922 275,149 Total (by industry) 5,925,350 786,216 1,002,924 4,136,210 Indeterminate 5,107,635 690,262 333,781 4,083,591 Total (by maturity) 5,925,350 786,216 1,002,924 4,136,210 57